Valuer Insights

Business Insights | Hong Kong’s FY2025/26 Land Sale Performance Recap

April 23, 2026

Contact

Senior Director, Valuation & Advisory Services, Hong Kong

Contact

Manager, Valuation & Advisory Services, Hong Kong

Introduction

The Hong Kong Government’s Land Sale List for the fiscal year 2025/26 comprised eight sites, all for residential purposes. Out of these eight sites, three were rolled over from the previous fiscal year. No new commercial sites were put up for tender, owing to the continued high vacancy rate of commercial properties across Hong Kong.As the fiscal year draws to a close, the FY2025/26 Land Sale List resulted in five of the eight sites being successfully tendered and awarded. The total land premium income generated from these five residential land sales amounted to approximately HK$8.36 billion, exceeding the corresponding figures recorded over the previous two fiscal years. This provides a modest upside to land sale revenue albeit still far below levels reached in the FY2022/23 and the years prior.

|

Lot No. |

Address |

Total Premium in HK$ bil. (AV/sf) |

Outcome |

|

|

1 |

RBL 1204 |

Cape Road, Stanley, Hong Kong |

N/A |

Not yet sold |

|

2 |

SIL 860 |

1.384 |

Successful |

|

|

3 |

NKIL 6675 |

1.807 |

Successful |

|

|

4 |

NKIL 6674 |

1.610 |

Successful |

|

|

5 |

Lot 317 in DD 223 |

Clear Water Bay Road, Ta Ku Ling, Sai Kung, New Territories |

N/A |

Not yet sold |

|

6 |

TWTL 441 |

Junction of Wing Shun Street and Texaco Road, Tsuen Wan, New Territories |

2.475 |

Successful |

|

7 |

TMTL 569 |

1.089 |

Successful |

|

|

8 |

TCTL 54 |

Area 106A, Tung Chung, New Territories |

N/A |

Not yet sold |

|

|

|

Total Premium Revenue |

8.36 |

|

Table 1: Overview of FY2025/26 Land Sale List

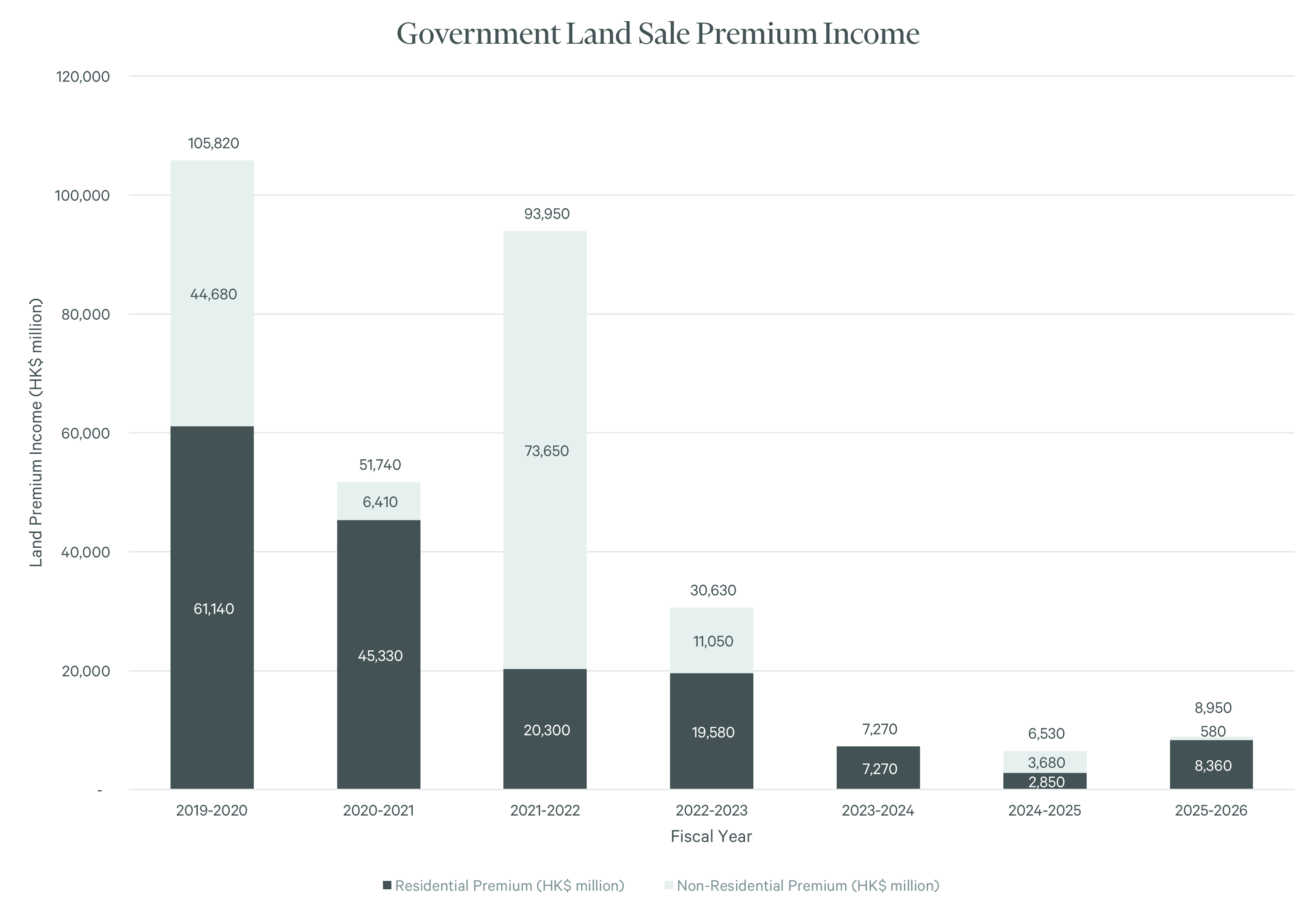

Figure 1: Government Land Sale Premium Income (FY2019/20 to FY2025/26)

Land premium revenue continues to be substantially reduced amid challenging property market conditions and weakened developer confidence, with the latest estimated government revenue from land premium at HK$17.5 billion, revised down from the original estimate of HK$21 billion. However, in FY2025/26, government revenue became more diversified, supported by a significant increase in stamp duty income of approximately HK99.5 billion from IPO activity and equity market turnover, which partially offset the fiscal shortfall from the underperforming land sales market.

That said, it remains inefficient and potentially counter‑productive for the Government to further increase the ad valorem stamp-duty rate for residential properties, with the latest 2026 Budget revision increasing the rate for residential properties valued at over HK$100 million up to a range from 4.5% to 6.5%. This is in addition to the progressive government rates introduced in 2025, which brought increased rates for properties with rateable value over HK$550,000. These layered measures may risk further suppressing high-value residential transactions and capital inflows at a fragile point in the market cycle.

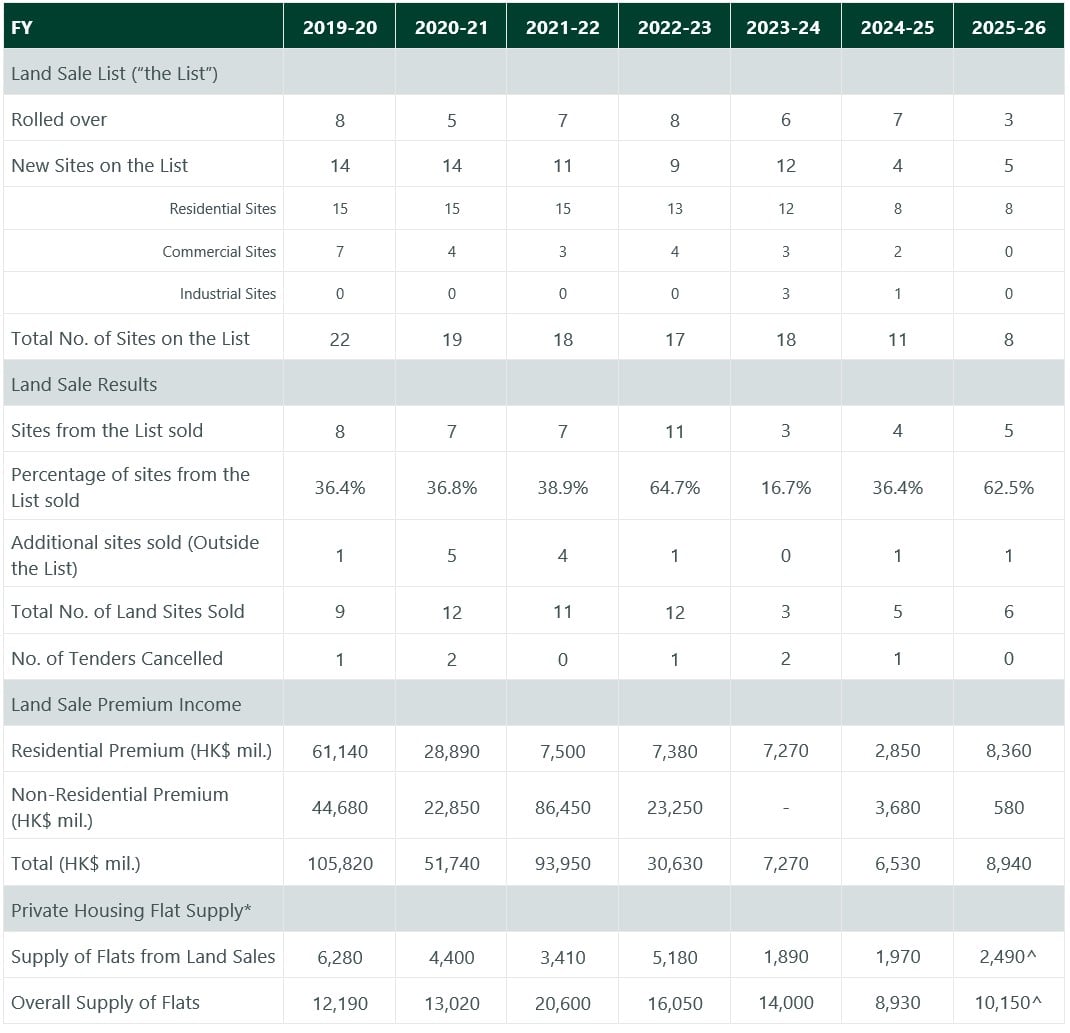

Table 2: Overview of Land Sale Performance (FY2019/20 to FY2025/26)

*Government estimated figures

^Government data not released, according to CBRE estimates

Historical data on the Land Sale shows that over the past seven years, the Government has been able to sell more than 50% of the listed sites in only two years. Moreover, the supply of private housing flats generated from government land sales over the past three years has remained at a relatively low level. Against this backdrop, a consistent and sustained land supply pipeline will be important for maintaining long‑term stability in the housing market.

The tender sites at a glance

Notably, two sites - NKIL 6675 in Kowloon Bay and SIL 860 in Shau Kei Wan, attracted bids that surpassed prevailing market expectations, reflecting stronger-than-anticipated developer interest.New Kowloon Inland Lot No. 6675, located at Choi Ha Road in Ngau Tau Kok, was awarded to a unit of China Overseas Land & Investment Limited for a winning bid of HK$1.806 billion. This transaction is particularly significant as it marks the first successful land tender by a Mainland developer in Hong Kong once again in more than five years. The bid translates into an estimated accommodation value of approximately HK$6,000 per square foot, slightly exceeded general market expectations.

Meanwhile, Shau Kei Wan Inland Lot No. 860 was awarded to a unit of Kerry Properties at a winning bid of HK$1.39 billion, implying an accommodation value of around HK$9,300 per square foot – a bid was notably above market expectations. This perhaps underscores the confidence in the long-term fundamentals of the Hong Kong Island residential market due to land scarcity. This land sale was also the first new land supply on Hong Kong Island in three years.

These two tender outcomes demonstrate that developer demand continues to improve for sites located within established residential neighbourhoods with strong location and amenity fundamentals. Both sites benefit from right-sized development scale, mature surrounding residential communities, proximity to MTR stations, established retail and social infrastructure, and demonstrated end-user demand.

Land Supply outside Government Tender

Meanwhile, in November 2025, the MTR awarded the Tuen Mun A16 Station Package One Property Development to Sun Hung Kai Properties. This project is for a site designated as Tuen Mun Town Lot No. 576, located adjacent to the tentatively named A16 station on the future extension of the Tuen Ma Line, also known as the Tuen Mun South Extension Line. According to CBRE estimates, the land value for the site is approximately HK$1.8 – 2.3 billion, which implies an AV of HK$3,000 to 3,800 per square foot. This assessment excludes any consideration of profit-sharing arrangements with MTR, which will impact the actual land value.The Urban Renewal Authority also successfully tendered the development contract for the Shantung Street / Thistle Street Development Scheme and awarded to a subsidiary of China Overseas Land & Investment Limited, for a tender amount of HK$860.68 million in May 2025.

Overall, the FY2025/26 Land Sale List has begun to demonstrate a gradual restoration in appetite and confidence in Hong Kong’s mass-market residential sector. However, with the most positive outcomes still limited to locations with strong fundamentals, it remains to be seen whether this recovery can be sustained across the broader Hong Kong property market.