Article | Intelligent Investment

Navigating Data Centres: Seizing investment opportunities in Asia Pacific

September 24, 2024

Asia Pacific has emerged as one of the most promising regions for data centres, seeing a surge in investor interest across markets. The region saw the strongest growth of live supply from 2018 to 2023, and is forecasted to grow at a CAGR of more than 10% over the next three years.

Asia Pacific data centre sector poised for growth

As AI and cloud adoption gains traction, the immense computing power and data storage requirements have led to burgeoning demand for data centres, as well as modifications in terms of power infrastructure, rack density and cooling solutions.

While established markets face challenges around power constraints and in most cases, land scarcity, emerging markets – even with their various obstacles, also present good opportunities for investment.

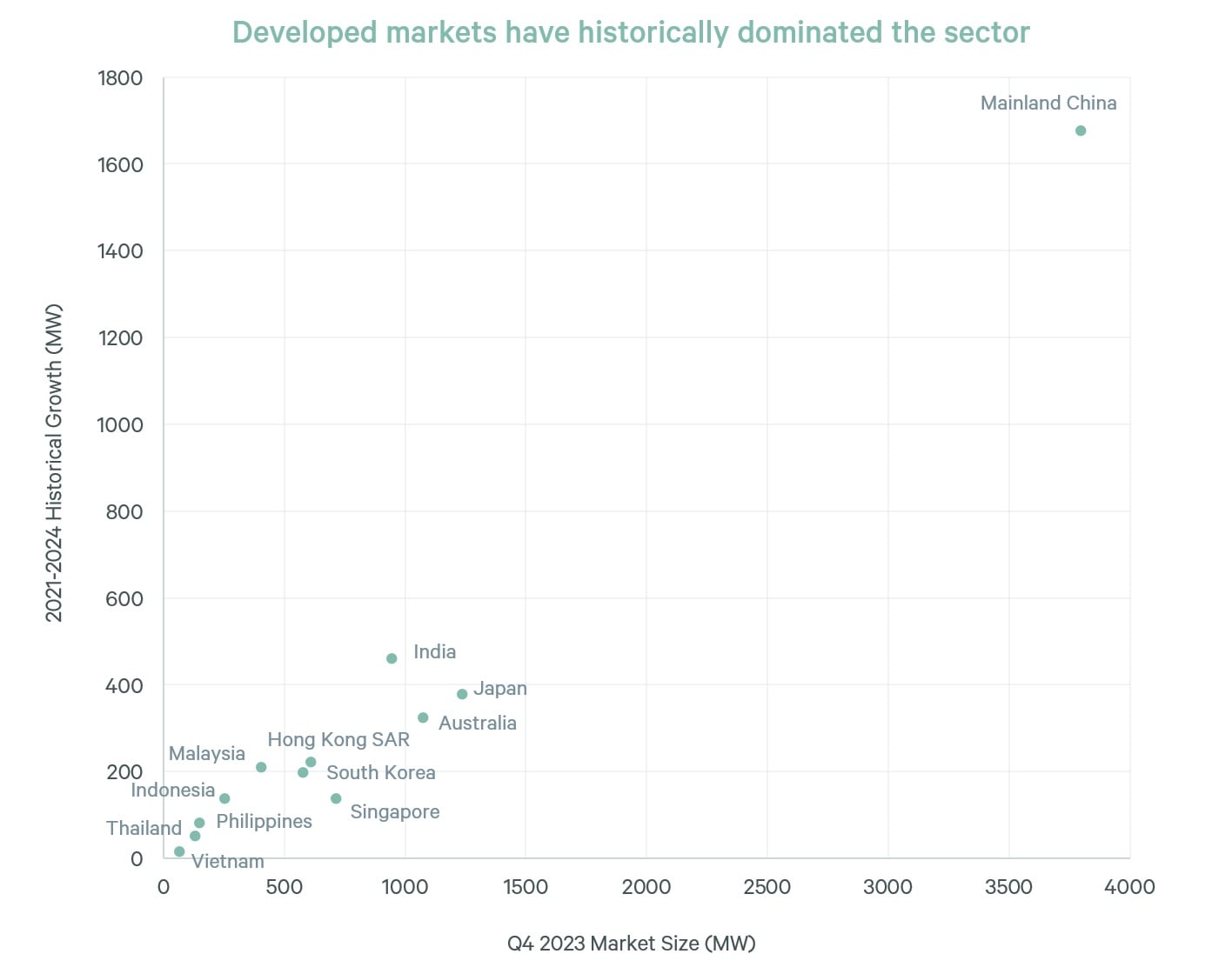

Figure 1: Developed markets have historically dominated the sector

Source: CBRE Digital Infrastructure Advisory

Several Southeast Asian markets have experienced an increase in investor interest; in particular, Malaysia, Indonesia and Thailand are expected to experience exponential growth in the data centre sector, with their capacities anticipated to more than double by 2026.

While there are significant economic benefits to be reaped from such investments, these markets are also cognisant of the potential drawbacks. For instance, the energy-intensive nature of data centres has raised concerns of a potential power supply shortage in Malaysia as electricity demand from data centres alone is expected to hit over 5,000 MW by as soon as 2035.

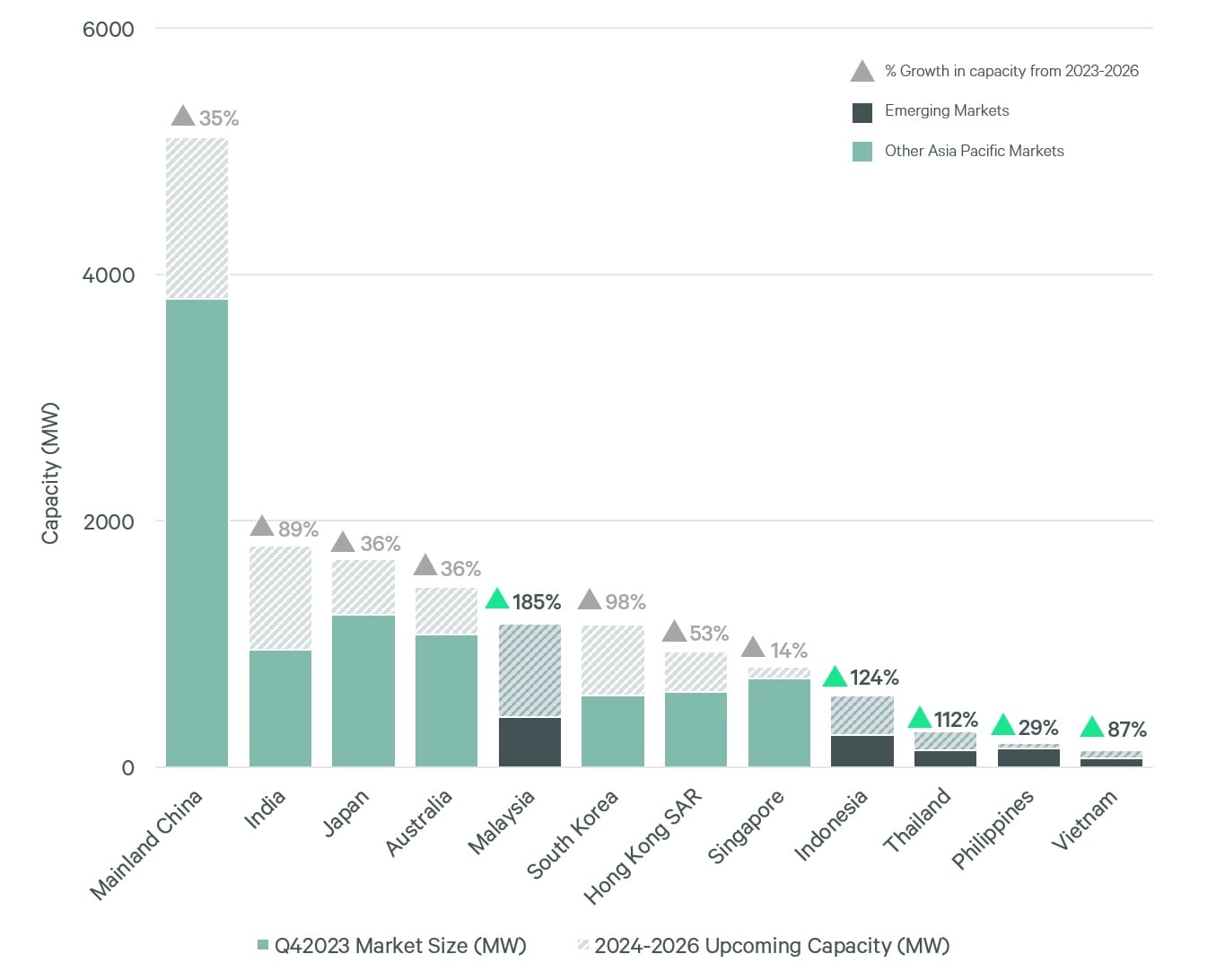

Figure 2: Emerging markets are gathering pace

Source: CBRE Digital Infrastructure Advisory

Each individual market poses nuanced challenges

Figure 3: Regulations and incentives relating to data centres

Emerging markets are extending fiscal incentives to attract data centre investment in a bid to establish themselves as the next data centre hub in the region.

On the other hand, established hubs typically focus on advantages such as advanced infrastructure capabilities and a deeper talent pool to attract data centre investment.

Figure 4: Incentives and investment in emerging markets

| Market | Examples of Incentives and Investments |

| Malaysia |

|

| Indonesia |

|

| Thailand |

|

Demand for data centres will continue to grow

Figure 5: Key drivers supporting data centre growth

Strategies for investors, developers and operators

| Stakeholders | Recommended Strategies |

| Investors & Developers |

|

| Operators |

|

About CBRE Asia Pacific Consulting

CBRE’s Asia Pacific Consulting practice helps clients with complex location strategy decisions that take into account a myriad of important location factors, such as workforce strategies, locational profiling and site selections.

Related Services

- Consulting

Data Center Solutions

Our lifecycle data center service offering consolidates your data center real estate, facilities and technology systems into a single operational and financial model.

- Consulting

Investor Advisory

CBRE is the global leader in commercial real estate services and investments. With capabilities, insights and data that span every dimension of the industry, we support investors and funds, through primary occupier insights, across every geography.

Related Insights

- Article

Navigating Data Centres: As demand for AI surges, what does this mean for data centres?

August 22, 2024

By

Artificial Intelligence (AI) has taken the world by storm. With the introduction of platforms such as OpenAI’s ChatGPT gathering millions of users within a shor...

The global data centre market continues to experience rapid growth, with artificial intelligence (AI) advancements fuelling demand for this asset class.

- Article

How to make the most of the Digital Infrastructure boom in APAC

July 8, 2024 10 Minute Read

By

Digital infrastructure has emerged as one of the most sought-after asset classes by investors, who are seeking stabilised assets and optimal returns for their i...

Despite a challenging economic environment, data centres remain in focus for the commercial real estate industry in Asia Pacific, with notable market developmen...