Article | Creating Resilience

Business Insights | Understanding mandatory climate related financial disclosures

The built environment is responsible for roughly 20% of Australia’s emissions. It’s why real estate owners across office, retail and industrial assets need to understand how to address sustainability ratings as it becomes embedded in valuation and leasing decisions.

November 2, 2025

Sustainability reporting solutions

Learn MoreHow mandatory disclosures impact commercial real estate

What?In September 2024, the Australian Government passed the Treasury Laws Amendment Bill, mandating large and medium-sized companies to report on climate-related risks, opportunities, and greenhouse gas emissions. Disclosed sustainability data must meet Australian Sustainability Reporting Standards (ASRS) assurance requirements. This legislation aligns with International Financial Reporting Standards.

When?

The reporting period for the largest companies started on January 1, 2025. They must report their first full financial period after this date, with initial disclosures due in 2026.

Who?

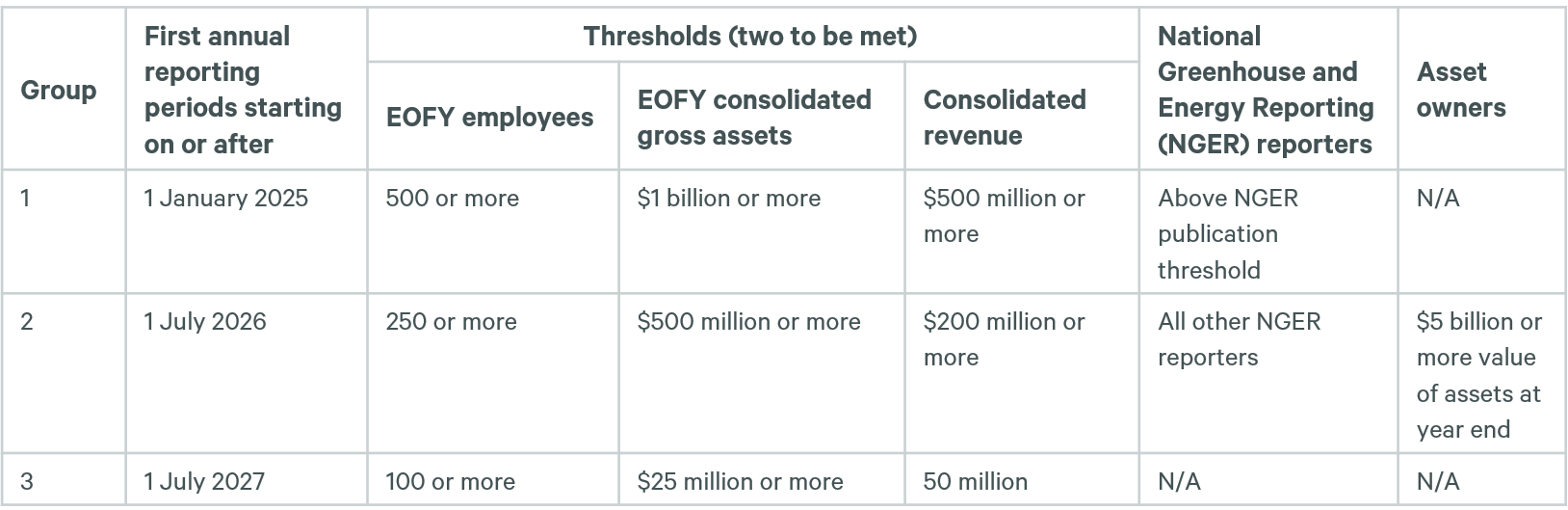

Large listed and unlisted entities under the Corporation Act that meet two of the three specified criteria must report, impacting commercial real estate owners, developers and occupiers. Asset owners with $5 billion in assets under management (AUM) fall into Group 2 and must report by the end of FY 2027 – as outlined in the table below:

Source: treasury.gov.au Mandatory climate-related financial disclosures, Policy Position Statement

This legislation affects the majority of companies in Australia. Companies in Group 1 must disclose in 2026 and should start preparing now. This includes assessing both physical and transition climate-risk exposure across the value chain, creating an emissions inventory, and analysing supply chain readiness. Early movers in the property sector are already leveraging disclosure readiness to differentiate assets in capital markets, as highlighted in CBRE’s Australian Real Estate Market Outlook.

Why it matters

This legislation promotes consistency, transparency, and comparability in sustainability reporting. For Australia, it’s a critical step on the journey to net zero by 2050. For property stakeholders, it’s a signal: your climate exposure, data, and governance structures will now be under scrutiny.Cutting through complexity

Navigating dynamic and challenging market conditions becomes even more complex when new regulations are introduced, particularly for organisations whose core business is not real estate.We’ve simplified the steps into a practical pathway:

1. Determine if you are in scope and your reporting timeline

The first step for property owners, developers and occupiers is to confirm your disclosure group and when to start reporting. Timelines vary, but clarity here determines the urgency of your compliance planning and data capture.Group 1

- Data capture: Start of your financial year in 2025

- First report due: 2026 at the end of your financial year

Group 2

- Data capture: Start of your financial year after 1 July 2026

- First report due: 2027 at the end of your financial year

Group 3

- Data capture: Start of your financial year after 1 July 2027

- First report due: 2028 at the end of your financial year

2. Assess your current position

For real estate owners and occupiers, disclosure readiness starts with understanding how climate impacts and opportunities are integrated into governance, strategy, risk, and performance. These lenses provide a practical baseline to identify gaps and prepare portfolios for compliance and long-term value.3. Start collecting data

For commercial real estate, disclosure begins at the asset level. Collecting accurate Scope 1, 2 and 3 emissions data across buildings and value chains creates the foundation for credible reporting and positions assets for long-term resilience and value.

Compile information required to calculate an organisational carbon account (total greenhouse gas [GHG] emissions) by scope:

- Scope 1: Emissions from directly burning fossil fuels on-site

- Scope 2: Emissions created off-site from purchased electricity/power

- Scope 3: Indirect upstream or downstream emissions relating to business activities such as purchasing, transportation, product use, disposal and investments that generate emissions outside a company’s direct control but within its value chain.

Disclosed sustainability data must meet Australian Sustainability Reporting Standards (ASRS) assurance requirements. This ensures it is accurate, consistent, and traceable with links to source data for auditors, supports regulatory compliance, enables efficient reporting, and scales with increasing legislated assurance requirements.

Pro tip: While some data platforms are designed to track emissions across an organisation’s value chain, they often fall short when it comes to the unique demands of real estate. Maximising value and ensuring readiness for regulatory reporting requires a solution that’s purpose-built to optimise the sustainability performance of physical assets and to unlock long-term property value.

We’ll guide you through the data deep dive

Mandatory climate disclosures require a focus on accurate data and a comprehensive approach to climate risk and opportunity analysis - disciplines that many organisations are still building. In practice, this means integrating asset-level metrics already familiar to real estate owners - NABERS, Green Star, Climate Active, and GRESB - into ASRS-aligned reporting frameworks. Our experts bring technical mastery, regulatory understanding, and real estate specific insights to help you report with confidence. Below are the key data points required to report:

How CBRE can help

Our sustainability professionals have the expertise to contextualise Australia’s mandatory disclosures in a complex global regulatory landscape for your portfolio or asset and get you ready for compliance.We’ve got you

As a single-source provider of comprehensive solutions – from planning to execution – we simplify complexity, mitigate risk and enable operational improvements and investments that create value at scale.Our team includes accredited professionals in GRESB, WELL, climate disclosure frameworks (ISSB/ASRS/TCFD), net zero strategy, and ESG data systems, bringing global standards and local insights together to deliver practical, high-impact solutions.

We work in close partnership with CBRE’s market-leading Property Management team, who implement and manage Sustainability data platforms and day-to-day operational programs.

Talk to our Sustainability Solutions team today.

Sustainability Solutions

We help organisations decarbonise, fast. As pioneers in real estate, CBRE simplifies complexity, turning your operations and assets into shining examples of environmental responsibility.