Article | Intelligent Investment

Business Insights | The evolving role of Sydney’s inner-city industrial precincts

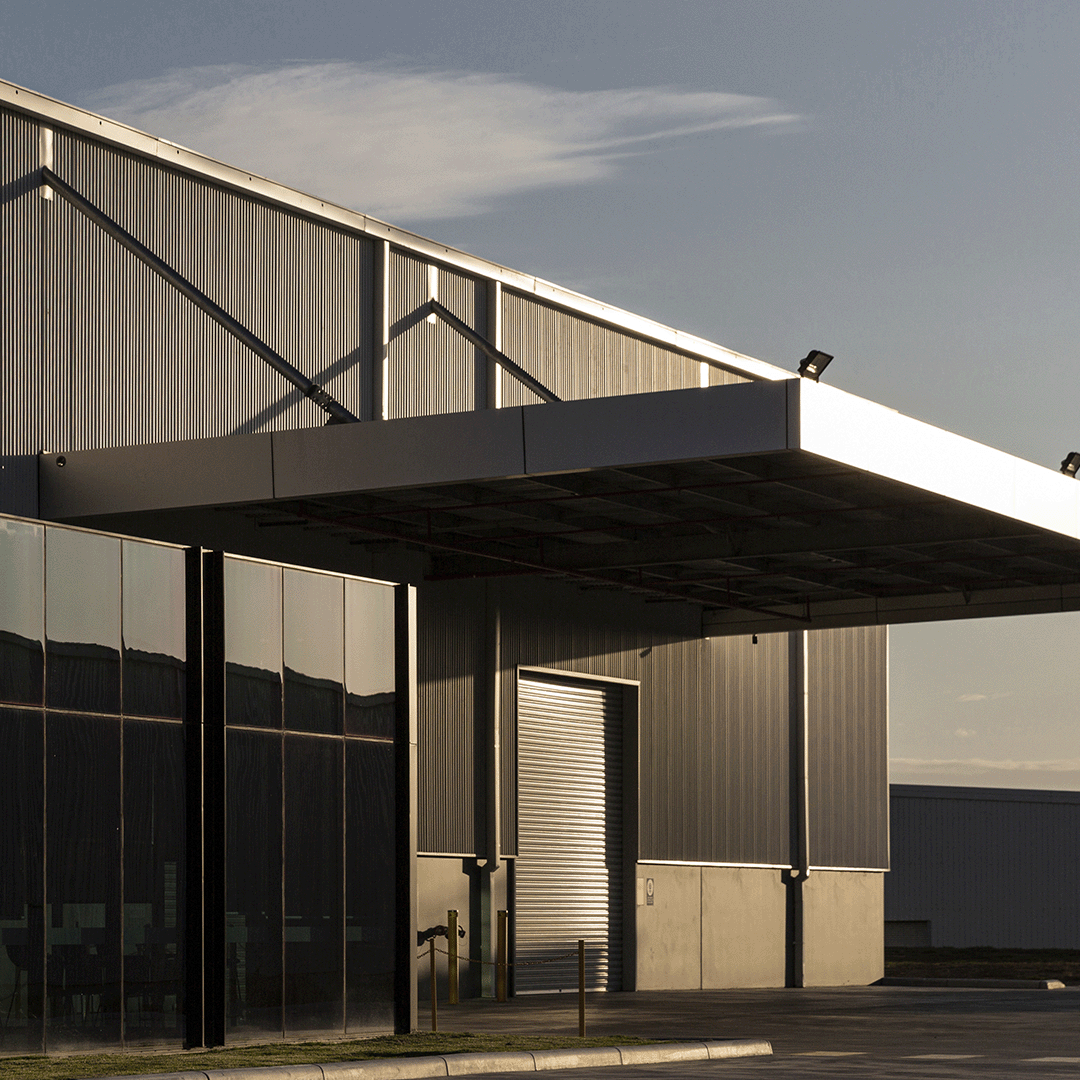

Sydney’s inner-city industrial precincts are undergoing a structural transformation and creating a highly competitive environment where demand is now outpacing supply.

September 15, 2025

Start your journey in Industrial & Logistics

Click HereSydney’s inner-city industrial precincts are undergoing a structural transformation. Once dominated by traditional warehousing and logistics, these areas are now home to a broader mix of occupiers, from data centres and defence contractors to lifestyle brands, self-storage operators, and high-end showrooms. This shift is creating a highly competitive environment where demand for well-located, flexible space is outpacing supply.

Rise of softer industrial

The definition of industrial is expanding. In precincts such as Alexandria, Rosebery, and Waterloo, a growing number of occupiers are redefining what these spaces can be:

- Showrooms for furniture, automotive, and lifestyle brands are targeting affluent inner-city consumers

- Recreational operators such as gyms, climbing centres, and indoor sports venues are leveraging large floorplates and high ceilings

- Self-storage providers are competing for the same assets, offering long-term stability and low churn

- Automotive and luxury vehicle brands are establishing flagship showrooms and service centres in high-visibility locations

- Trade supply businesses are prioritising accessibility and speed to service time-sensitive customer needs

This diversification is intensifying competition for space and pushing landlords to consider a wider range of tenant types. Properties that can flex to accommodate these uses are more likely to remain fully occupied and command premium rents.

Location still matters

Sydney’s inner-city industrial landscape is at a pivotal moment. As traditional warehousing gives way to a more diverse mix of occupiers, the pressure on space is intensifying. Tenants who must remain close to key markets, particularly in South Sydney, are increasingly willing to pay a premium, driving rents upward.

In response, many are rethinking their operational footprints. Non-essential functions are being relocated to fringe or regional areas, while core operations remain close to customers and transport links. But location is still everything. Being just a few streets too far from public transport or cafe culture can derail a deal. Access to parking is now a premium feature, not a given.

For landlords, presentation matters. Properties that offer vision, flexibility, and amenity are more likely to attract and retain tenants. In a tight market, these factors can be the difference between prolonged vacancy and full occupancy.

Competing priorities, limited supply

The inner south has become a battleground for space. A wide range of occupiers are competing for limited land:

- Tech and defence sectors require secure, high-spec facilities to support government and private contracts

- Waste and recycling operators must remain close to the communities they serve

- Data centres are increasingly locating in urban fringe areas due to their infrastructure needs

- Residential encroachment is creating planning tensions, as families live just streets away from industrial traffic

This convergence of uses is placing unprecedented pressure on land supply. Developers and investors must navigate complex planning environments while identifying assets that can serve multiple functions.

Adaptive reuse and upcycling

Older industrial assets are being repositioned to meet modern requirements. Obsolete stock is being replaced or upgraded with ESG considerations in mind. Mixed-use hubs like Sydney Corporate Park show how industrial buildings can be transformed into vibrant destinations that combine business accommodation with lifestyle amenity.

- Purpose-built facilities are replacing outdated stock to meet modern operational needs

- Mixed-use precincts are attracting a broader range of tenants and visitors

- Long-term leases in logistics, storage, and data infrastructure remain attractive to investors

Assets that can be adapted or repositioned are well placed to capture demand from emerging sectors. Investors should look beyond traditional industrial metrics and consider long-term flexibility and placemaking potential.

Planning and policy response

The City of Sydney and surrounding councils are under pressure to balance:

- Industrial retention with residential growth

- Short-term flexibility with long-term land use certainty

- Economic productivity with urban liveability

Policy settings will play a critical role in shaping the future of inner-city industrial. Stakeholders must engage early and often to ensure planning frameworks support both innovation and investment.

What comes next?

As demand intensifies, the question is not just how to accommodate these uses, but where. Key trends to watch include:

- The rise of vertical industrial developments

- Zoning reform to allow greater flexibility

- Decentralisation to outer metropolitan areas

- Landlords repositioning assets to attract non-traditional occupiers

The inner-city footprint may not grow, but its function is expanding. Those who anticipate and respond to these shifts will be best positioned to lead.

Positioning for the future

Sydney’s inner-city industrial market is no longer defined by a single use class. It is a dynamic, multi-use environment where occupiers from vastly different sectors are competing for the same scarce land. For investors and developers, the opportunity lies in anticipating these shifts and delivering assets that are not only fit for purpose but fit for the future.

Get in Touch

Shaping Sydney’s Tomorrow

Discover expert insights on how Sydney is evolving across housing, workspaces, retail, and industrial growth.