Creating Resilience

The Lag in Food and Beverage Recovery

By Robert Mandelbaum and Andrew Hartley

December 7, 2022 7 Minute Read

Unfortunately for the owners and operators of full-service, convention and resort hotels, food and beverage (F&B) revenue is lagging in recovery and yet to return to pre-COVID levels. This can be attributed to a combination of the following factors:

- Health regulations

- The lag in group demand recovery

- Staffing shortages

- Relaxed brand standards

- Cost control measures

To gain a better understanding of recent trends in hotel food and beverage within U.S. hotels, CBRE analyzed the F&B department revenues, expenses and profits of 1,228 properties that reported F&B revenue to our annual Trends® in the Hotel Industry survey each year from 2015 through 2021. Estimates for 2022 F&B revenues, expenses and profits were made based on the performance of a sample of 1,000 hotels through August 2022.

The sample consisted of three property types:

- Full-Service Hotels – Properties that offer some degree of F&B service through restaurants, lounges and in-room dining, plus a limited amount of meeting and banquet space.

- Convention Hotels – Properties that frequently offer multiple F&B venues, in-room dining, plus extensive meeting and banquet space.

- Resort Hotels – Hotels that offer extensive recreational facilities. F&B facilities and services may be limited or extensive.

Limited-service and extended-stay hotels that only offer complimentary food and beverages were excluded from this analysis.

Revenues

In 2020, total F&B department revenues measured on a dollar per-available-room (PAR) basis declined by 72.5 percent. This is greater than the 67.5 percent fall-off in total hotel revenue. Despite growth in 2021 and 2022, CBRE estimates that 2022 annual F&B revenue levels for the hotels in our sample will be just 88.3 percent of 2019 levels at year end.The relative F&B revenue recovery by property type follows the overall demand patterns for the various categories. For 2022, full-service F&B revenues are estimated to be 18.6 percent behind 2019 levels. These hotels are frequently dependent on individual business travelers, the demand segment that has struggled the most to return. Group demand has shown some degree of revival, supporting the ability of convention hotels to return to 92.5 percent of their 2019 F&B revenue levels. Given the strong resurgence in leisure travel, CBRE estimates that resort property F&B revenue will surpass 2019 volume in 2022 by 15.7 percent.

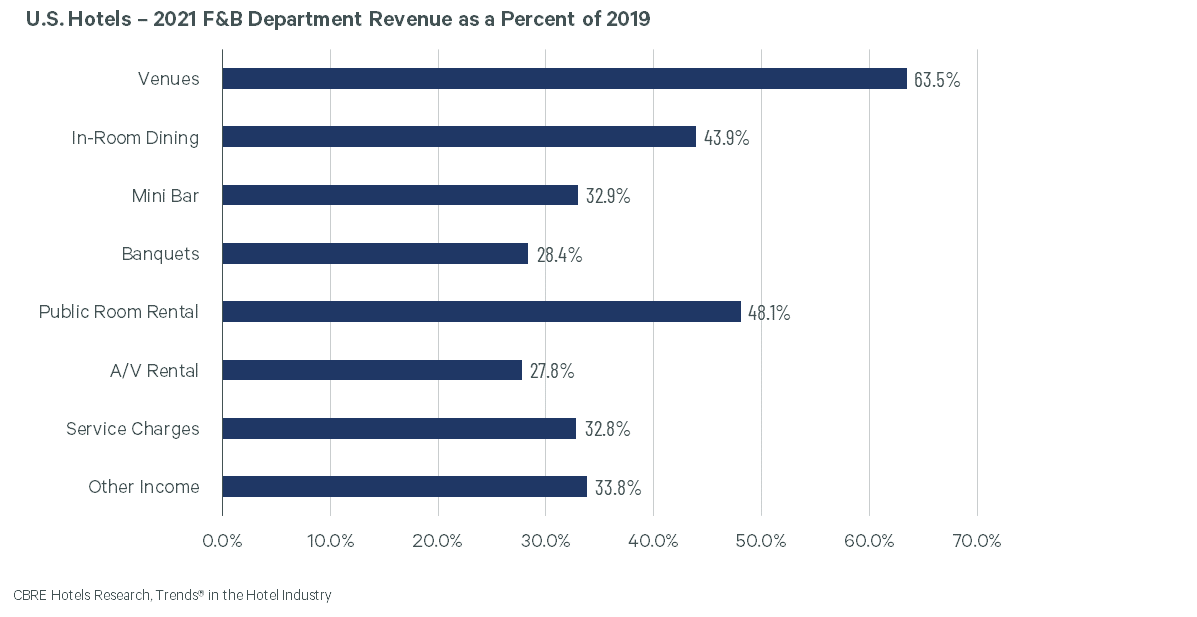

While F&B revenue on a PAR basis has yet to recover to 2019 levels, F&B revenue on a per-occupied-room (POR) basis has. As of August 2022, F&B revenue on a POR basis is on pace to be 13.8 percent above 2019 sales. Analyzing the F&B department revenue sources that have increased at the greatest pace since 2019 provides some insights into the POR growth. Strong venue revenue gains indicate menu price increases since cover counts are believed to be reduced. In-room dining gains reflect guests’ desire to stay in their guest room and away from crowded restaurant dining rooms. Finally, we have seen strong gains in public room rental revenue, concurrent with relatively tepid growth in banquet revenue. This indicates an increase in local business meetings and local catering events that supply their own food and beverages. Increases in local F&B revenue contributes significantly to a rise in revenue on a POR basis.

Trends Influencing F&B Revenue

Toward the end of 2021 and going into 2022, social group functions, such as weddings, galas, reunions, etc., ramped up aggressively. Full-service and convention hotels in corporate or downtown locations, which historically serviced midweek events, have been filling up on the weekends. Social groups are varied and could lead to inconsistent pricing of F&B services.Properties with aggressive F&B planning such as rooftop venues, active lobby bars or signature restaurants, are ramping up faster than competitors as the F&B amenity is potentially a major leisure and small group/events draw for local diners and travelers. Furthermore, pre-pandemic, the industry was pushing toward oversized, trendier, bar-centric F&B outlets to differentiate among traditional competitors. Many of the new designs did away with the prototypical isolated restaurant space and treated the entire lobby as an F&B outlet. This creates a sense of place and an active environment at check-in and drives greater F&B revenues with greater efficiencies, and an increase overall in ADR. This trend looks to be continuing despite disruptions from COVID. Moreover, these less traditional F&B models are flexible and can operate as counter-service grab and go or full-service, depending upon brand standards, time of day, location and guest profile.

In general, operators have had to reconfigure their F&B standards and service to accommodate local health and brand restrictions. Some of these efficiencies are sticking and have contributed to a more dynamic F&B service style.

Expenses and Profits

While lagging revenues are troublesome, the rise in F&B operating expenses is becoming a greater concern. CBRE estimates that by year-end 2022, the F&B department profit margin for the hotels in our sample will be 27.7 percent. This is less than the 30.5 percent profit margin achieved in 2019.Labor and costs of goods are the primary contributing factor to the reduction in profit margins. The country is at near full-employment and low wage driven hotels/restaurants are susceptible to this dynamic. According to various interviews, individual position wages have grown 20 to 40 percent over 2019 levels as F&B outlets are struggling to re-staff and maintain. Food prices have increased more than 10 percent relative to 2021 and inflationary concerns are continuing.

Fortunately, these costs have been somewhat mitigated with streamlined staffing and greater menu pricing. As mentioned earlier, the shift in restaurant service styles lends itself to potentially eliminating various redundant positions. Additionally, these new F&B outlets offer smaller and focused menu planning with better quality, but less quantity and selection.

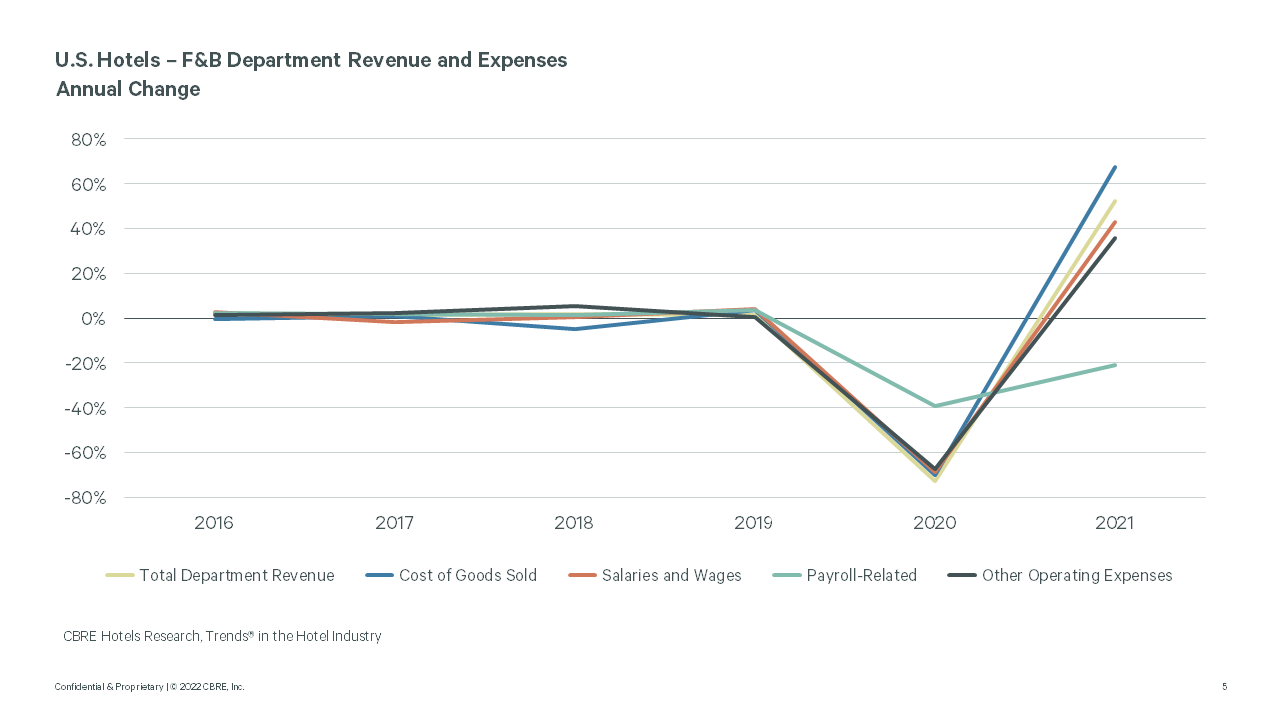

In 2021, the cost of food and beverages increased at the greatest pace (67.6%) among all department expenses. This was followed by salaries and wages (42.9%) and other operating expenses (35.7%). Only a reduction in payroll-related expenses (-20.9%) helped to moderate total F&B department expense growth. The reduction was the result of fewer severance payments made in 2021 compared with 2020.

Unfortunately, we believe these expense trends from 2021 have continued into 2022, without the benefit of the payroll-related reductions. During the early stages of 2022 we observed some operating efficiencies and growing margins, but those have been on a downward trend since April as inflation has risen.

Given these relative changes in revenues and expenses, CBRE estimates that F&B Department profits PAR will be just 80.2 percent of the profits earned in 2019. Like department revenues, full-service F&B profits will lag the most in 2022, while resort hotels will record a 19.8 percent premium in F&B profits over 2019.

The Future

Leading up to COVID, the F&B space within hotels has long been a ‘necessary evil’. This less profitable department posed greater day-to-day risks. The industry started introducing flexible, lifestyle F&B offerings that follow current dining trends and potentially mitigate fixed expenses. Concurrently the modern traveler and diner has drifted away from hands-on service styles in favor of higher quality food and streamlined service.Within the free-standing restaurant space, fast-food and table service dining are merging, and the high-quality $25 burger wrapped in paper served at the counter is here to stay. Hotel F&B (and hotels in general) are following a similar trajectory. Limited-service is merging with full-service. Smaller limited-service dining rooms combined with craft cocktails and artisanal appetizers are redefining what modern guests value in their hotel stays.

The industry will continue to balance standards, service, efficiency and quality to maximize profit and reduce risk. From a groups/conference perspective, event space is becoming more varied with unique alternatives to supplement the traditional ballrooms, junior ballrooms and breakouts spaces. Depending upon location, new outliers in the space include screening rooms, sound studios, art galleries, eSport/game rooms and/or rooftop venues. The pandemic was detrimental to the F&B space but potentially accelerated various trends the industry was initially sluggish to adopt.