Article | Intelligent Investment

Business insights | Can crucial housing be created from withdrawn offices?

With housing in high demand across Australia, our experts explore the unique potential alongside the challenges of withdrawn office stock being redeveloped for residential use.

August 8, 2025

Learn about office stock withdrawals

Click Here

One trend is clear when it comes to residential demand in Australia today.

Established houses, new houses, and recently renovated properties continue to experience the strongest demand, according to findings from CBRE’s residential research. An important fact to highlight is the appeal of freshly renovated properties, which include apartments.

It’s a fitting segue to CBRE’s latest office report, The Great Withdrawal, which explores the impact of office stock withdrawals in major CBDs like Sydney. Interestingly, it found that properties permanently withdrawn from office stock are being earmarked for redevelopment into residential apartments to reflect the current climate.

This raises the critical question: How feasible is redeveloping or converting withdrawn office stock into residential housing?

“We see circa-$960 billion of additional income in the system to support mortgage, rents and other living expenses,” says CBRE’s Head of Pacific Research, Sameer Chopra.

CBRE forecasts the future supply of apartments is likely to hover around 60,000 per annum from 2025 to 2029. Australia’s forecast population growth requires apartment supply of 75,000 per annum to avoid further falls in vacancy.

Looking at the major cities specifically, Sydney’s apartment delivery will average 12,200 per annum from 2025 to 2029 – well below the 30,000 per annum demand for total housing stock.

And the outlook isn’t any brighter in Melbourne. Apartment delivery is set to average 9,300 per annum over that same period, which is almost 25% less supply than Sydney. Demand meanwhile is expected to average 38,000 per annum over the next five years.

In Brisbane, average supply will see 4,800 apartments per annum while demand will hover at 16,000 per annum.

Converting withdrawn offices into accommodation isn’t just feasible; it’s already happening.

“We’ve started marketing a student accommodation asset in Perth that was a former office,” explains Andrew Purdon, Pacific Head of CBRE’s Living Sectors Capital Markets business.

Campus Perth & Hostel G is the latest example of this successful adaptive re-use of an office for residential use. More importantly, these conversions aren’t just destined for the premium end of the market.

“It’s quite the opposite. Depending on the physical characteristics and the building’s location, you can create accommodation for very specific cohorts of the population including young professionals, students and affordable housing.”

The work involved in the conversion is fundamentally building specific. Not every office can be converted, and physical considerations such as the floor to ceiling height, openable windows, floorplate depth and the inclusion of balconies for residential use all need to be addressed before any talks of conversion.

“Another important characteristic is the financial viability of taking existing office buildings and changing them for a totally different use, simply because there’s a lot of capex involved,” says Andrew.

In today’s climate, studio-led conversions are making the most noise with examples such as smaller type residential offerings - think student accommodation and co-living spaces. There are also societal benefits when considering office conversions. Delivering a better carbon footprint through the re-use of existing structures is one.

“You’re creating value out of older and potentially obsolete offices, giving them a new lease on life. And depending on where the building is, bringing residential into office areas can also activate the precinct, lending itself to supporting a 24-hour economy.”

One final consideration for these types of conversions is the time frame; a factor that Andrew says is entirely dependent on the work involved.

“In some instances, you could be taking the office building back to frame and then developing it again. But if the floorplate and condition of the property is a good fit, it can be a very quick process. It could just be 12 months to take it from an old office to a new form of residential.”

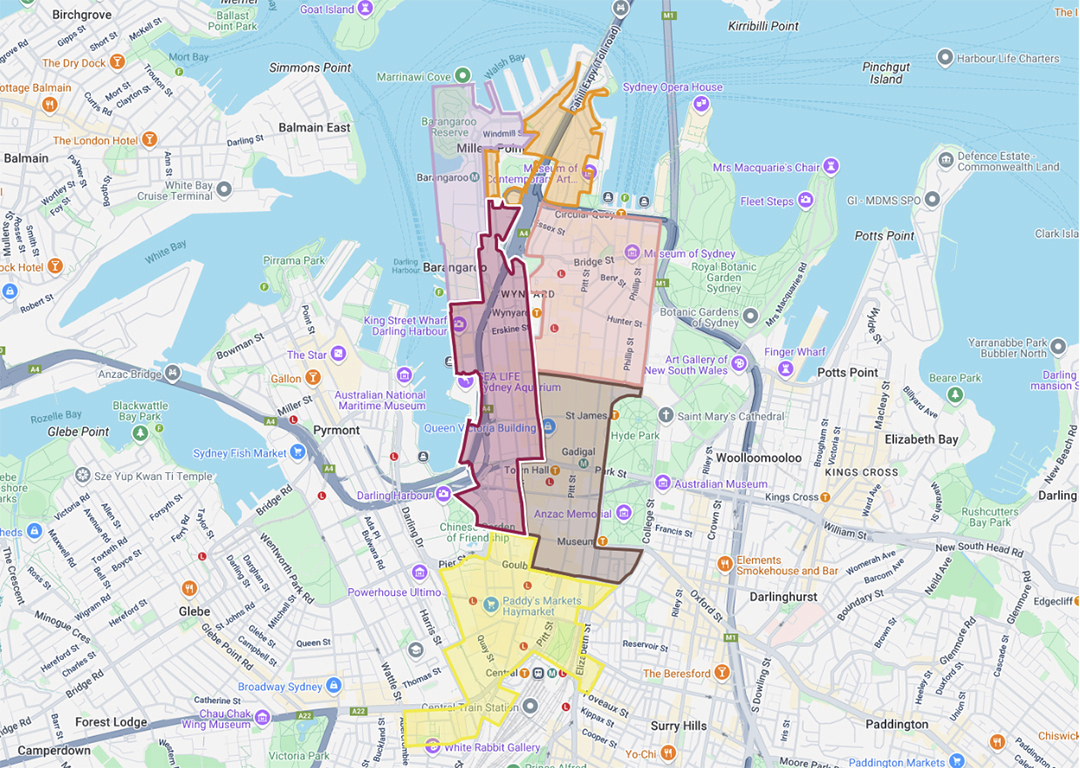

The office withdrawal report found that all the properties earmarked for permanent withdrawal are located outside of Sydney's Core precinct. That covers areas such as Midtown (brown region), Western Corridor (red region), and Southern Precinct (yellow region).

“Office leasing markets in these areas were the hardest hit exiting the pandemic as flight-to-quality drove migration into the Core,” explains Thomas Biglands, CBRE's Associate Director and report author.

“Owners of struggling office properties in these precincts have therefore been searching for alternative strategies to reposition or redevelop their assets.”

For a deeper dive into the market dynamics driving office withdrawals and their broader impact on Australian cities, download CBRE's full report on 'The Great Withdrawal' or contact the Living Sector Teams for tailored insights.

Established houses, new houses, and recently renovated properties continue to experience the strongest demand, according to findings from CBRE’s residential research. An important fact to highlight is the appeal of freshly renovated properties, which include apartments.

It’s a fitting segue to CBRE’s latest office report, The Great Withdrawal, which explores the impact of office stock withdrawals in major CBDs like Sydney. Interestingly, it found that properties permanently withdrawn from office stock are being earmarked for redevelopment into residential apartments to reflect the current climate.

This raises the critical question: How feasible is redeveloping or converting withdrawn office stock into residential housing?

Australia’s current housing situation

Over the next 10 years, demand for housing is expected to benefit from the triple boost of rising population, rising jobs and rising income.“We see circa-$960 billion of additional income in the system to support mortgage, rents and other living expenses,” says CBRE’s Head of Pacific Research, Sameer Chopra.

CBRE forecasts the future supply of apartments is likely to hover around 60,000 per annum from 2025 to 2029. Australia’s forecast population growth requires apartment supply of 75,000 per annum to avoid further falls in vacancy.

Looking at the major cities specifically, Sydney’s apartment delivery will average 12,200 per annum from 2025 to 2029 – well below the 30,000 per annum demand for total housing stock.

And the outlook isn’t any brighter in Melbourne. Apartment delivery is set to average 9,300 per annum over that same period, which is almost 25% less supply than Sydney. Demand meanwhile is expected to average 38,000 per annum over the next five years.

In Brisbane, average supply will see 4,800 apartments per annum while demand will hover at 16,000 per annum.

Realities of turning office into residential

Converting withdrawn offices into accommodation isn’t just feasible; it’s already happening.

“We’ve started marketing a student accommodation asset in Perth that was a former office,” explains Andrew Purdon, Pacific Head of CBRE’s Living Sectors Capital Markets business.

Campus Perth & Hostel G is the latest example of this successful adaptive re-use of an office for residential use. More importantly, these conversions aren’t just destined for the premium end of the market.

“It’s quite the opposite. Depending on the physical characteristics and the building’s location, you can create accommodation for very specific cohorts of the population including young professionals, students and affordable housing.”

The work involved in the conversion is fundamentally building specific. Not every office can be converted, and physical considerations such as the floor to ceiling height, openable windows, floorplate depth and the inclusion of balconies for residential use all need to be addressed before any talks of conversion.

“Another important characteristic is the financial viability of taking existing office buildings and changing them for a totally different use, simply because there’s a lot of capex involved,” says Andrew.

In today’s climate, studio-led conversions are making the most noise with examples such as smaller type residential offerings - think student accommodation and co-living spaces. There are also societal benefits when considering office conversions. Delivering a better carbon footprint through the re-use of existing structures is one.

“You’re creating value out of older and potentially obsolete offices, giving them a new lease on life. And depending on where the building is, bringing residential into office areas can also activate the precinct, lending itself to supporting a 24-hour economy.”

One final consideration for these types of conversions is the time frame; a factor that Andrew says is entirely dependent on the work involved.

“In some instances, you could be taking the office building back to frame and then developing it again. But if the floorplate and condition of the property is a good fit, it can be a very quick process. It could just be 12 months to take it from an old office to a new form of residential.”

Location of withdrawals

While the potential for residential derived from office has promising signs, don't expect to see the onset of waterfront high-rise apartments occupying the space of former office buildings.The office withdrawal report found that all the properties earmarked for permanent withdrawal are located outside of Sydney's Core precinct. That covers areas such as Midtown (brown region), Western Corridor (red region), and Southern Precinct (yellow region).

“Office leasing markets in these areas were the hardest hit exiting the pandemic as flight-to-quality drove migration into the Core,” explains Thomas Biglands, CBRE's Associate Director and report author.

“Owners of struggling office properties in these precincts have therefore been searching for alternative strategies to reposition or redevelop their assets.”

For a deeper dive into the market dynamics driving office withdrawals and their broader impact on Australian cities, download CBRE's full report on 'The Great Withdrawal' or contact the Living Sector Teams for tailored insights.