Intelligent Investment

High-Supply Multifamily Markets Begin to Recover

September 4, 2024 3 Minute Read

Many multifamily markets that have seen the most growth in new supply, and consequently the most negative effective rent growth, may be recovering soon. Occupancy rates have stabilized across these markets as renter demand has absorbed much of this new supply.

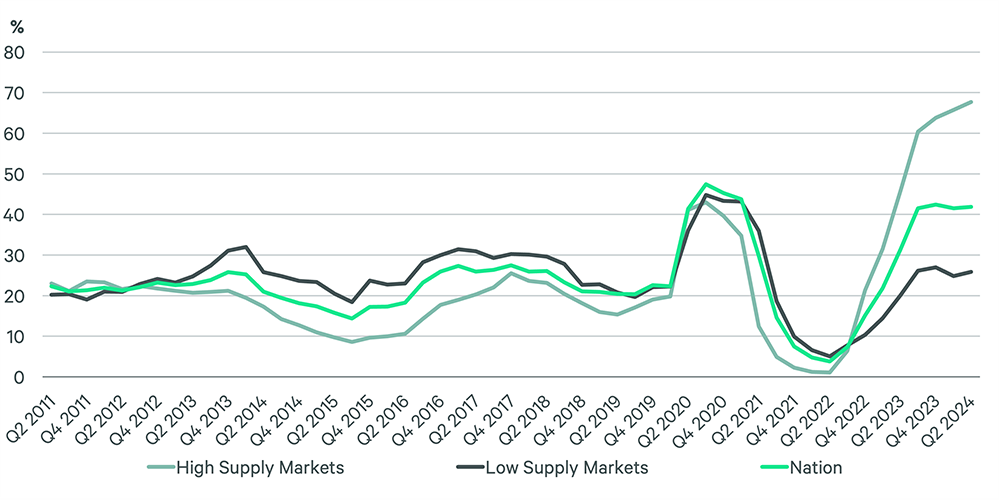

Figure 1: Percentage of multifamily inventory with negative rent growth by segment

More than 20% of total inventory in most multifamily markets typically see rents decline in any given year. Low-supply markets have recently seen negative rent growth for 26% of their inventory, only slightly more than the typical level. Negative rent growth has been a bigger challenge in high-supply markets, where nearly 70% of the inventory had negative rent growth in Q2 2024. Even in the hardest-hit markets, it is notable that nearly one-third of the inventory is still showing positive rent growth.

We expect the negative rent growth trend will soon reverse as demand begins outpacing new supply, boosting both occupancy rates and rent growth. This is already occurring in the downtowns of Atlanta, Austin, Orlando and Phoenix.

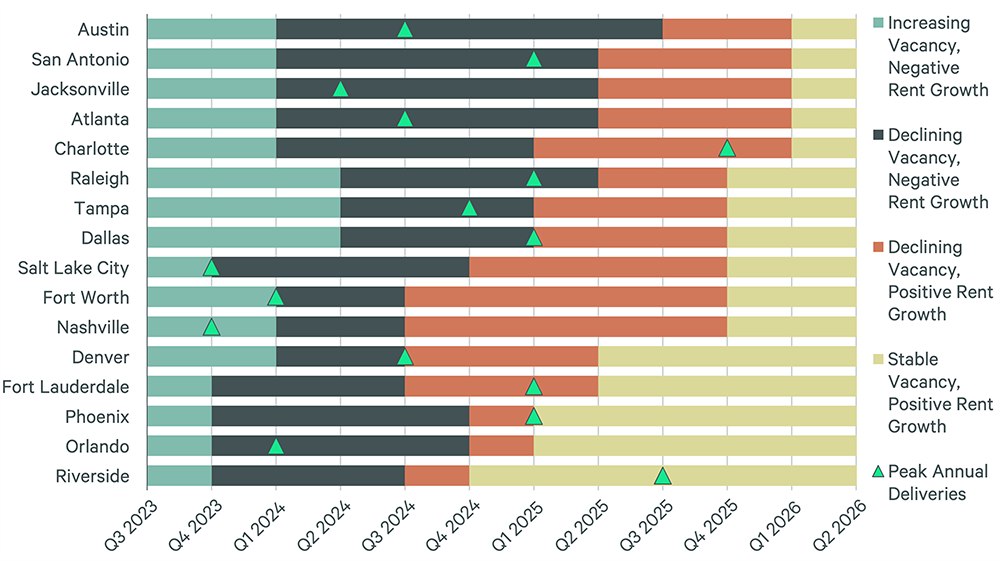

Figure 2: Recovery timeline for high-supply markets with negative rent growth

New supply puts upward pressure on vacancy rates and on landlords to compete for tenants based on price. Rent discounts have been highest in Sun Belt and Mountain markets as unprecedented in-migration in recent years induced developers to add new supply. However, vacancy rates have now peaked in many of these markets as renter demand exceeds new supply growth.

Nearly all high-supply markets with negative rent growth are expected to see positive rent growth and stable vacancy rates by mid-2025. The exception is Austin, where the sharp increase in new suburban supply will likely sustain negative rent growth until Q3 2025.

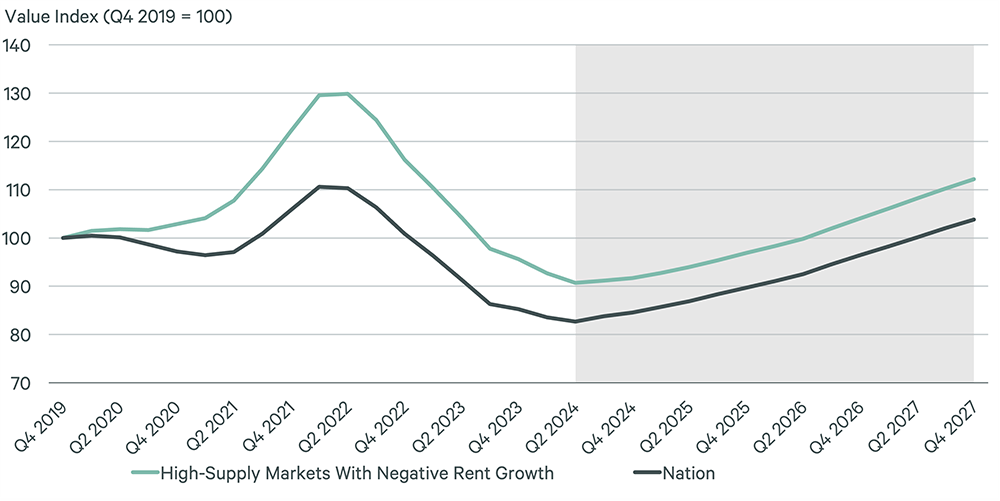

Figure 3: Multifamily value index forecast by market segment

Overall multifamily property values also appear to have stabilized and capitalization rates are expected to fall soon after the Fed begins cutting interest rates. As higher multifamily occupancy rates lead to rent growth, multifamily property values will continue to climb. There is now light at the end of the tunnel for markets with the highest supply and most negative rent growth, some of which are poised to set the pace of the recovery in multifamily values.