Intelligent Investment

2026 North American Data Center Investor Intentions Survey

April 21, 2026 3 Minute Read

Executive Summary

- More than half of investors recently surveyed by CBRE expect to increase their capital allocations to data centers this year by as much as 10%.

- Fifty-five percent of surveyed investors said they will increase their data center buying activity by more than 10%.

- Over 50% of respondents have investments in turnkey-wholesale, turnkey-hyperscale and powered-shell centers.

- For the third consecutive year, power availability was cited as the top challenge facing the data center industry.

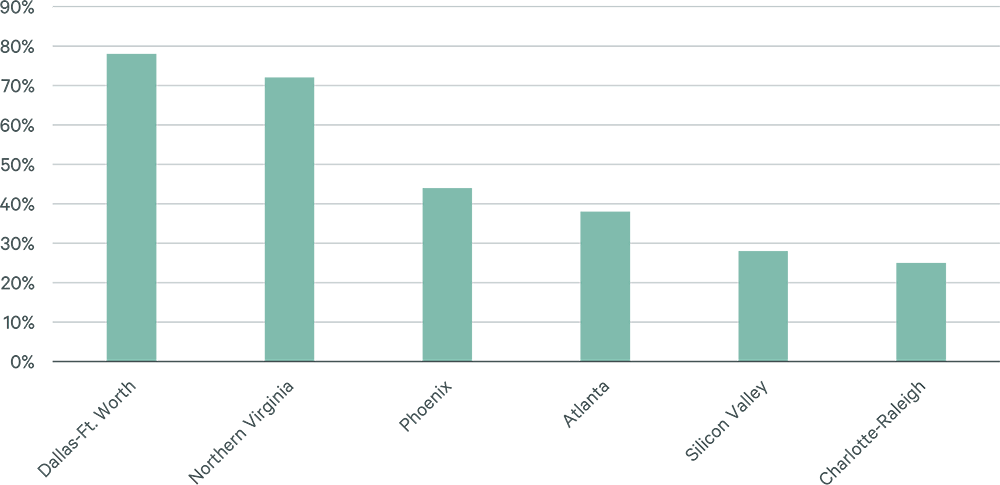

Top Markets

Dallas-Ft. Worth is the most attractive market for 78% of data center investors this year, slightly edging out Northern Virginia (72%). Dallas-Ft. Worth offers land availability, a deregulated electricity market, competitive power costs, robust fiber infrastructure and limited natural disaster risks. It will be interesting to see if the many large data center development projects in the planning stages will be delivered, which could propel Texas ahead of Northern Virginia as North America’s largest data center market by 2030.

More broadly, data center developers continue to prefer 250+ megawatt (MW) projects on a single parcel of land with power delivery by 2028. A large majority of the 10 most attractive markets for investors offer state tax incentives, land availability and relatively low power costs.

Figure 1: Top North American Markets for Investors

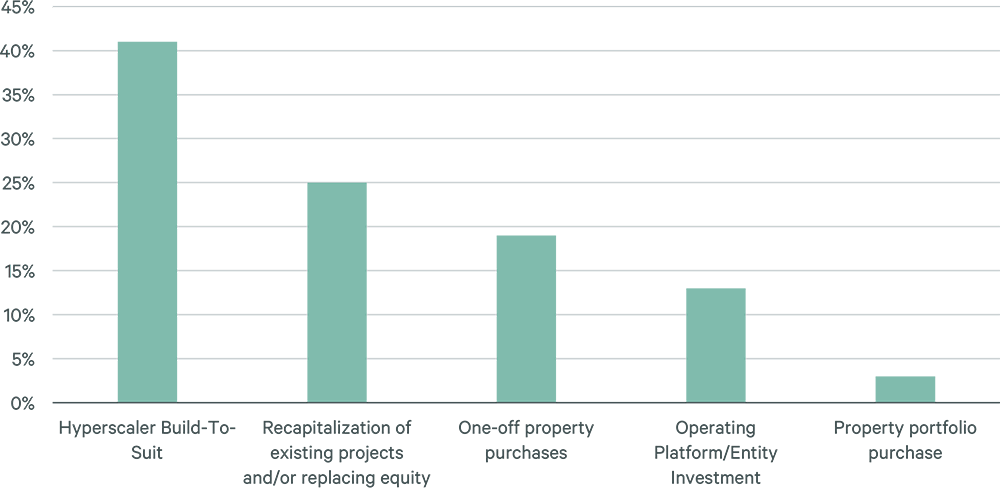

Top Opportunities for Investment

Major cloud-service providers continue to drive growth of the data center industry. Primary markets grew their total inventory by 36% last year and 34% in 2024. Build-to-suit hyperscale projects remained the most popular investment opportunity for data center investors over the next 12 to 24 months, cited by 41% of survey respondents. Recapitalization of existing projects and/or replacing existing equity was the second most popular opportunity.

Figure 2: What is the greatest opportunity for investment over the next 12-24 months?

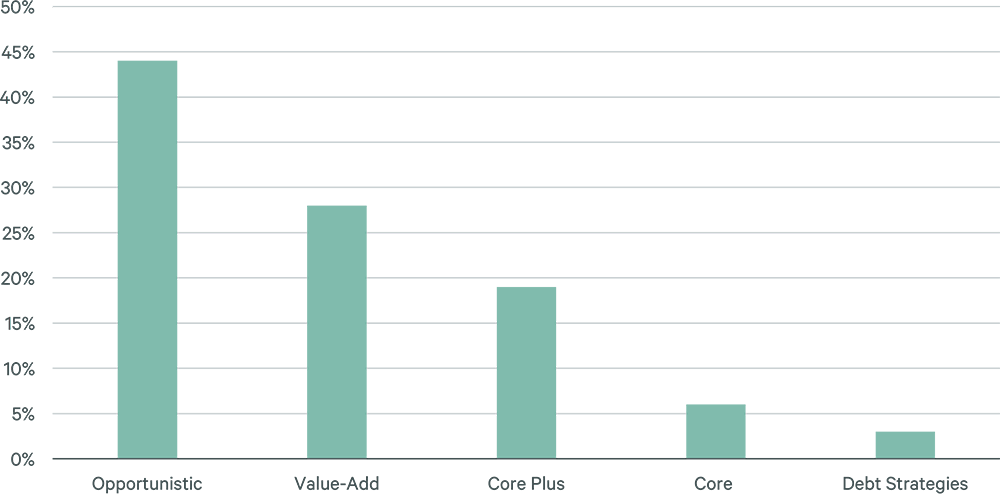

Strategies & Property Types

Opportunistic new development was the most attractive strategy for 44% of surveyed investors. Value-add strategies were most attractive for 28%, up from 15% in the 2025 survey. There are several key questions that investors will need to answer as they consider retrofitting older, legacy assets. As data center servers continue to change and require increased power density, landlords will need to determine whether retrofitting old assets will allow for premium rents. Investors also should consider whether Edge sites—small-scale data centers close to urban business districts and end-users—will be particularly attractive. Other considerations include whether data center operators should generate their own electricity on site rather than rely on the traditional power grid.

Figure 3: Most Attractive Investment Strategies for 2026

Cost of Capital Uncertainty

More than 80% of survey respondents cited strong occupier demand as the leading tailwind for the data center industry this year. Nearly 60% also cited lower debt costs as a potential tailwind. However, since the survey was conducted, the 10-year Treasury yield has increased by as much as 30 basis points amid the conflict in the Middle East. We expect that long-term interest rates will ease later in the year, assuming the conflict winds down.

Figure 4: Leading Tailwinds for Data Center Investors

Related Insights

-

With record low vacancy, mounting power constraints and limited new deliveries, the race for data center capacity is intensifying.

-

Despite uncertainty, growth will continue for the U.S. commercial real estate market in 2026.

-

Investor demand for data centers is surging, fueled by AI growth, rising capital allocations, and a shift toward high-risk, hyperscale strategies.

Data Center Solutions

Contacts

Pat Lynch

Executive Managing Director, Data Center Solutions

Kevin Aussef

President of Private Investor, Capital Markets

James Millon

President and Co-Head of Capital Markets, U.S. & Canada