Adaptive Spaces

Aging Population Fuels Greater Demand for Specialty Healthcare Real Estate

March 26, 2026 4 Minute Read

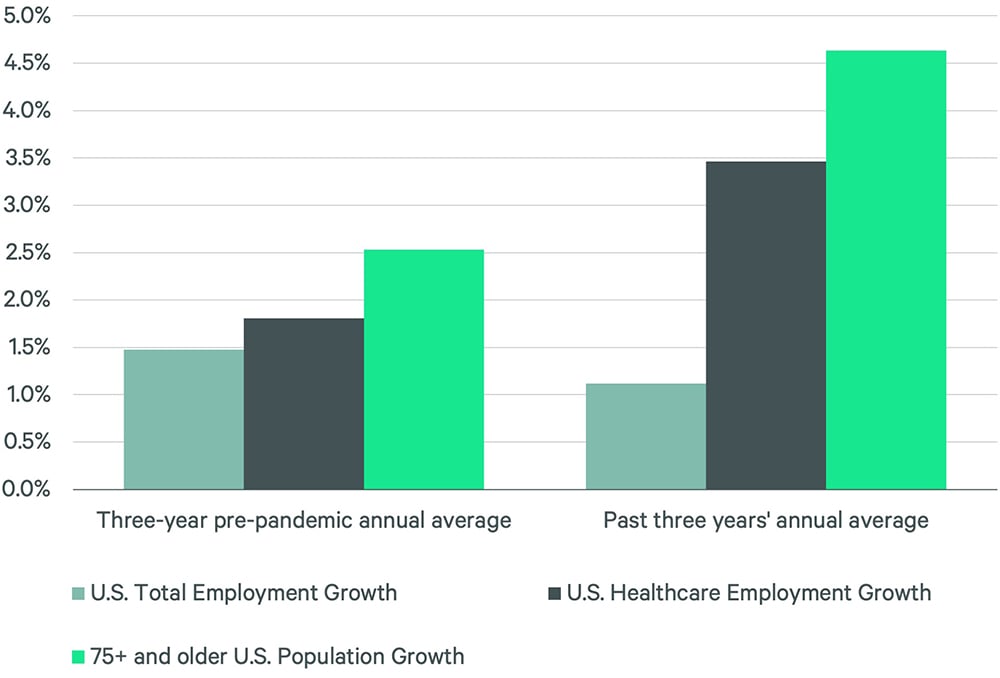

An aging U.S. population has contributed to unusually robust healthcare job growth over the past three years that, in turn, has caused surging demand for various healthcare facilities.

Since March 2023, the U.S. healthcare industry has created jobs at three times the rate of the overall economy, a sharp escalation from the three years prior to the pandemic. Much of this can be attributed to a 4.6% annual increase in Americans aged 75 and older over the past three years versus a three-year pre-pandemic annual average of 2.5%.

Figure 1: U.S. Job & Senior Population Growth

Healthcare real estate is adapting to this accelerated demand, underpinned by insurance reimbursement pressures, convenience for patients and new technologies. These factors are leading to a more decentralized healthcare-delivery system with a rise in outpatient facilities.

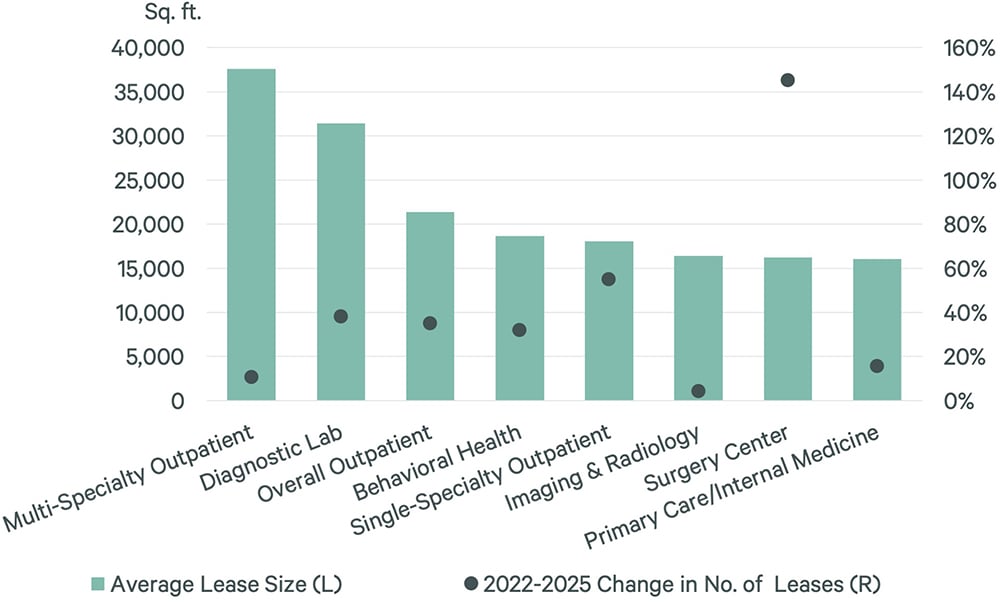

A CBRE analysis of hundreds of leases signed over the past several years reveals that some healthcare segments are driving demand for space disproportionately.

Figure 2: Average Lease Size & Change in No. of Leases by Occupier Type

Figure 2 shows the growth in the number of leases for outpatient facilities by occupier type between 2022 and 2025, along with the average lease size. Surgery centers saw the most growth, with the number of leases up by 145%. Healthcare systems have embraced outpatient surgery centers for their convenience, cost-efficiency and cutting-edge technologies.

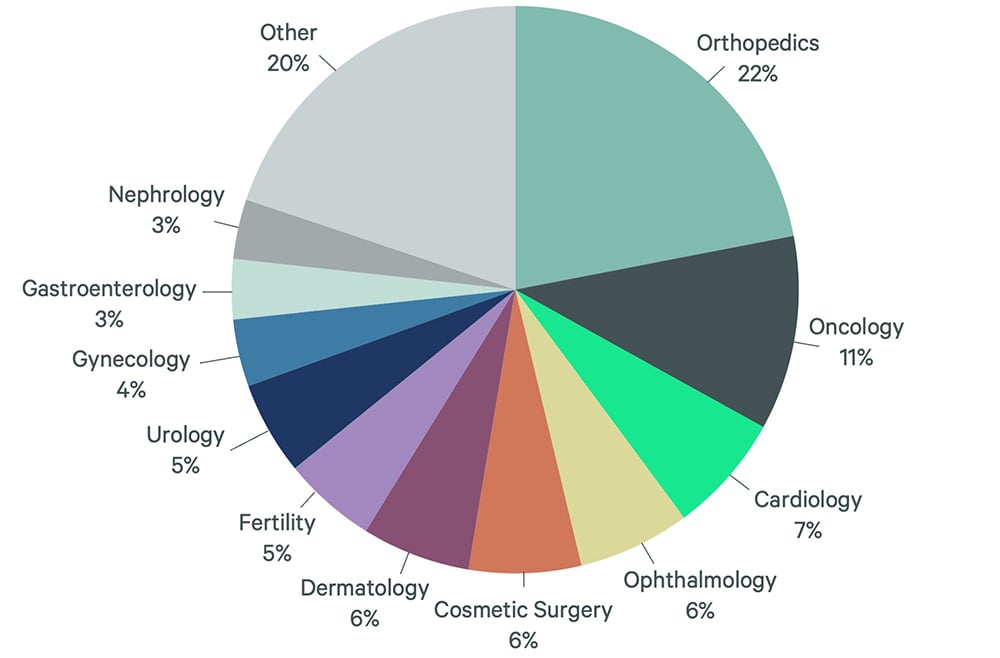

Figure 3: Single-Specialty Leases Signed by Occupier Type Between 2022 & 2025

Leases signed by single-specialty occupiers rose by 55% between 2022 and 2025, based on demand for orthopedics, oncology, fertility services and other high-demand specialties. Figure 3 shows the composition of specialties driving the increased demand for this property type.

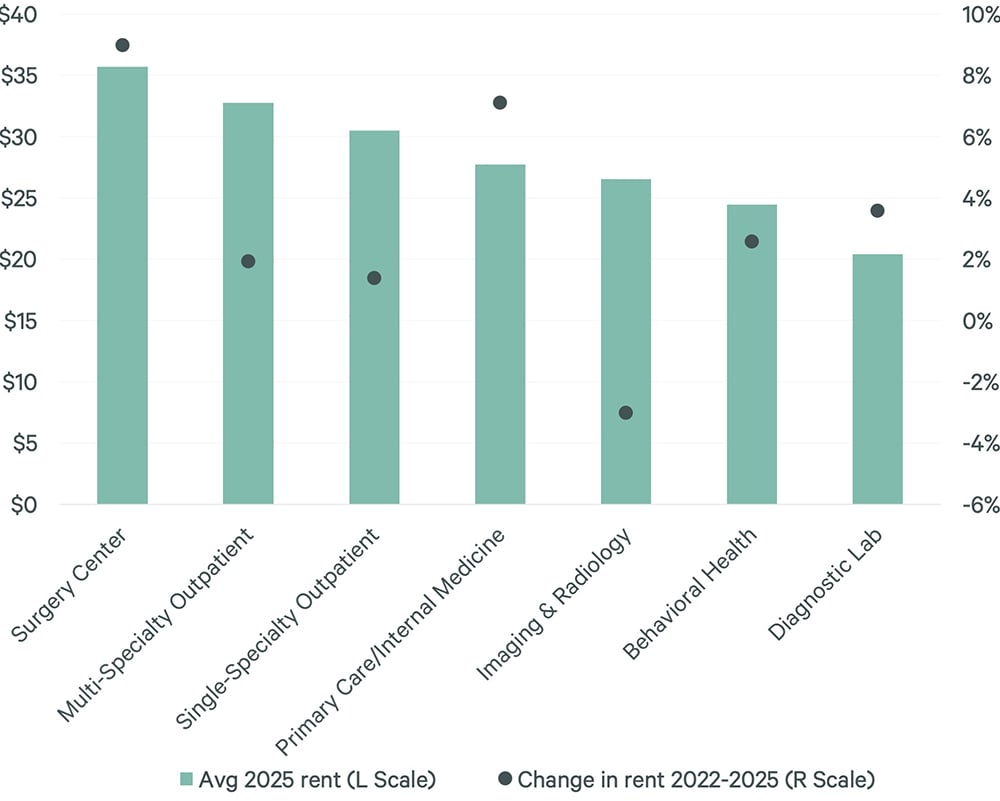

Increases in the number of leases by other occupier types between 2022 and 2025 include 38% for diagnostic labs, 32% for behavioral health providers, 16% for primary care/internal medicine specialists and 11% for multi-specialty outpatient providers. Imaging & radiology occupiers posted the slowest growth of 4% over the same period.

Figure 4: Average Rent & Change Between 2022 and 2025

Partly due to their unique infrastructure needs, surgery centers have seen the greatest rent escalations over the past three years. Other users like behavioral health providers and specialty practitioners, which can be accommodated in conventional office space, have seen more measured rent growth. Rents can vary based upon the occupier’s specific use. For example, higher-acuity and resource-intensive users like surgery centers and multi-specialty providers are more likely to have triple-net leasing arrangements and higher rents.

We expect recent trends in outpatient real estate demand to persist in the near term. However, as the drivers of healthcare demand evolve, so will healthcare real estate. While adaptable and purpose-built medical facilities will remain prevalent within many institutional medical portfolios, competitive leased space allows for the quick deployment of services in an industry where evolving technology and policy are driving dynamic healthcare real estate strategies.

Related Insights

-

Despite uncertainty, growth will continue for the U.S. commercial real estate market in 2026.