Intelligent Investment

As Obsolescence Plagues Malls, Neighborhood Centers Remain Resilient

Chart of the Week

January 8, 2024 2 Minute

Receive EA Insights Directly in your Inbox

Lifestyle & Mall availability rates have been bouncing around the 5% to 6% range for the past several years. While this is higher than the sub-3% rates that were typical prior to the Global Financial Crisis, current availability is not as bad as the scores of “dead” malls throughout the suburbs might suggest.

A key factor may be that nearly half of the vacant Lifestyle & Mall space is obsolete and no longer available for lease, so no longer part of the competitive inventory. The good news is that the many healthy, high sales-per-square-foot malls face less competition from weaker centers.

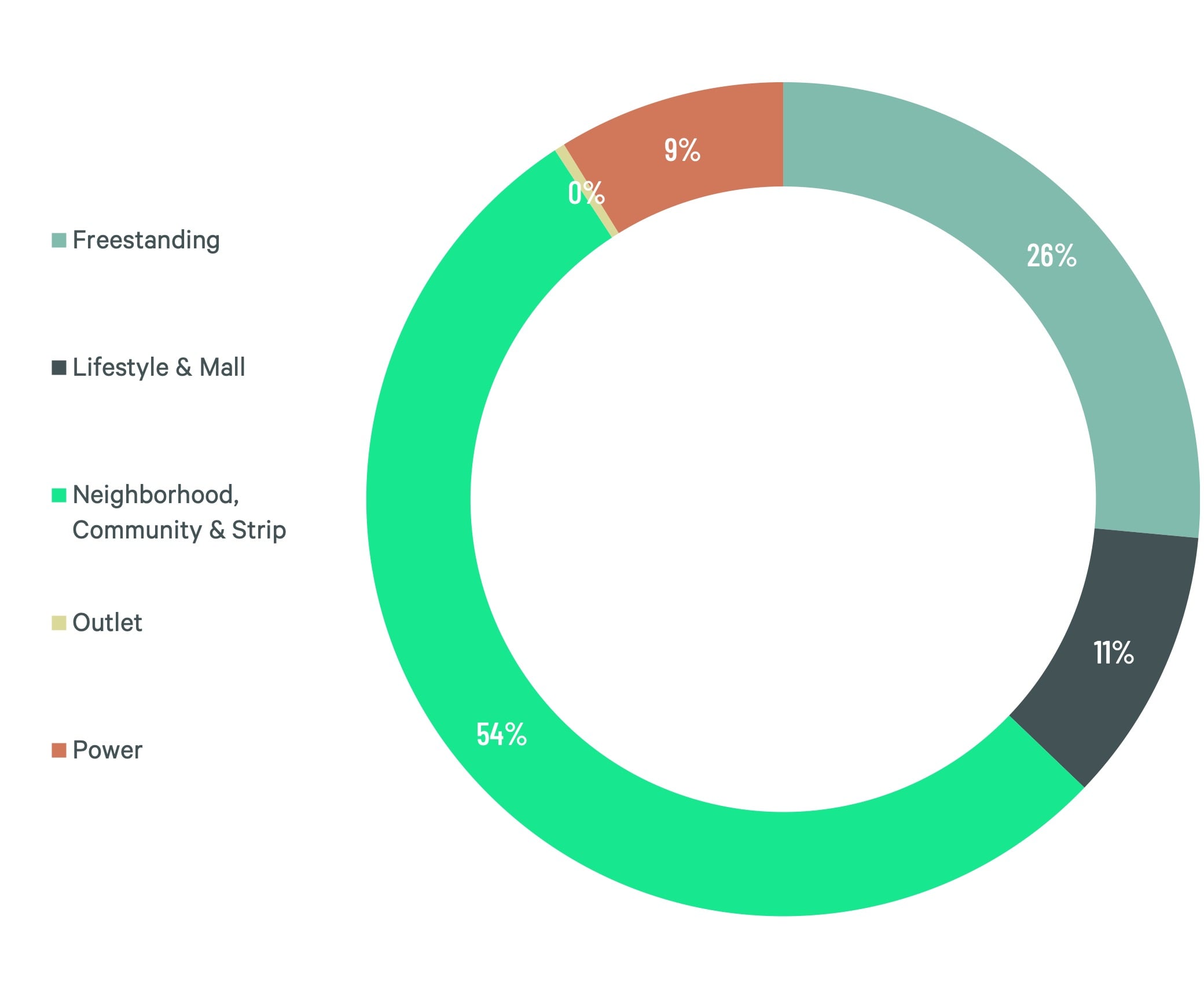

Trends in the regional mall space are a stark contrast from Neighborhood, Community & Strip Centers, where vacancy rates today are lower than in the 2000s due to the years-long pause in new construction. Moreover, there are fewer “dead” centers with over half (54%) of the empty space still part of the total inventory. Steady demand for Neighborhood, Community & Strip Centers, combined with a very thin construction pipeline, will keep availability relatively tight.

Figure 1: Share of Retail Space that is Vacant but NOT Available

Figure 2 : Share of Retail Space that is Vacant AND Available

Let's Talk

Dennis Schoenmaker, Ph.D.

Global Head of Forecasting and Strategic Insight, Head of Data Centre of Excellence