Intelligent Investment

Inflation and Commercial Real Estate: a more nuanced relationship than often portrayed

November 7, 2022

Receive EA Insights Directly in your Inbox

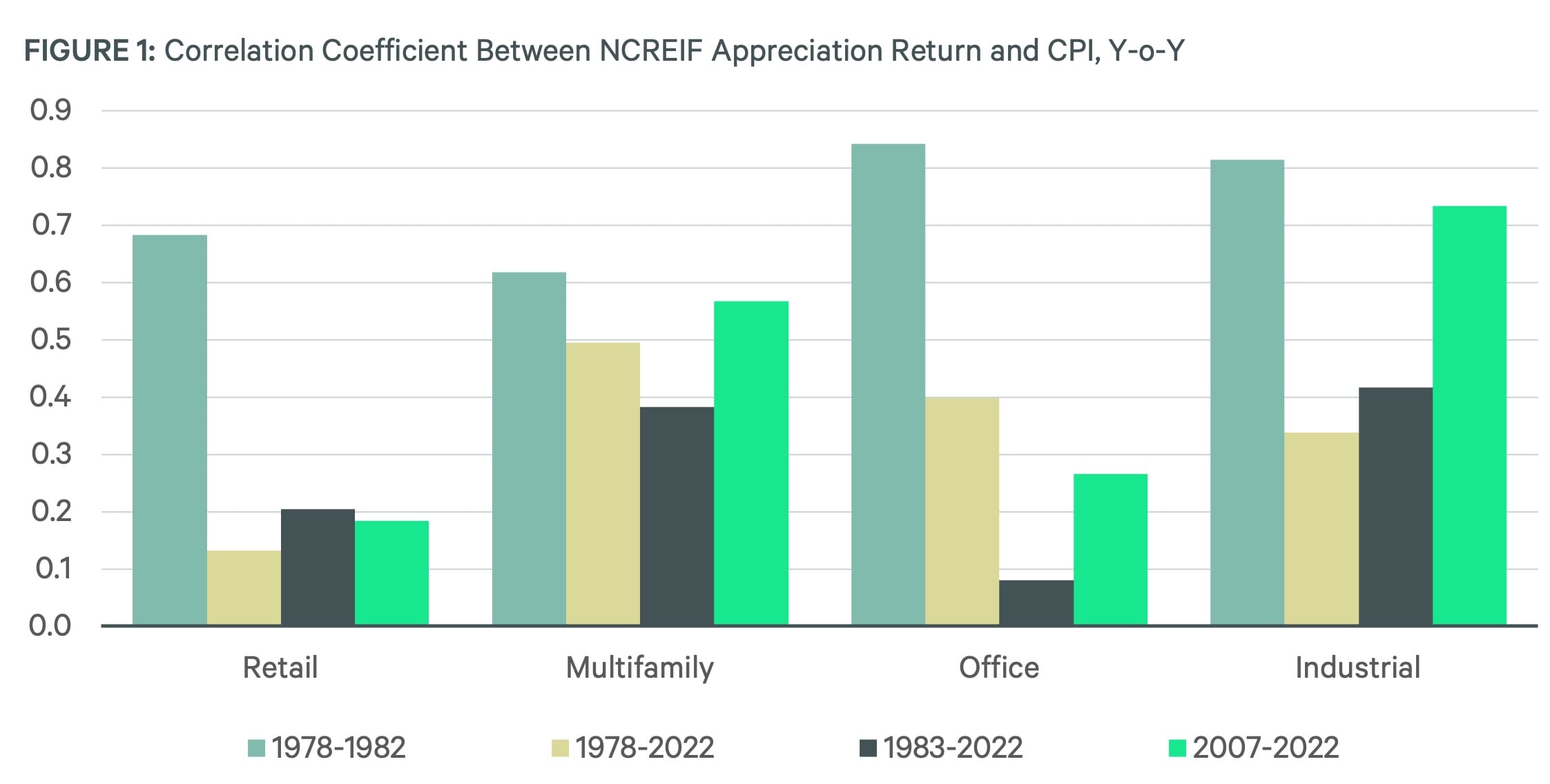

Commercial real estate is often thought of as a reliable inflation hedge. Perhaps this reputation grew from the early days of the NCREIF Property Index (NPI), when all property types saw sturdy value growth between 1978 and 1982, amid surging inflation. However, market fundamentals were tight during these years, likely contributing as much to rising property values as inflation did.

Since 1983, value growth has been markedly less correlated with CPI changes and since 2007, macroeconomic trends have trumped inflation as a driver of property values. Over the past 15 years, multifamily and industrial appreciation returns have been bolstered, respectively, by high rental household formation and the emergence of e-commerce. Conversely, e-commerce has negatively affected retail and changes in space utilization (e.g., less space per worker) has taken a toll on office. Changes in values across property types appears to be more sensitive to these macro trends than to CPI.

This evidence suggests real estate’s ability to hedge inflation is not a foregone conclusion. Each cycle is different, and each property type will respond to macro trends in different ways.

Source: NCREIF, U.S. Bureau of Labor Statistics, CBRE Econometric Advisors

Since 1983, value growth has been markedly less correlated with CPI changes and since 2007, macroeconomic trends have trumped inflation as a driver of property values. Over the past 15 years, multifamily and industrial appreciation returns have been bolstered, respectively, by high rental household formation and the emergence of e-commerce. Conversely, e-commerce has negatively affected retail and changes in space utilization (e.g., less space per worker) has taken a toll on office. Changes in values across property types appears to be more sensitive to these macro trends than to CPI.

This evidence suggests real estate’s ability to hedge inflation is not a foregone conclusion. Each cycle is different, and each property type will respond to macro trends in different ways.

Source: NCREIF, U.S. Bureau of Labor Statistics, CBRE Econometric Advisors

Let's Talk

Dennis Schoenmaker, Ph.D.

Global Head of Forecasting and Strategic Insight, Head of Data Centre of Excellence