Intelligent Investment

Larger warehouses feeling the pinch from occupier cutbacks and spirited new construction

Chart of the Week

August 31, 2023

Receive EA Insights Directly in your Inbox

Some logistics occupiers, especially general merchandisers, e-commerce companies and home-improvement retailers, are cutting their space commitments. This is resulting in an uptick in sublease space, particularly for warehouses larger than 300,000 sq. ft., just as the market is trying to absorb a spate of new development. In contrast, infill assets, generally smaller than 100,000 sq. ft., have not seen as much availability growth due to continued occupier appetite for last-mile fulfillment centers and an absence of extensive development of assets in this size range.

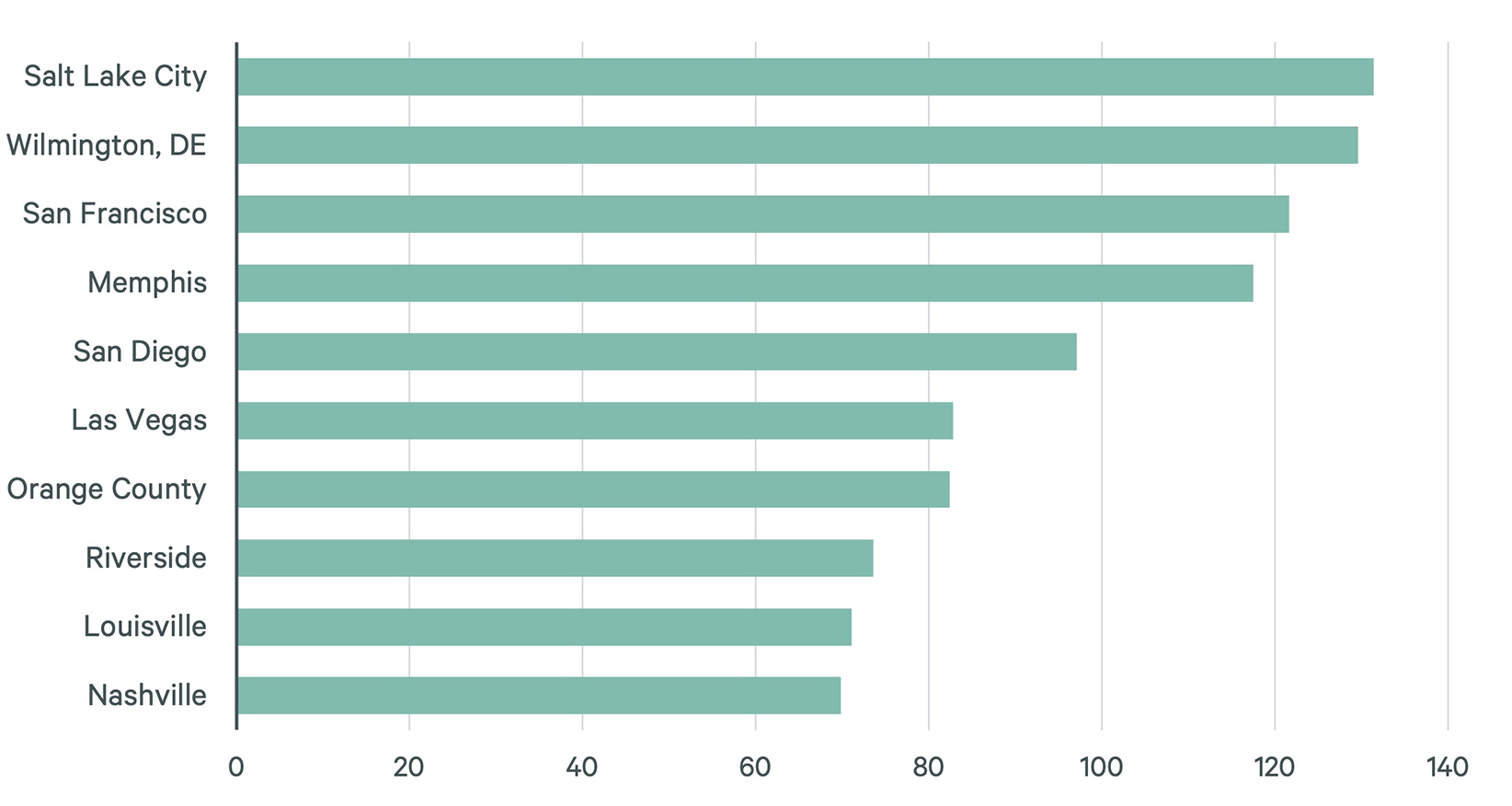

In total, 115 million sq. ft. is available for sublease today, twice as much as at year-end 2021. Figure 1 shows the 10 markets where sublease availability has grown the most this year. Three of the markets are in Southern California, perhaps reflecting weaker shipping activity. Major Midwest logistics hubs, such as Memphis and Louisville, are also feeling pressure.

Overall, logistics market conditions remain very tight. However, occupier retrenchment at a time of robust new construction is pushing availability in some markets back toward historical averages.

Figure 1: Basis-Point Change in Sublease Availability Rate (Q2 2022 - Q2 2023), Top 10 Markets

Source: CBRE Econometric Advisors.

Let's Talk

Dennis Schoenmaker, Ph.D.

Global Head of Forecasting and Strategic Insight, Head of Data Centre of Excellence