Intelligent Investment

The 1990s offer solace from today’s office pains

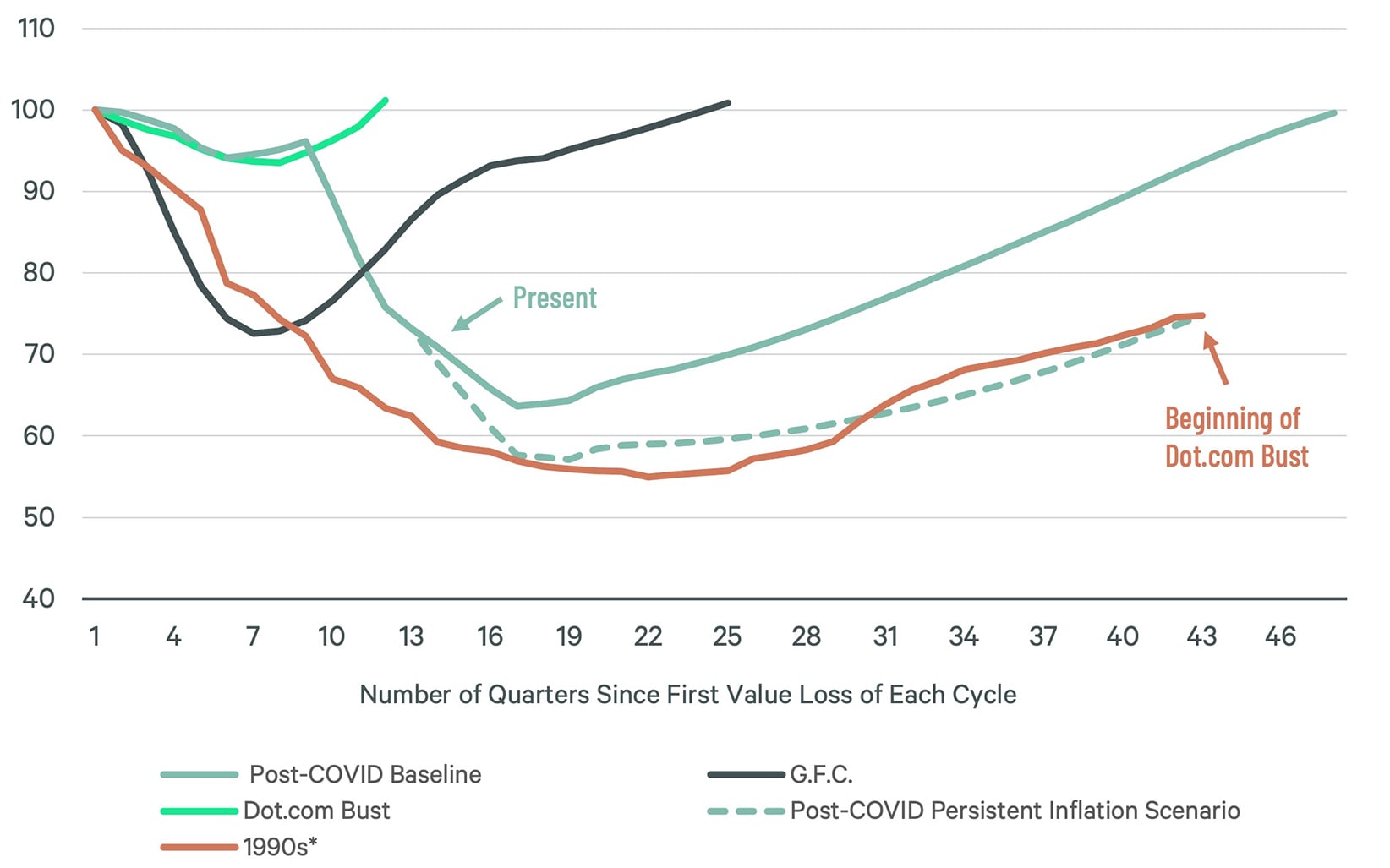

Chart of the Week

June 6, 2023

Receive EA Insights Directly in your Inbox

The office sector always has its ups and downs. Market cycles are heavily influenced by speculative development, in-place rents that roll over to market rates and macroeconomic forces, notably changes in finance and tech employment.

Every market cycle is different, as Figure 1 illustrates. The dot-com downcycle was the mildest in recent history as most of the pain was confined to a few markets. Also, elevated cap rates quickly attracted capital back to commercial real estate as the economy recovered.

Today’s downturn is much rougher, already stretching to 13 quarters, but it is not unprecedented. The steep 1990s downcycle was arguably worse and followed a trajectory that is similar to CBRE Econometric Advisors’ Downside scenario under which the Federal Reserve continues to aggressively raise interest rates.

The office market has been on its back before. Past experience tells us the preconditions to recovery include a throttling back of the new supply pipeline and painful distress sales that provide necessary price signals. Both of these are happening now. We expect office valuations to find a floor by early 2024 in our Baseline scenario before a new, long upcycle commences, led by prime buildings in “live-work-shop” submarkets.

Figure 1: Capital Value Index, 100 Equates to the Peak of Each Cycle

*This cycle is constructed from NCREIF NPI data

Source: CBRE Econometric Advisors, NCREIF.

Let's Talk

Dennis Schoenmaker, Ph.D.

Global Head of Forecasting and Strategic Insight, Head of Data Centre of Excellence