Intelligent Investment

Economic Watch: 50-bp Hike Signals Fed’s Resolve to Curb Inflation

December 14, 2022 3 Minute Read

Executive Summary

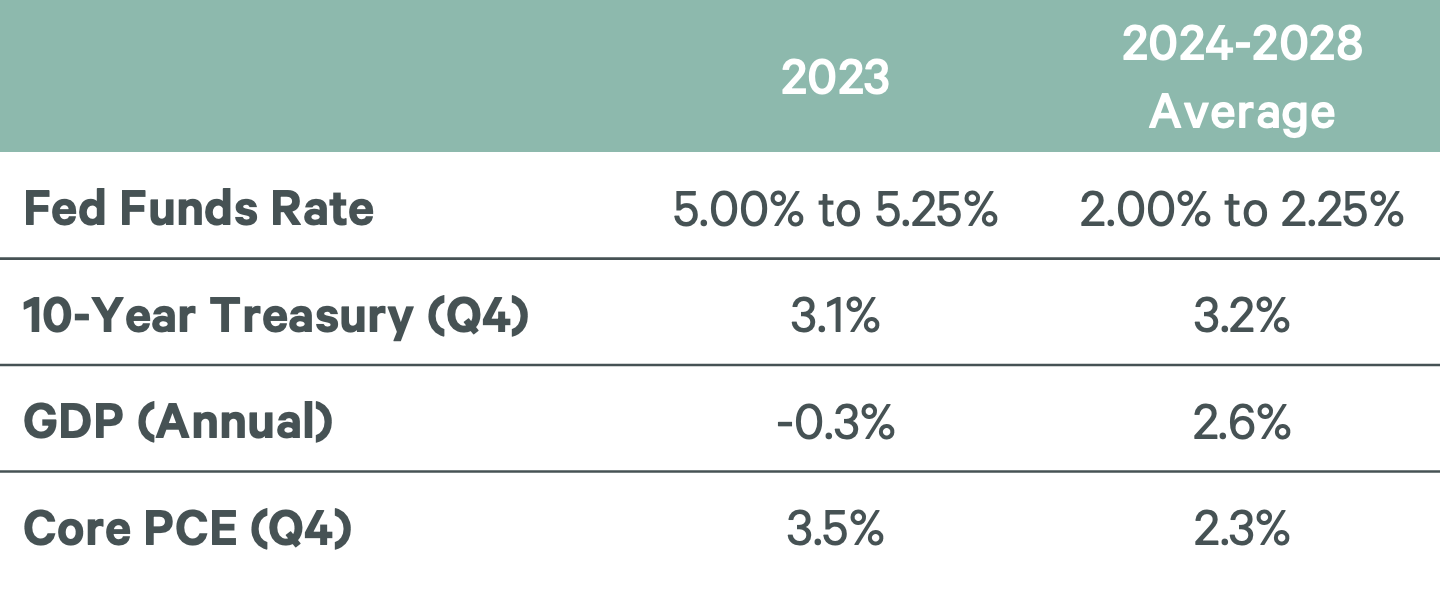

- The Federal Reserve raised the federal funds rate by 50 basis points (bps) today to a range of 4.25% to 4.5%.

- The Fed will continue to reduce its $8.6 trillion balance sheet by $95 billion per month, putting upward pressure on long-term interest rates and the cost of debt for real estate investment.

- The Fed forecasts that GDP growth will slow to just 0.5% next year and that core PCE (its preferred gauge of inflation) will end 2023 at 3.5%.

- The Fed also revised its interest rate outlook, which is now in line with CBRE’s expectations that the federal funds rate will peak at a range of 5% to 5.25% next year. Rising interest rates, along with CBRE’s expectation of a moderate recession in 2023, will limit real estate sales and leasing activity through the year.

December FOMC Meeting

The Federal Reserve increased the federal funds rate by 50 bps today to a range of 4.25% to 4.5% after four consecutive 75-bp increases. While another 50-bp hike is possible, we expect the Fed will move toward smaller increases of 25 bps in 2023. The Fed also signaled its continued quantitative tightening campaign of reducing its $8.6 trillion balance sheet by $95 billion per month.

While today’s rate hike was expected, the Fed took a more hawkish stance on the future level of interest rates due to persistent high inflation. The Fed now expects core PCE to end 2023 at 3.5% and the federal funds rate to peak at 5.1%, both higher than its earlier forecasts.

The Bottom Line

CBRE expects the federal funds rate will peak at a range of 5.00% to 5.25% next year, which along with quantitative tightening will slow economic growth. This, in addition to improved supply chains, will help to reduce prices. Lower inflation will give the Fed more flexibility to balance economic activity and price stability with smaller 25-bp rate increases next year.

The Fed’s monetary tightening will continue to limit capital markets activity in the near term and leasing activity will remain relatively subdued for most of 2023.

Figure 1: CBRE House View