Intelligent Investment

Economic Watch: Despite Lower Inflation, Quarter-Point Rate Hike Still Expected

July 12, 2023 1 Minute Read

Executive Summary

- The Consumer Price Index (CPI) rose by 3% year-over-year in June and 0.2% for the month, below consensus estimates of 3.1% and 0.3%. This was the lowest rate of inflation since March 2021.

- Core inflation, which excludes food and energy prices, rose by 4.8% year-over-year and 0.2% for the month. Services inflation has stabilized and is cooling in various areas.

- Housing (shelter) costs continue to largely keep annual inflation above the Federal Reserve’s 2% target.

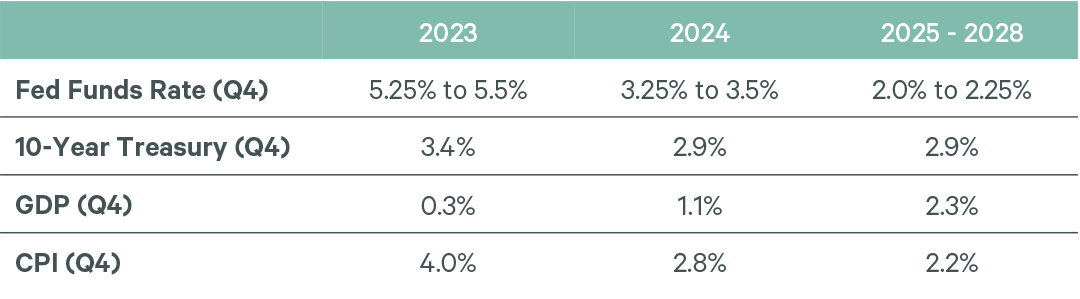

- We still expect that the Fed will increase the federal funds rate by another 25 basis points (bps) this month to a range of 5.25% to 5.50%, then hold them at that level through 2023.

The Bottom Line

Inflation increased by 3.0% year-over-year in June (0.2% for the month), the lowest rate since March 2021. The decline was driven by lower energy, airfare, food-at-home and used-car prices. Signs of cooling services inflation are also encouraging. Housing costs remained the primary contributor to inflation; however, we expect rent increases to continue easing in coming months. Core inflation, which excludes food and energy prices, rose by 4.8% year-over-year in June (0.2% for the month), remaining well above the Fed’s 2% target.

The large drop in June’s CPI in part reflects a reduction in energy prices, which had spiked last year due to the Ukraine war. We expect that inflation will continue to moderate but remain above the Fed’s 2% for the rest of 2023.

Even though inflation is easing, CBRE expects that the Fed will increase the federal funds rate by another 25 bps this month to a range of 5.25% to 5.50% to keep downward pressure on prices. We then expect that the Fed will hold rates at that level through 2023, resulting in a moderate recession later this year. As result, we do not anticipate that capital markets activity in the commercial real estate sector will improve until the first half of 2024, followed by improved leasing activity in the second half.

Figure 1: CBRE House View

Contacts

Insights in Your Inbox

Stay up to date on relevant trends and the latest research.