Intelligent Investment

Economic Watch: GDP Growth Slows in Q4 But Remains Relatively Strong

January 30, 2025 3 Minute Read

Executive Summary

- U.S. GDP increased by 2.3% on an annualized basis in Q4 2024, down from 3.1% in Q3 and below market expectations of 2.5%.

- For the full-year, GDP grew by 2.8% compared with 2.9% in 2023, still well above the 2.2% annual average since 2000.

- Above-average growth was accompanied by a 2.3% increase in the Personal Consumption Expenditures (PCE) Index in Q4, close to the Fed’s 2% target but up from 1.5% in Q3. The Core PCE Price Index, which excludes food and energy prices, increased by 2.5% in Q4 from 2.2% in Q3.

- CBRE expects relatively strong economic growth to continue in 2025, despite certain risks.

- We expect that inflation will moderate in 2025 and that the Fed will slow the pace of interest rate cuts.

The Bottom Line

Increases in consumer spending and government expenditures contributed to above-average GDP growth in Q4. Personal consumption expenditures increased by 4.2%—the strongest quarter since Q1 2023—while government spending rose by 3.2%. Non-residential investment fell by 2.2%. The U.S. trade deficit was a mild drag on growth, reflecting fewer exports due to weakness in the global economy and higher imports driven by the prospect of tariffs on certain foreign products.

Price increases should moderate toward the Fed’s 2% target in 2025, despite persistent service-sector inflation. Strong economic growth and the large federal budget deficit should keep the 10-year Treasury yield slightly above 4% throughout the year.

A modest increase in office leasing activity is expected this year, while industrial leasing will likely slow from 2024’s strong pace. Although long-term interest rates will remain a headwind for capital markets activity, commercial real estate investment volume is expected to improve this year.

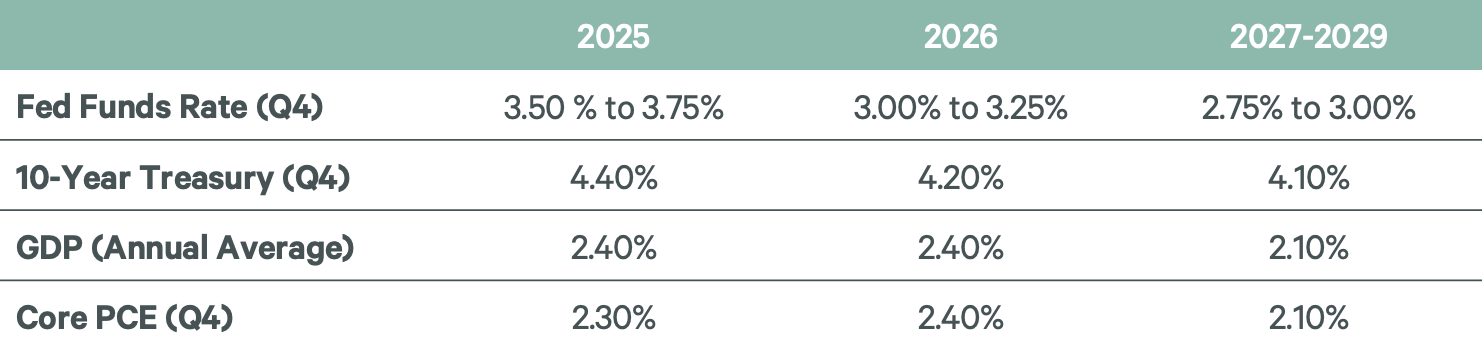

Figure 1: CBRE House View