Intelligent Investment

Economic Watch: Persistent Inflation Likely Delays Rate Cut to June

March 12, 2024 3 Minute Read

Executive Summary

- The Consumer Price Index (CPI) increased by 0.4% in February and 3.2% year-over-year. The monthly gain met expectations, while the annual rate was slightly above the 3.1% forecast. Shelter and gasoline accounted for most of the price increases.

- Core inflation, which excludes food and energy prices, rose by 0.4% for the month and 3.8% over the past year vs. respective expectations of 0.3% and 3.7%.

- We expect that February’s CPI reading will reinforce the Fed’s cautious approach to lowering interest rates and push the likelihood of an initial rate cut from May to June.

- Real estate investment activity will remain sluggish in the first half of 2024 amid bond market volatility and high interest rates before beginning to pick up in the second half.

The Bottom Line

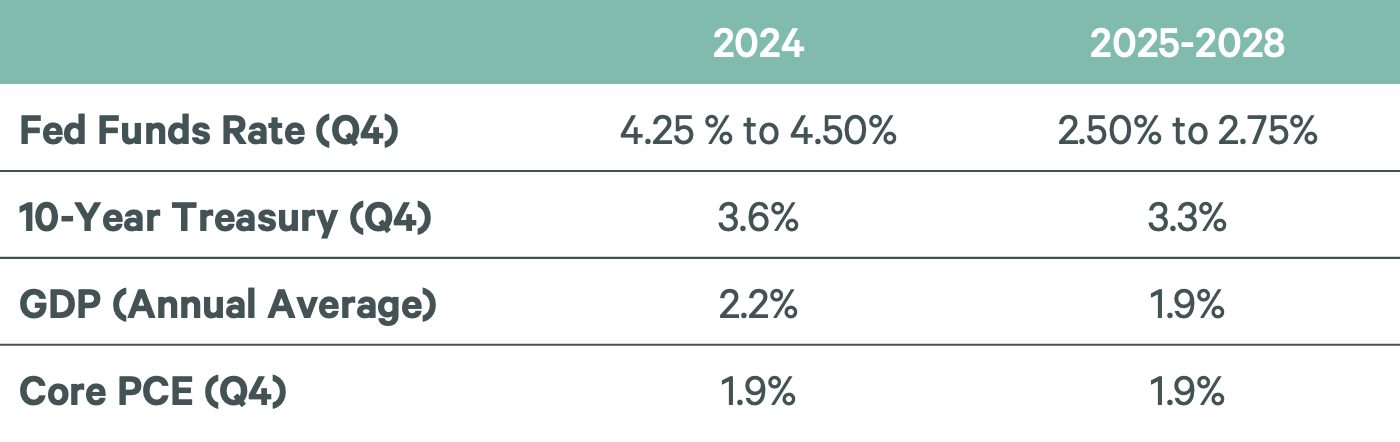

February’s higher-than-expected inflation reading delays the likelihood of an initial interest rate cut to June at the earliest. Core inflation remains elevated, primarily due to higher shelter costs, airfares, hotel rates and auto and medical insurance premiums. Although we expect continued volatility in monthly readings, inflation should gradually fall toward the Fed’s 2% target throughout the year. The 10-year Treasury yield also is expected to fall to the upper 3% range by year-end.

High interest rates and uncertainty about overall business conditions will continue to limit real estate investment activity in the first half of the year. We expect investment volume to pick up in the second half of the year once the Fed begins cutting rates and borrowing costs fall. A resilient economy will support leasing activity.

Figure 1: CBRE House View