Intelligent Investment

Economic Watch: Q2 GDP Beats Expectations Despite Aggressive Fed Tightening

July 27, 2023 3 Minute Read

Executive Summary

- U.S. GDP increased by 2.4% on an annualized basis in Q2 2023, above consensus expectations of 2%. Consumer spending and business investment were the main growth drivers.

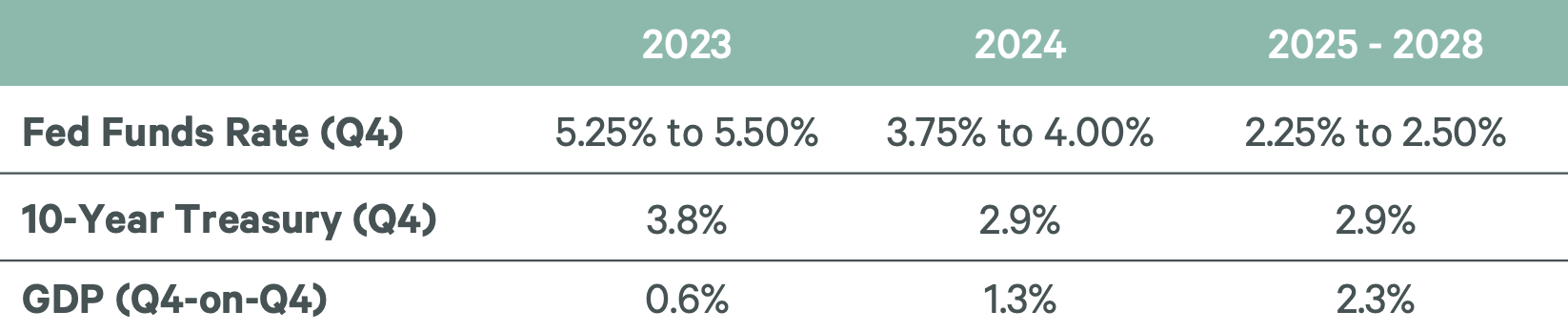

- Sustained growth and elevated inflation caused the Fed to increase interest rates by 25 basis points (bps) yesterday to a range of 5.25% to 5.50%. While another rate hike this year cannot be ruled out if the labor market remains tight and the economy stays strong, we do not expect the Fed will need to do so.

- CBRE expects economic growth will slow, reflecting higher interest rates, tighter credit conditions and diminished savings.

- Amid a weakening economy and tighter credit conditions, real estate capital markets and leasing activity will remain subdued in the near term. We expect investor sentiment to improve as the path for interest rates becomes clearer later this year. This should result in increased capital markets activity in early 2024, followed by a revival in leasing activity.

Q2 2023 GDP

U.S. GDP grew by 2.4% on an annualized basis in Q2 2023, above consensus expectations of 2%. Personal consumption rose 1.6%, reflecting strong consumer spending despite high inflation and rising interest rates. Business investment increased by 4.9% during the quarter (annualized), with companies spending on equipment and buildings. Overall, the economy, notably the consumer, has remained remarkably resilient but annualized growth in spending on both goods and services was lower than in Q1.

CBRE Forecast

High inflation and continued economic growth caused the Fed to increase interest rates by 25 bps yesterday to the highest level in 22 years. We expect the combination of higher rates, diminishing savings, tighter lending standards and the restart of student loan payments will weigh on consumers as the year progresses. This will cause GDP growth to slow during the second half of 2023, with the U.S. economy slipping into a short, moderate recession late this year.

Higher interest rates, tight credit conditions and economic uncertainty will limit commercial real estate activity. We do not expect capital markets activity to pick up across the board until early 2024, with leasing activity likely to begin recovering by midyear.

Figure 1: CBRE House View