Intelligent Investment

Fed Still Expected to Hold Rates Steady, Despite August Inflation Uptick

September 13, 2023 2 Minute Read

Executive Summary

- The Consumer Price Index (CPI) rose by 0.6% in August or 3.7% year-over-year, in line with consensus estimates of 0.6% and 3.6%, respectively.

- Headline inflation was largely driven by energy prices, particularly gasoline, and represents the largest jump in prices this year.

- Core inflation, which excludes volatile food and energy prices, rose by 0.3% month-over-month, slightly more than expectations of 0.2%. On a year-over-year basis, core inflation was up 4.3%, as expected.

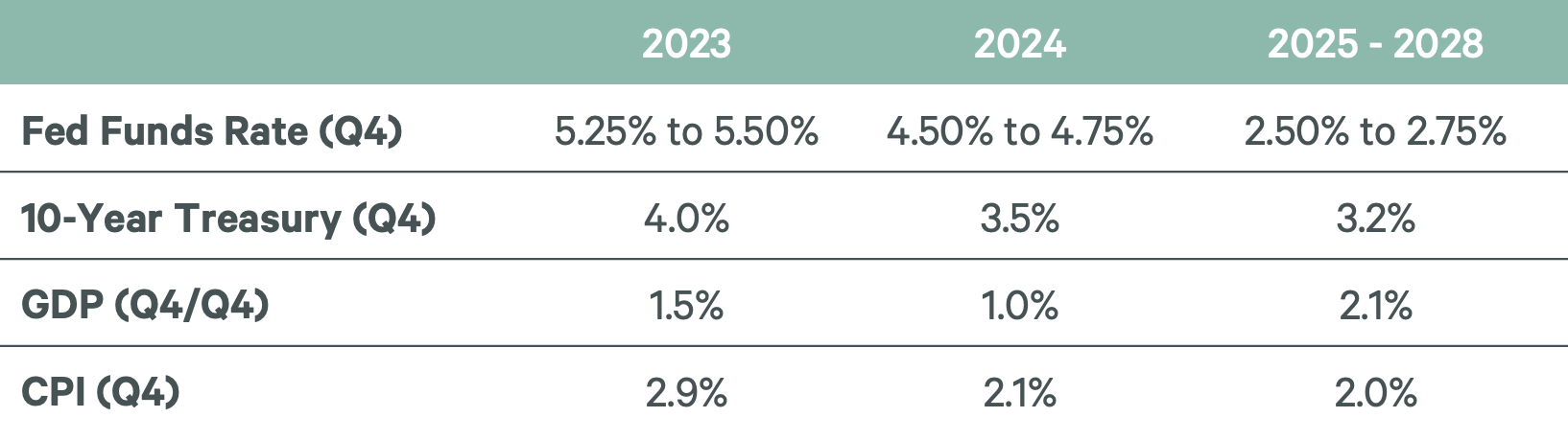

- CBRE expects that the Federal Reserve will hold rates at the current level (5.25% to 5.50%) when it meets next week. Still, today’s report keeps alive the possibility of another rate hike in November or December if inflation continues to increase more than expected.

- CBRE continues to believe investment activity will remain subdued for the rest of 2023, and begin to recover in the first half of 2024.

The Bottom Line

The CPI rose at its fastest monthly pace of the year—up 0.6%, pressured by higher gasoline prices. Core inflation, which excludes volatile food and energy prices, rose 0.3% for the month, slightly more than expectations of 0.2%.

Elevated rental housing costs continued to stoke high core inflation, but this pressure should lessen as the year goes on. Over the past three months, core inflation is up just 2.4% on an annualized basis. While this is above the Fed’s 2% target, it reflects significant progress in lowering price pressure since core inflation peaked at 6.6% in September 2022.

Today’s CPI report supports our view that the Fed will hold rates steady when it meets next week and is likely done with hikes for this cycle. However, today’s report keeps alive the possibility of one more rate increase later this year. Still, we expect the economy will slow in the fourth quarter, helping to keep a lid on inflation and allowing the Fed to hold rates steady.

Commercial real estate investment activity is unlikely to improve until capital sources are confident that interest rates have stabilized. We believe investors will gain such confidence in the fourth quarter, setting the stage for a recovery of sales volumes in the first half of next year. A leasing market rebound will follow the capital markets recovery and is dependent on an improved economic outlook.

Figure 1: CBRE House View