Intelligent Investment

Leasing of Sublease Space Gains Momentum, but Availability Grows in Q1 2022

May 3, 2022 2 Minute Read

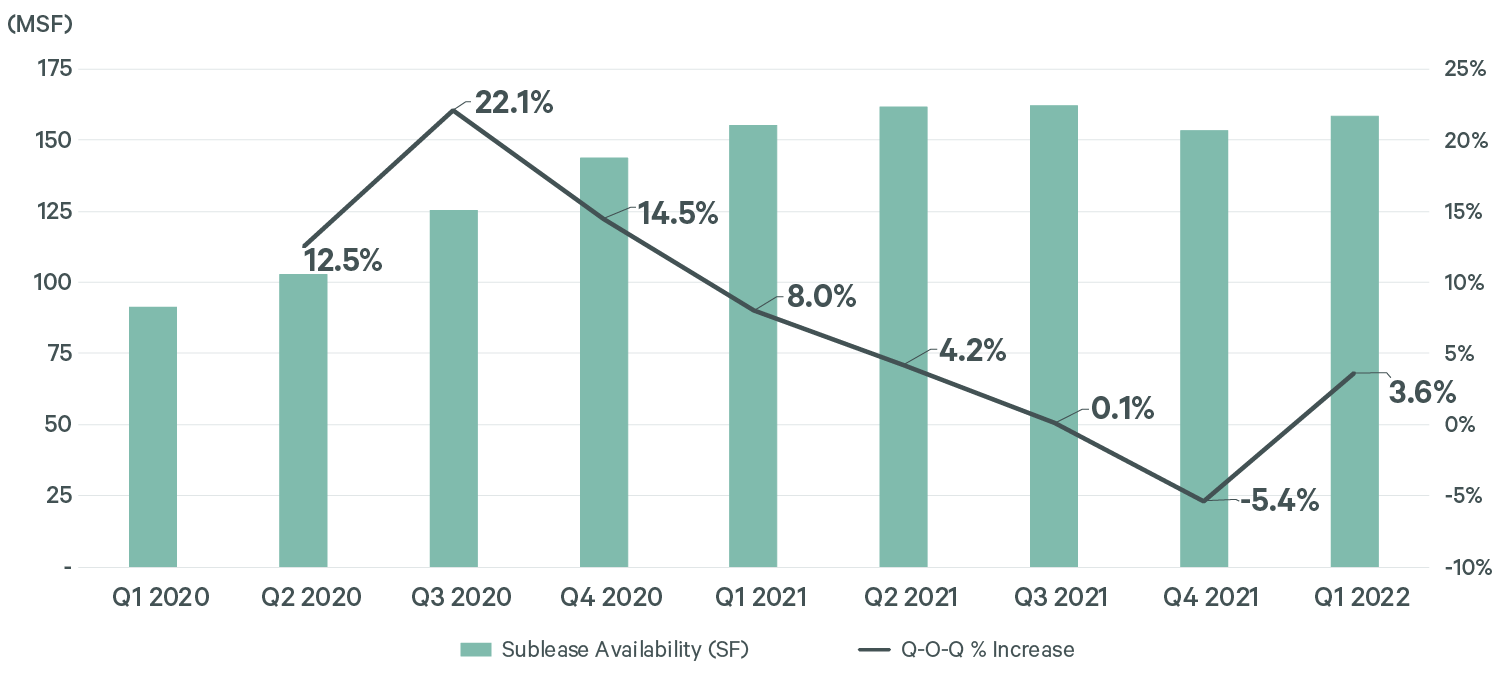

U.S. office sublease availability began to rise again in Q1 2022. During the second half of 2021, sublease space nationally fell by 5.4% as some occupiers took advantage of its economical pricing. However, sublease availability increased 3.6% in Q1 2022, even though price-conscious tenants continued to lease up sublease space at an impressive clip.

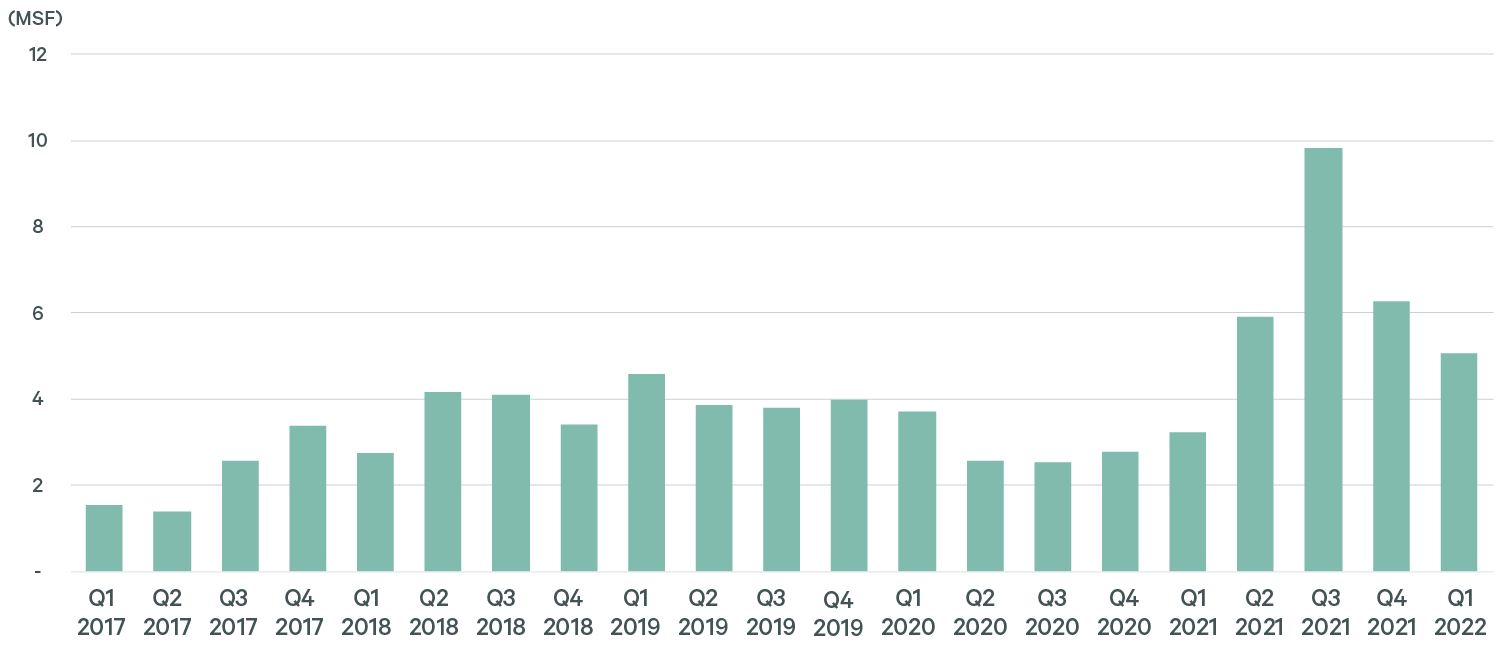

The leasing of sublease space rose 60% year-over-year in Q1 2022, the most activity of any other first quarter in the past six years. Historically, Q1s have the lowest amounts of subleasing activity of all other quarters. Therefore, Q1 2022’s surge in activity may be a harbinger of bigger quarterly increases later this year.

Figure 1: U.S. Office Sublease Activity by Quarter

Source: CBRE Research, Q1 2022.

While the pace of sublease space additions had been moderating over the previous six quarters, it increased to 159 million sq. ft. in Q1—slightly less than the peak of 162 million sq. ft. in Q3 2021.

Figure 2: U.S. Office Sublease Availability

Source: CBRE Research, Q1 2022.

While sublease availability remains above pre-pandemic levels in every major market, some of them are seeing modest improvements. Of the 20 largest markets, Boston, Denver and Seattle recorded the biggest Q1 2022 percentage reductions in their available sublease supply from Q3 2021, which was the pandemic-era peak for total U.S. sublease space. Minneapolis, Philadelphia and San Jose had the biggest increases, while Manhattan, San Francisco and Washington, D.C. had the most total available sublease space.

Figure 3: Sublease Availability by Major Metro Market

Source: CBRE Research, Q1 2022.