Creating Resilience

New Office Leasing Activity Rebounds in 2021

January 6, 2022 2 Minute Read

Office leasing activity1 rebounded in 2021 despite uncertainty posed by the delta variant. A preponderance of renewals in the last three quarters of 2020 during the height of pandemic-related restrictions gave way to more long-term commitments in the first three quarters of 2021. Although the omicron variant could cause short-term disruption, this data suggests that new leasing activity likely will continue to gain momentum as 2022 progresses.

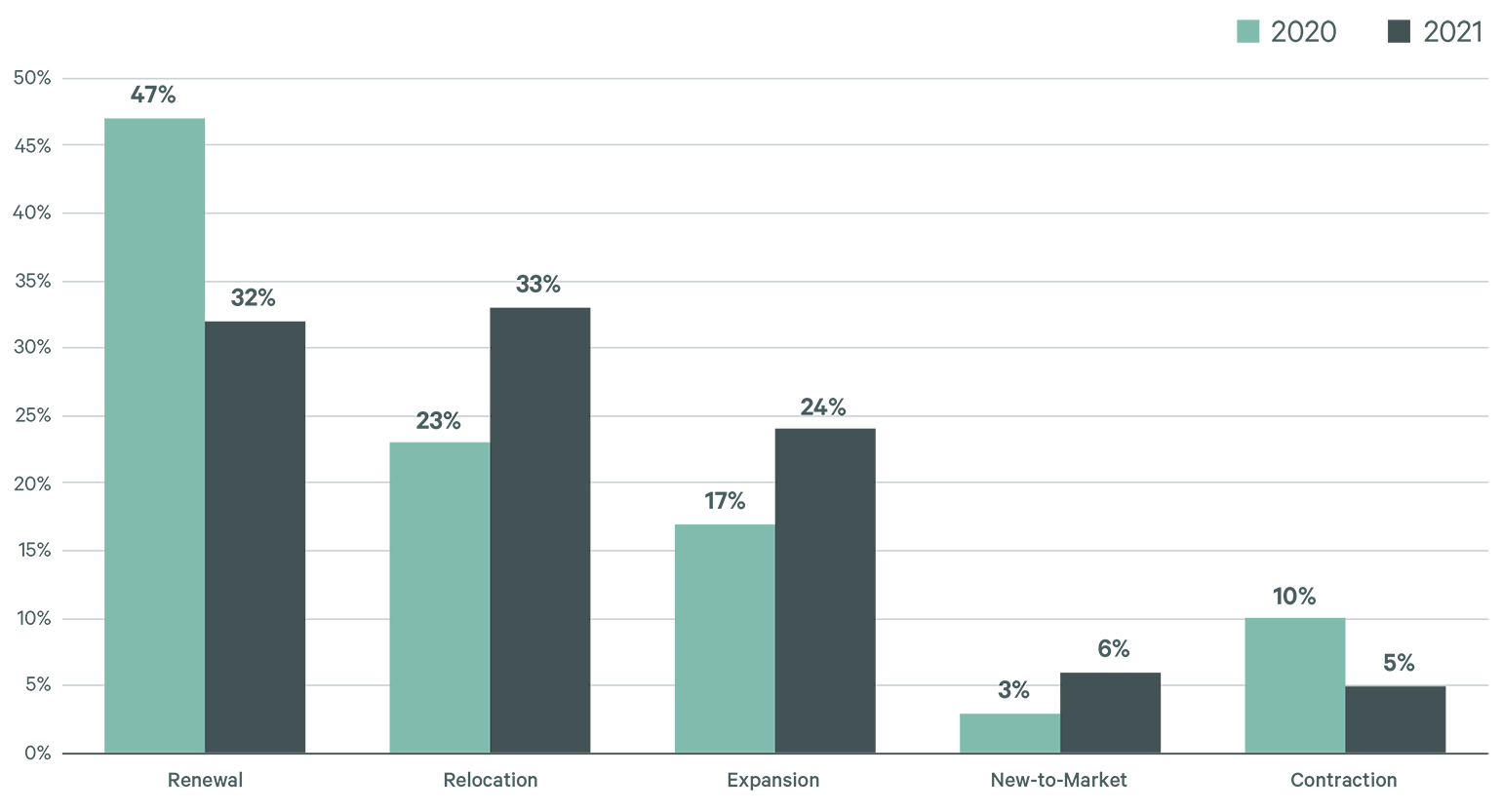

Figure 1: Office Leasing Activity by Transaction Type in Primary Markets

Source: CBRE Research, Q3 2021

Primary markets2 saw a considerable uptick in relocation activity in the first three quarters of 2021, illustrating tenants’ confidence to make more long-term real estate decisions. Relocations reflected a flight-to-quality trend—especially in primary markets like Manhattan and Washington, D.C.—that supports tenants’ efforts to attract employees back to the office more regularly. Expansion activity increased while contraction activity decreased in the 2021 vs. 2020 comparison periods.

Figure 2: Office Leasing Activity by Transaction Type in Secondary Markets

Source: CBRE Research, Q3 2021

Secondary markets3 saw a greater percentage of new-to-market leasing activity in 2021 vs. their primary market counterparts. Companies’ migration to new secondary markets mirrors the movement of population to lower-cost and less-dense metro areas during the pandemic. The average lease size for companies expanding into secondary markets increased by 17% in the 2021 vs. 2020 comparison periods, suggesting that tenants are making bigger commitments to these markets.

Figure 3: New-to-Market Office Leasing by Region (Q2 2020 - Q3 2021)

Source: CBRE Research, Q3 2021.

The South-Central and Southeast regions accounted for the most new-to-market leasing activity since Q2 2020. Personal income tax rates may be one factor driving this movement, as 72% of new-to-market leasing within these two regions and 42% of new-to-market leasing overall has occurred in markets with no state income-tax, such as Dallas/Fort Worth, Nashville and Miami.

The growth of new leasing in the first three quarters of 2021 signals a budding recovery of the U.S. office market. How omicron will impact this recovery is uncertain, but the improvement exhibited in 2021 despite the delta variant gives reason for optimism in 2022.