Intelligent Investment

Prime Multifamily Metrics Improve for First Time in Two Years

April 12, 2024 3 Minute Read

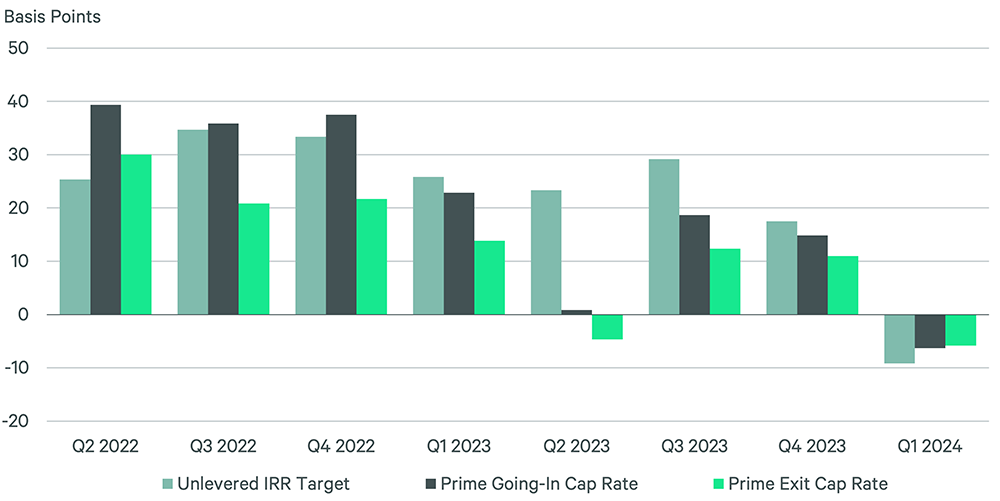

Going-in cap rates, exit cap rates and unlevered internal rate of return (IRR) targets for prime multifamily assets improved slightly in Q1 for the first time since the Federal Reserve began raising interest rates in early 2022. These improvements indicate that key underwriting metrics may have peaked in anticipation of possible rate cuts later this year.

Figure 1: Quarter-over-Quarter Change in IRR Target & Cap Rates

The slightly positive spread between going-in and exit cap rates stabilized at 12 basis points (bps) in Q1 after falling for eight consecutive quarters. This positive spread will likely continue unless economic conditions unexpectedly deteriorate.

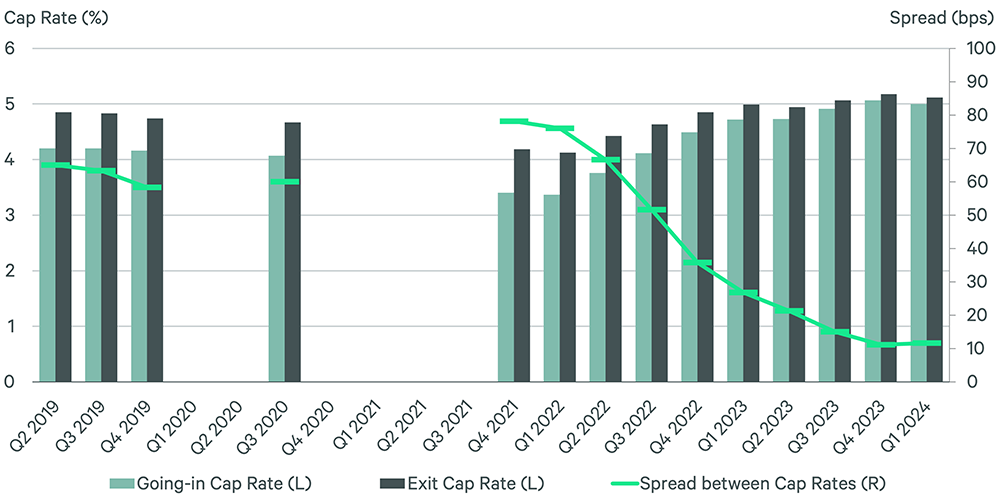

The overall average exit cap rate for prime multifamily assets is not expected to fall below the going-in rate over the near-term. However, on a market-by-market basis, cap rates have already inverted in Chicago (Q4 2022), Washington, D.C. (Q3 2023) and Philadelphia (Q1 2024). Phoenix and Seattle, which previously reached cap-rate parity, returned to a positive spread in Q1. Cap-rate parity continued in New York and San Francisco.

Figure 2: Going-In & Exit Cap Rate Spreads

Note: Survey was not conducted for six quarters throughout the COVID-19 pandemic due to lack of trendable market activity and price discovery.

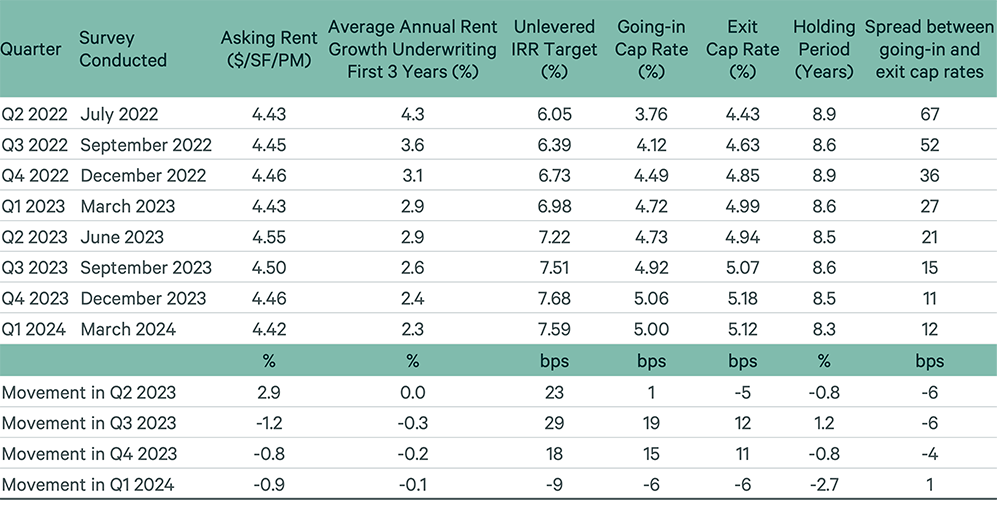

After several quarters of decelerating growth, the average prime multifamily going-in and exit cap rates decreased by 6 bps in Q1 to 5.00% and 5.12%, respectively. Underwriting assumptions of annual asking rent growth over the next three years decreased slightly in Q1 to 2.3%.

Unlevered IRR targets decreased by 9 bps in Q1 to 7.59%. All but two (Chicago and Philadelphia) of the 15 prime multifamily markets tracked by CBRE had either stable or lower IRR targets in Q1. Denver (-100 bps) and Los Angeles (-50 bps) had the biggest reductions.

Figure 3: Buyer Valuation Underwriting Assumptions for Prime Class A Multifamily Assets

For the 10th consecutive quarter, Austin had the lowest risk requirements on an underwriting basis. Most markets remained unchanged quarter-over-quarter, with only Los Angeles and Phoenix moving slightly up the list because their underwriting metrics improved.

Figure 4: Buyer Valuation Underwriting Assumptions for Prime Class A Multifamily Assets by Market, Q1 2024

Note: Estimates of current buyer underwriting assumptions for the highest quality asset in the best location of a particular market. The quoted prime rents reflect the level at which top-tier relevant transactions are being completed. Estimates are based on the expert opinion of local CBRE investment professionals.

Four markets (Denver, Los Angeles, Phoenix and Seattle) had moderate going-in cap rate decreases in Q1, while eight had no change. Going-in cap rates increased by less than 25 bps in three markets (Chicago, Miami and Philadelphia). Exit caps were unchanged in 12 markets, while Chicago, Denver and Los Angeles had slight decreases.

Related Services

- Invest, Finance & Value

Capital Markets

Gain proactive insights and strategies that unlock value, drive returns and enhance outcomes for your real estat...

- Property Type

Multifamily

Unlock the potential of your residential real estate with expert investment, financing, valuation, due diligence, design, management and leasing strat...