Intelligent Investment

Q1 2021 Apartment Forecast

May 7, 2021 2 Minute Read

Multifamily fundamentals started to stabilize in Q1—quarterly rent increased by 0.4% from Q4 2020 after declining for three quarters, although the rent is still weaker compared to a year ago. Y-O-Y rent fell 4.2% to $1,673.54. The vacancy rate for our national sample of properties was at 4.7% in Q1 -- 50 bps above the first quarter of last year. The supply pipeline remains strong, with stock growing a healthy 1.8% Y-O-Y.

With widespread distribution of vaccines and more fuel from government spending, the US economy had a strong start this year and Q1 GDP increased at 6.4% annual rate. March unemployment rate was at 6%, a considerable decline from 14.8% recorded in April 2020, but still above 3.5% recorded in February of 2020. Widespread vaccinations, re-opening of major metros together with continued job growth would help the recovery of the multifamily sector.

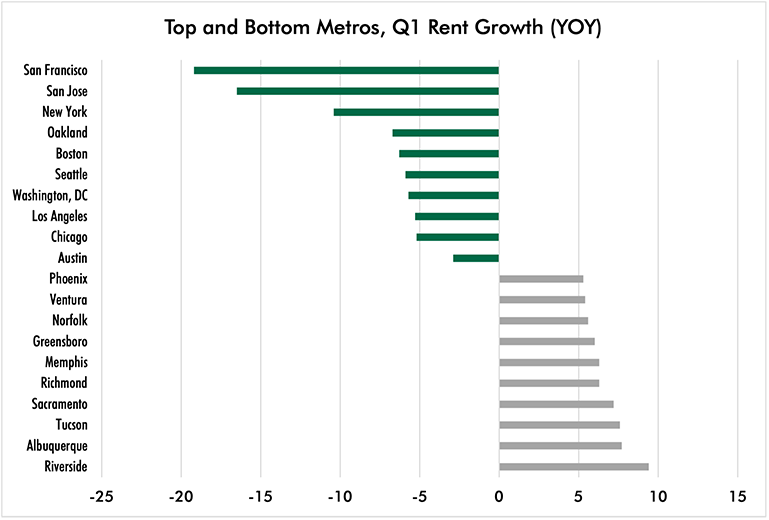

Due to outmigration, rents fell furthest in major metropolitan markets. With remote working allowing employees to live further from the office, and some of the amenities in major metros still shuttered, rental demand has shifted toward secondary and tertiary metros where renters can find more space at a lower cost. We expect this trend to be temporary, with demand shifting back to major metros from H2 2021 through 2022, as workers return to the office and renters compete to lock in lower rents before they rise to pre-COVID levels.

We believe national multifamily rent bottomed out in Q4 2020 and will continue to recover, with secondary markets leading the recovery in H2 2021, followed by major metros. Vacancy is expected to rise to 4.9% at its highest point in Q2 2021. The long-term outlook for multifamily remains strong, with rent expected to recover to pre-COVID levels by Q1 2022, and vacancy to recover to pre-COVID levels one quarter after.