Future Cities

Secondary Markets Stand Out in U.S. Office Recovery

September 21, 2022 3 Minute Read

Despite a slow post-pandemic recovery, vacancy rates in more than half of the nation’s major office markets—those with more than 25 million sq. ft. of total inventory—are now below their pandemic-era peaks. Fast-growing Sun Belt markets have been the most resilient and are attracting the attention of both occupiers and investors.

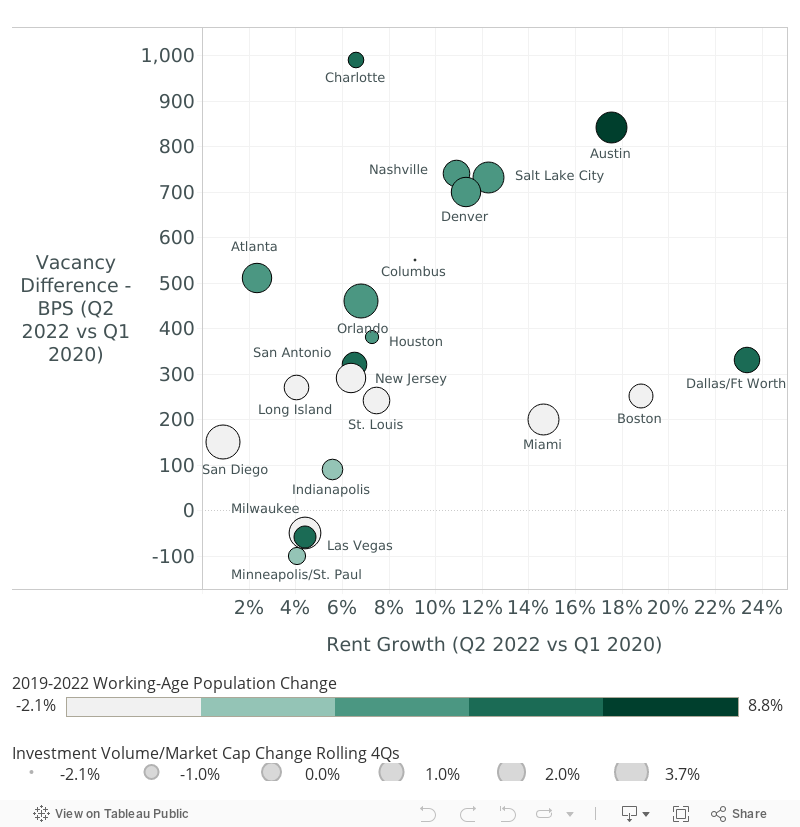

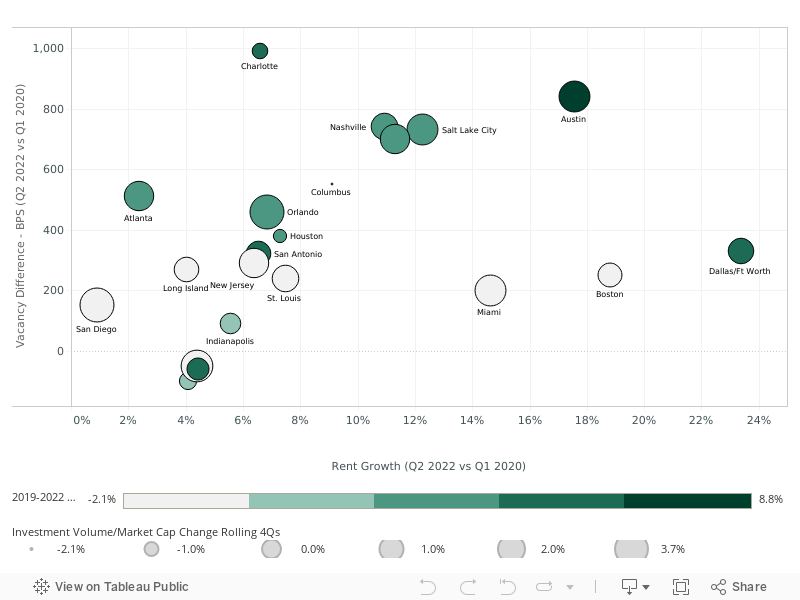

Figure 1 illustrates the 19 secondary and two primary1 markets (Dallas and Boston) that have outperformed the U.S. average in a combination of metrics, including rent growth, vacancy reduction and population growth since Q1 2020 and investment volume growth since Q2 2021. Markets in the lower right quadrant had the highest rent growth and lowest vacancy rate relative to their pre-pandemic levels, with dark green shading representing strong working-age population growth and a large bubble representing strong investment volume growth as a percent of market capitalization. No single market scored highest for all the indicators.

Figure 1: Market Recovery Dynamics

Source: CBRE Research, Real Capital Analytics, EMSI Burning Glass, Q2 2022.

*Working age population change through June 2022.

Figure 1: Market Recovery Dynamics

Source: CBRE Research, Real Capital Analytics, EMSI Burning Glass, Q2 2022.

*Working age population change through June 2022.

COVID restrictions were eased earlier in Texas than most of the country, contributing to a faster office market rebound in Dallas and Austin.2 Both have led Kastle Systems’ top 10 markets for office occupancy rates throughout the pandemic.3 While Austin had the strongest working-age population growth among all markets (8.8%) and impressive rent and investment volume growth, its vacancy rate remained relatively high compared with its pre-pandemic rate (+840 basis points), partly due to a large amount of new speculative space. Most of the demand in Austin is from tech tenants and concentrated Downtown.

In Dallas, most of the leasing activity is outside of the CBD, which has a vacancy rate of more than 30%. Dallas has long grappled with high vacancy due to a large supply of outdated office space. In the suburbs, a variety of tenants, including Charles Schwab, Caterpillar, Keurig and PGA of America, have recently committed to new office space.

Two Florida metros are also standouts: Miami and Orlando. Finance, technology and health-care tenants are driving office demand in Miami. Despite a 200-basis-point increase in its vacancy rate since Q1 2020, tenant demand for premier office space in the CBD has driven rent growth of nearly 15%, prompting the delivery of new supply. Miami has recorded four consecutive quarters of positive net absorption and robust office investment volume.

Some primary markets that were particularly hard-hit by the pandemic are beginning to see their vacancy and rental rates stabilize. Aside from Dallas, Boston stands out for its rent growth, a nearly 1-percentage-point drop in its vacancy rate from its pandemic-era peak and positive office absorption over the past several quarters. Life sciences and tech companies have fueled demand for office space in Boston and have been especially active in leasing new construction.

As companies remain thoughtful about office utilization, location and talent attraction, fast-growing markets benefiting from in-migration and that offer affordable housing, amenities and short commutes will remain in favor. However, rampant growth has impacted some of these markets by overburdening infrastructure and heightening competition for talent. This has contributed to demand migrating to other markets; San Antonio and Houston, for example, are seeing spillover demand from Austin.

1 Primary markets are defined as markets with a total asset value of more than $100B.

2 “Map of COVID-19 case trends and restrictions,” USA Today, July 11, 2022.

3 “Getting Back to Work,” Kastle Systems.

Contacts

Insights in Your Inbox

Stay up to date on relevant trends and the latest research.