Adaptive Spaces

Shallow-Bay Industrial Availability Remains Tight Amid Strong Demand

March 24, 2026 5 Minute Read

Demand from smaller industrial occupiers for shallow-bay properties—buildings under 50,000 sq. ft. with clear heights between 14 and 28 feet—is outstripping available supply.

Unlike big-box warehouses that have expanded rapidly in recent years, the supply of shallow-bay space has grown only modestly, leaving many markets with aging inventory and limited new construction. An analysis of major U.S. markets highlights how limited supply, steady tenant demand and regional market dynamics have shaped performance of the shallow-bay segment over the past decade.

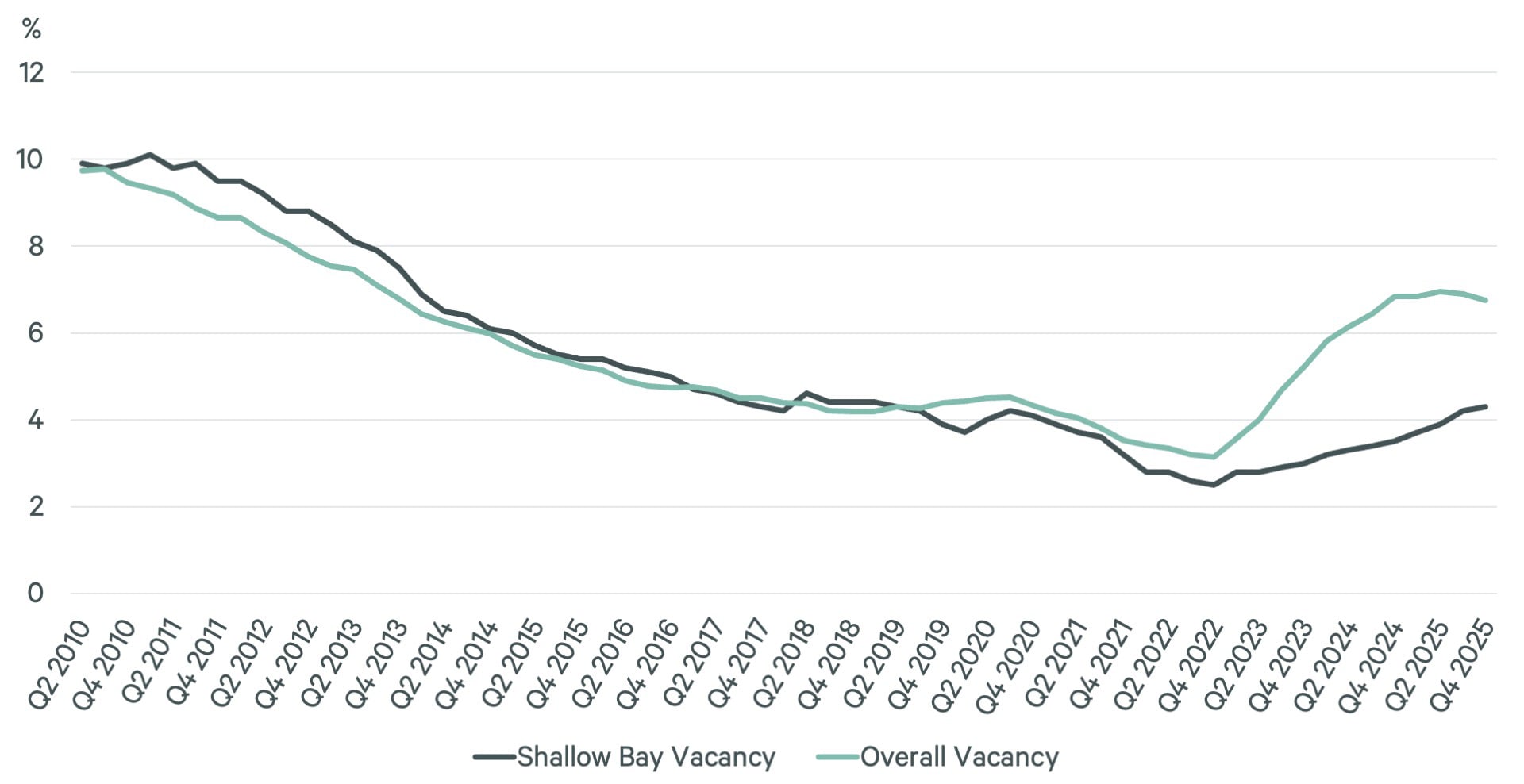

Figure 1: Shallow-Bay Vacancy Falls Below Overall Industrial Vacancy

Starting in 2017, shallow-bay vacancy began falling below the overall industrial vacancy rate, reflecting growing demand for smaller-format space tied to service-oriented users and last-mile distribution. This gap widened significantly during the recent development cycle, as new supply was largely concentrated in big-box warehouse development while shallow-bay construction remained limited. By early 2024, shallow-bay vacancy was 2.5 percentage points below the overall industrial vacancy rate, underscoring the limited availability amid sustained demand for these smaller facilities.

Aging Inventory Amid Limited New Development

Figure 2: Shallow-Bay Inventory Concentrated in Older Facilities

With little new development over the past two decades, shallow-bay industrial inventory in major U.S. markets is heavily concentrated in older facilities. Nearly half of shallow-bay inventory was built prior to 1980 and more than 80% was built before 2000. Properties built since 2010 account for only 5% of total inventory. This aging supply reflects the economic challenges of developing new shallow-bay facilities in major markets, where land costs and zoning constraints often favor larger warehouse developments.

New industrial development over the past decade has been largely big-box facilities, with relatively little construction of facilities under 50,000 sq. ft. This has led to a growing supply imbalance between smaller and larger industrial facilities.

Rents Climb Amid Steady Demand

Figure 3: Shallow-Bay Rents Rose Steadily Over Past Decade

Source: CBRE Research.

Shallow-bay industrial rents have increased steadily over the past decade as demand strengthened for smaller-format space serving light-manufacturing and local occupiers. While overall industrial rents accelerated rapidly during the pandemic-era logistics expansion, shallow-bay rent growth was more measured, reflecting the sector’s distinct tenant base and limited speculative development pipeline. By 2025, shallow-bay asking rents were more than 50% higher than 2010 levels, highlighting the durable demand and supply constraints of this segment. The steady increase in rents over this period reflects continued leasing activity and limited available space for smaller occupiers across most markets.

Regional Market Fundamentals Vary

Figure 4: Shallow-Bay Market Conditions Vary by Market

Shallow-bay fundamentals are closely tied to regional population growth, land constraints and local economic conditions.

Orange County, CA and Charlotte are the most supply-constrained markets for shallow-bay space, with both low vacancy rates and rents that rank among the highest across the markets analyzed. A larger group of markets, including Phoenix, Atlanta and Dallas-Fort Worth, command above-average rents relative to other U.S. markets but have slightly higher vacancy rates due to their larger size or recent development activity.

Many Midwest markets such as Chicago, Milwaukee and Columbus also have very tight availability, but with comparatively lower rent levels to coastal and high-growth markets. This highlights the stable demand for smaller industrial spaces serving local manufacturers and distributors.

Limited Construction Pipeline Continues to Support Fundamentals

Limited new construction of smaller multi-tenant industrial space reflects the economics of modern industrial development. Rising construction costs, higher land prices in urban locations and tenant preferences for modern amenities have limited most new projects to larger big-box warehouse facilities. In addition, institutional capital has increasingly favored large distribution assets with long-term leases to national tenants, further concentrating development activity in the big-box segment. As a result, shallow-bay inventory remains heavily composed of older properties.

Outlook

The combination of limited supply and steady tenant demand will likely keep shallow-bay fundamentals relatively tight across many U.S. markets. Strong rent growth in several high-cost markets may create opportunities for selective new development or redevelopment of existing sites, though rising construction costs and zoning restraints will continue to make these projects difficult to break ground.

Demand for shallow-bay space remains closely tied to small and mid-sized businesses that serve local economies. While a slowing economy could temper demand in the near term, the limited development pipeline and aging inventory base suggest shallow-bay properties will remain an important and supply-constrained segment of the industrial market.

Related Insights

-

Brief | Intelligent Investment

Impact of Supreme Court’s Tariff Ruling on Industrial Real Estate

February 27, 2026

Supreme Court tariff ruling boosts U.S. industrial leasing, port activity, and IOS demand, benefiting key logistics markets.