Intelligent Investment

Thriving U.S. Industrial Market Well Positioned to Withstand Economic Headwinds

May 26, 2022 3 Minute Read

Executive Summary

- Industrial real estate is expected to remain well positioned should an economic downturn emerge.

- While inflation remains near a 40-year high, it is primarily being driven by the energy, automobile and food sectors—not by general merchandise that is widely stored in warehouses.

- Retail sales, which have the biggest impact on industrial real estate fundamentals, remain solid and consumers are spending more online than in 2020.

- Large companies are leasing more warehouse and distribution space to hold more inventory as a check against rising supply chain costs.

- Leasing activity year-to-date through April is up by 7% from the same period in 2021, led by third-party logistics (3PL) providers. Total leasing volume for the full year is expected to be the second strongest on record.

- Manufacturing demand is expected to rise this year as more companies onshore their operations to avoid supply chain disruptions.

- Despite record new development, strong demand for first-generation industrial space will keep the market from becoming oversupplied. The overall vacancy rate currently stands at just 3.1%.

- Taking rental rates were up by 16% year-over-year in Q1 2022. Landlords are expected to further raise rents in undersupplied markets, passing on increased debt service and other costs to their tenants.

The Economy

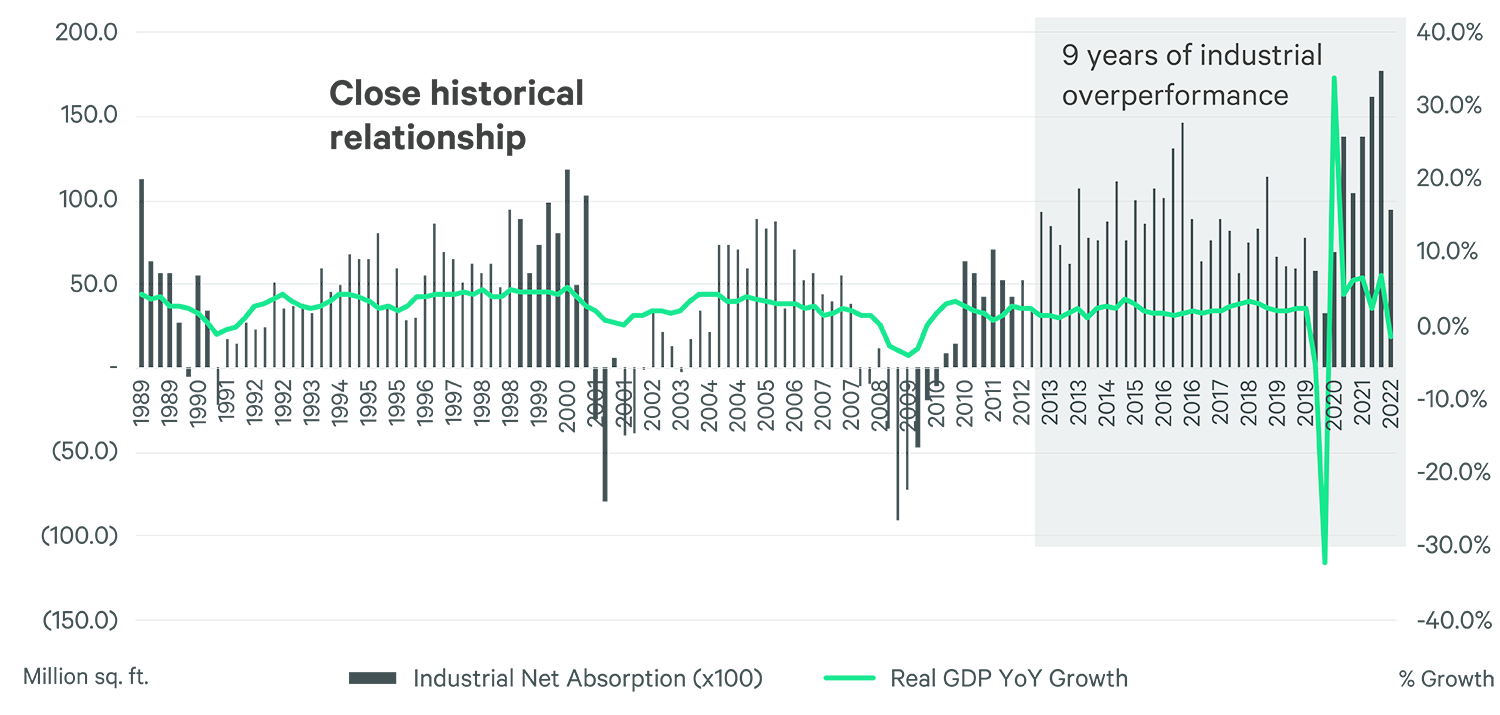

The U.S. economic outlook is becoming more pessimistic due to rising inflation, geopolitical instability and tighter monetary policy. Industrial real estate demand has outperformed the economy for the past nine years because of the growth in e-commerce sales, diversification of supply chain sources, inventory control and population shifts. These drivers will support the sector in the event of an economic slowdown.

Figure 1: Industrial Demand Outperforms GDP

Source: CBRE Econometric Advisors, Bureau of Economic Analysis, Q1 2022.

Retail Sales

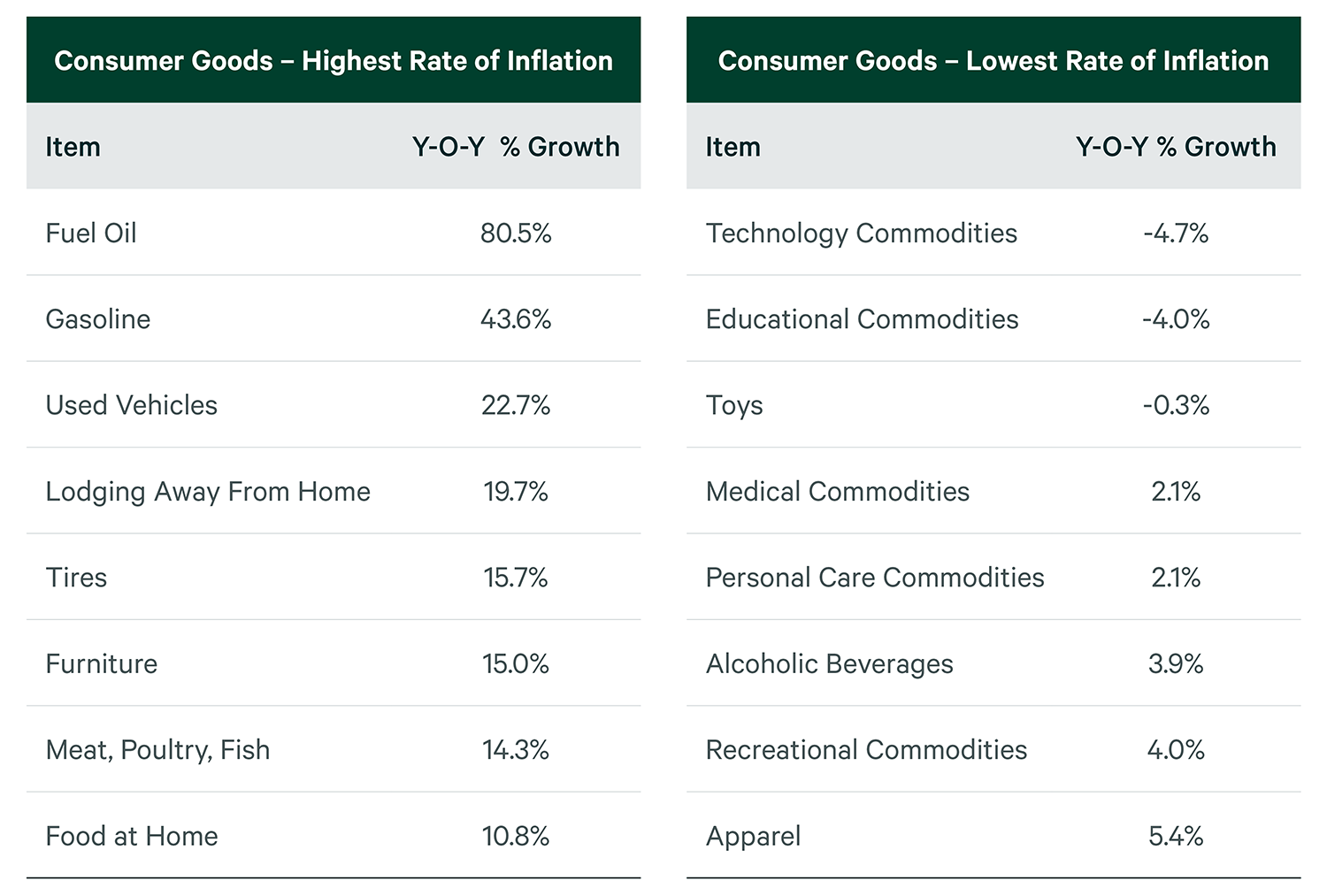

Forty-year-high inflation has not dampened retail sales. While energy, automobile and food prices continue to rise, prices of many general merchandise items typically stored in warehouses have either decreased or stayed the same as last year. April’s 20-bp drop in inflation is a positive sign as the year progresses. CBRE forecasts an inflation rate of 6.6% for the year.

Figure 2: Consumer Price Index Price Growth by Item

Source: U.S. Bureau of Labor Statistics, April 2022.

Much attention has been focused on the 60-bp year-over-year drop in e-commerce’s share of total retail sales in Q4 2021. However on a full-year basis, the e-commerce share was unchanged at 19.5%, with online sales rising by $100 billion and brick-and-mortar sales up $400 billion. Several important conclusions can be drawn from this data:

- Many online retailers and their suppliers are expanding to keep up with increased online sales and the corresponding need to hold more inventory closer to consumers.

- More than 80% of items stored in warehouses are distributed to brick-and-mortar retailers. Traditional retail sales remain just as important to industrial demand as online sales, as the need to keep stores fully stocked will fuel the need for additional warehouse and distribution space.

- CBRE projects both traditional and e-commerce sales will finish 2022 on par with 2021 and that it will take a significant decline in sales to cancel occupiers' expansion plans.

Figure 3: E-Commerce as a % of Non-Auto Retail Sales

Note: Retail sales does not include motor vehicles, parts dealers, and gasoline stations.

Source: CBRE Econometric Advisors, Q1 2022.

Supply Chain Costs

Global transportation costs continue to rise. On May 19, the average cost to ship a standard 40-foot container ($7,600) was 24% more than a year earlier, according to Drewry Supply Chain Advisors. International shipping costs to the U.S. are also elevated, with the Shanghai to Los Angeles route up by 55% to $8,700 and the Rotterdam to New York route up 102% to $7,200.

Domestic freight costs are rising even more, up by almost 31% year-over-year in April and nearly 90% from two years ago, according to the Cass Freight Index on Expenditures. Rising fuel prices and trucker shortages are largely to blame. The U.S. average per-gallon cost of diesel fuel, for example, hit $5.61 on May 16, up by 236% from a year ago, according to the U.S. Energy Information Administration.

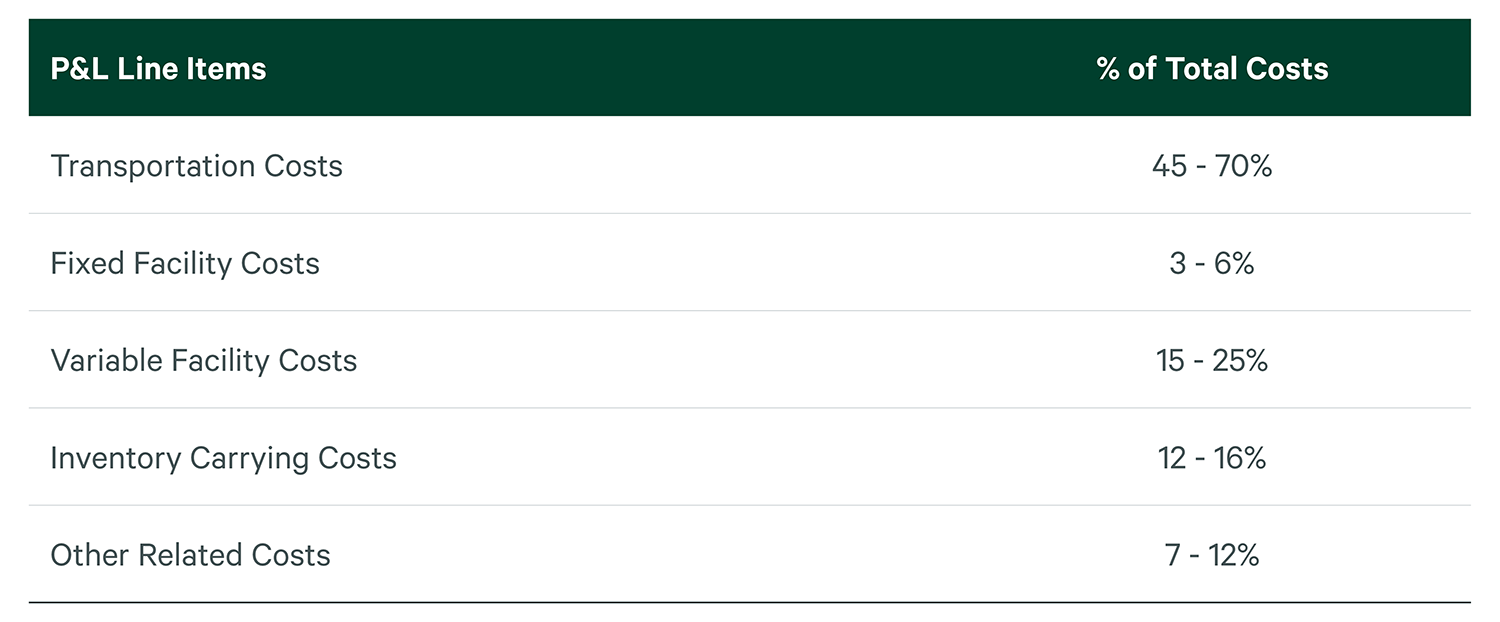

Transportation costs account for between 45% and 70% of total supply chain costs, while inventory carrying costs make up between 12% and 16% and fixed facilities costs account for only 3% to 6%, according to CBRE Supply Chain Advisory.

The rise in transportation costs can be a double-edged sword for industrial demand. Larger occupiers can lease additional space for more inventory near consumers to cut transportation costs, but smaller industrial occupiers (25,000 sq. ft. and less) may not. These small businesses that are more acutely feeling the pinch of cost increases could slow expansion plans or vacate space in the coming quarters.

Figure 4: Supply Chain Cost Breakdown

Source: CBRE Supply Chain Advisory.

How Will Industrial Respond?

Demand

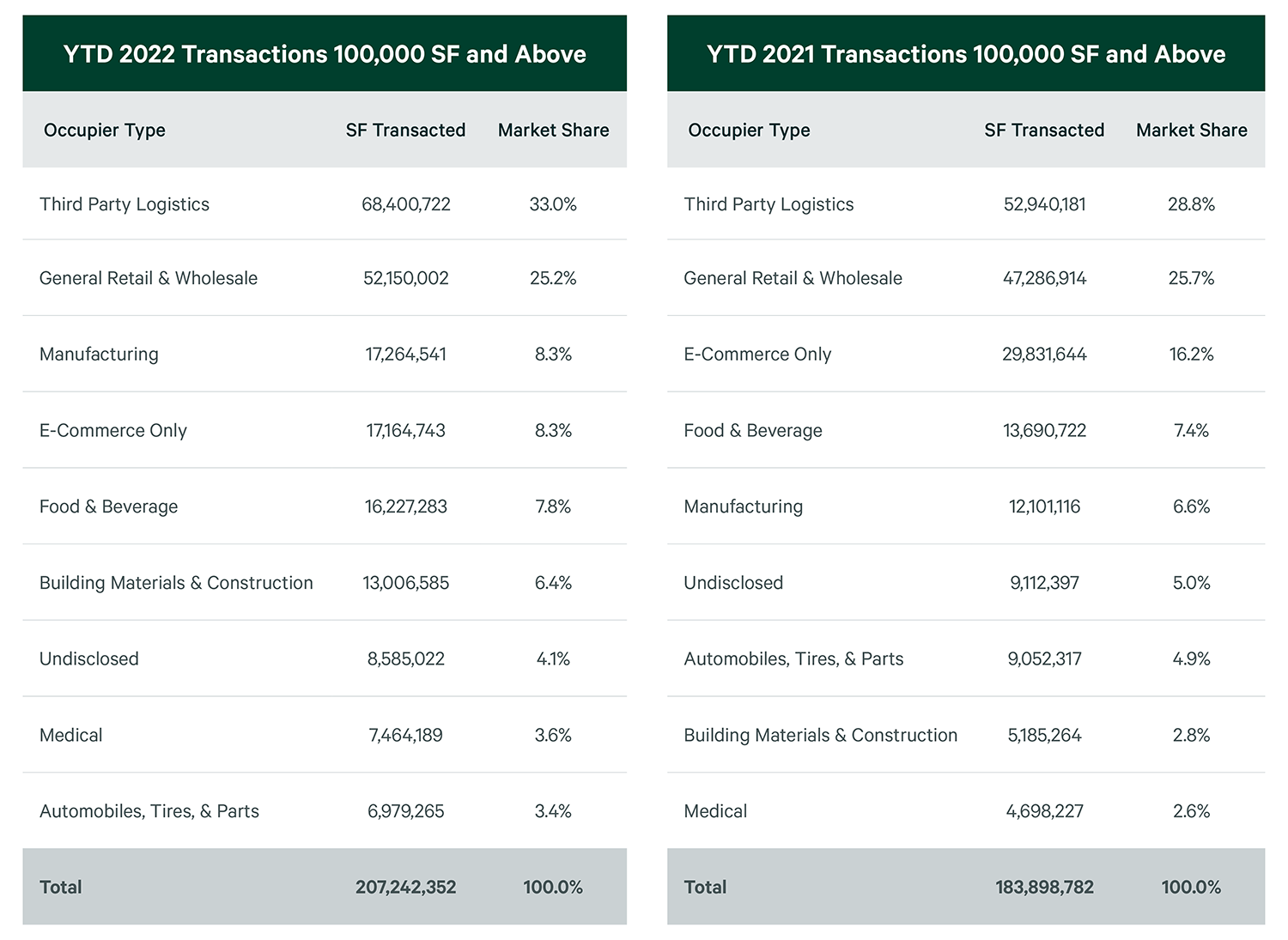

Industrial leasing activity through the first four months of 2022 increased by 7% year-over year to 300 million sq. ft. Of that amount, 3PL providers leased 68.4 million sq. ft. for a 33% market share. Outsourcing of distribution will increase as retailers and wholesalers look to mitigate risk from undersupply, rising rents, labor shortages and a possible economic slowdown. Look for 3PL market share to surpass 35% by year-end.

Demand for specialty industrial real estate, including manufacturing plants, industrial outside storage, data centers and cold storage facilities, is expected to increase this year. Manufacturers were the third most active industrial occupier through April, more than tenants that focus solely on e-commerce distribution. Onshoring of manufacturing operations will be a major component of supply chain diversification, especially for the electric vehicle components, computer and vehicle technology, packaging materials, medical and defense industries.

Despite a slowdown in demand from e-commerce and big-box retailers, CBRE forecasts that leasing activity will total between 850 million and 900 million sq. ft. for the year—about 10% to 15% less than last year’s record level. The 1 billion sq. ft. of leasing volume in 2021 was an outlier and there is not a large enough tenant base to maintain that pace. Nevertheless, 2022 is expected to have the second highest total on record.

Figure 5: Bulk Leasing Activity by Occupier Type

Note: Compares new lease and renewal transactions 100,000 sq. ft. and above from 1/1 to 4/30.

Source: CBRE Research, April 2022.

Supply

With an overall vacancy rate of just 3.1%, U.S. net industrial space absorption fell to 93.8 million sq. ft. in Q1—the lowest level since Q3 2020. The drop in net absorption was not due to less demand but to a 130 million-sq.-ft. year-over-year reduction in available space.

These tight market conditions have led to record-high development. As of Q1, 545 million sq. ft. is under construction, with 177 million sq. ft. already accounted for. Despite this surge in new supply, many U.S. markets remain undersupplied when comparing available under-construction space with tenant demand.

Rental Rates

The average industrial rental rate year-to-date through April is up by 16% from the same period last year. Rental rate growth is prevalent in coastal markets and near expanding population centers. Despite some economic uncertainty, a landlord’s market is expected for the foreseeable future with no letup in rent escalations. Rent growth will accelerate at an even higher pace in markets with below-average vacancy rates. Short supply will keep landlords bullish on raising rents even further, passing on higher debt service and other costs to tenants.

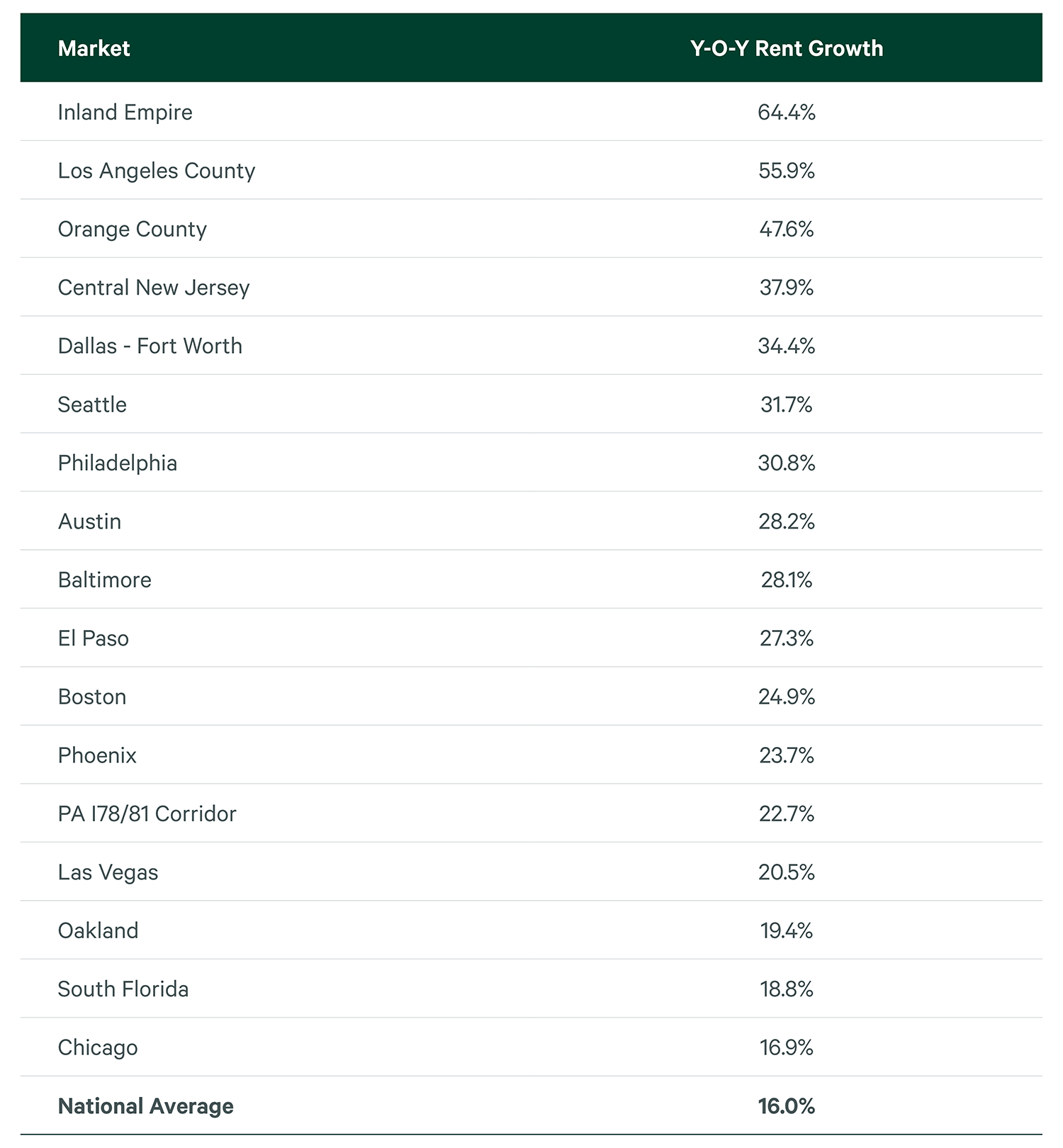

Figure 6: Top Markets for Year-Over-Year Taking Rent Growth

Note: Compares first year base rents for leases 10,000 sq. ft. and above with a lease term of 12 months and above from 1/1 to 4/30 2022 vs the same time period in 2021.

Source: CBRE Research.

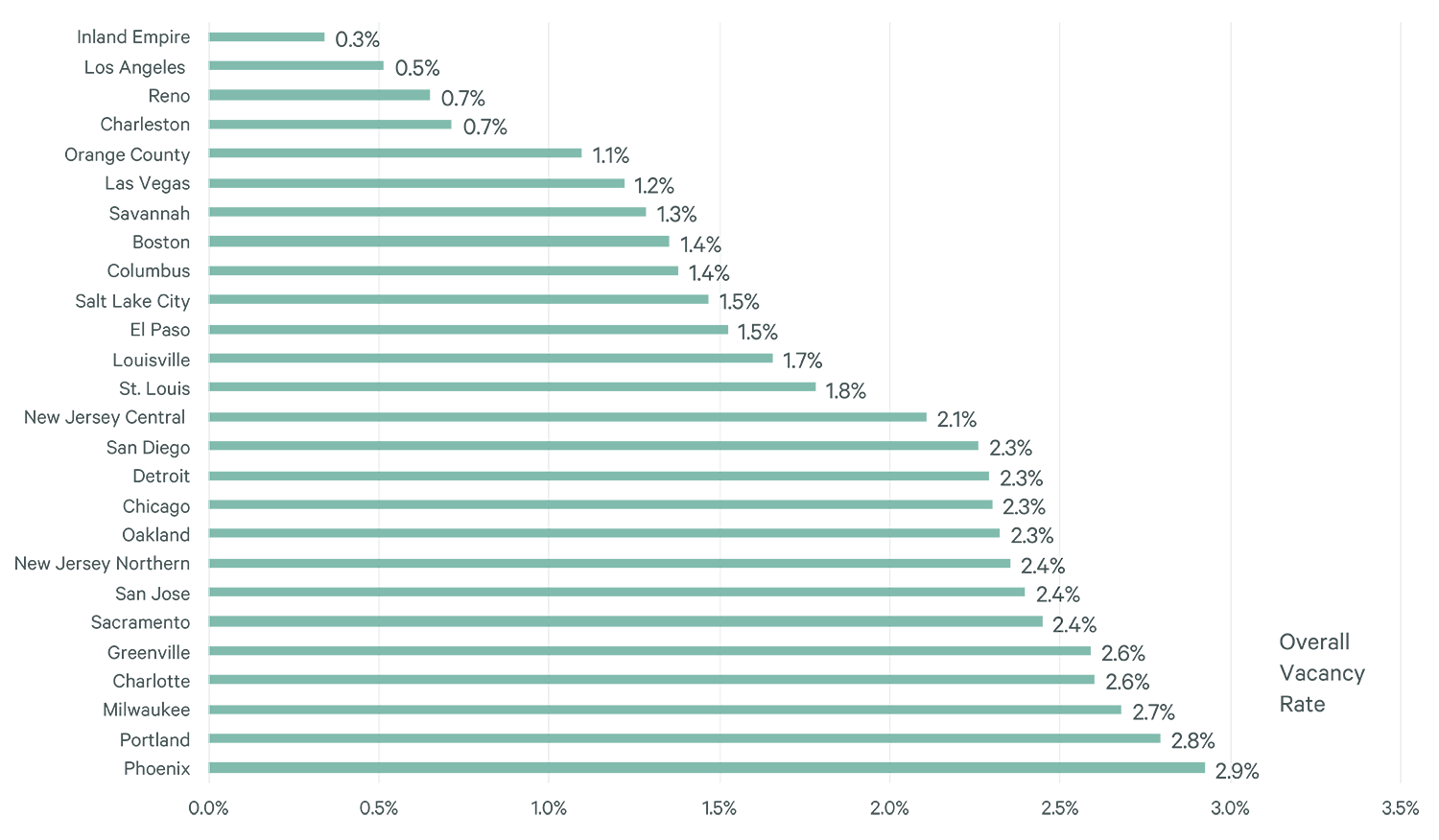

Figure 7: Markets with Lowest Vacancies Will Post Highest Rent Growth in the Coming Quarters

Note: Markets with vacancy rates under the national average.

Source: CBRE Research.