Intelligent Investment

CBRE Berlin Hyp Housing Market Report Berlin 2026

Rental price dynamics are slowing down, purchase prices for condominiums are rising slightly again - housing shortage remains

May 11, 2026 60 Minute Read

Looking for a PDF of this content?

Overview

- Asking rents remain almost stable at an average of €15.80 per square metre

- Supply of rental apartments remains at a low level

- Asking prices for condominiums are rising slightly – prices for apartment buildings are stagnating

- Large rental housing construction projects are mainly outside the S-Bahn ring and in the Berlin metropolitan area

Rental housing market

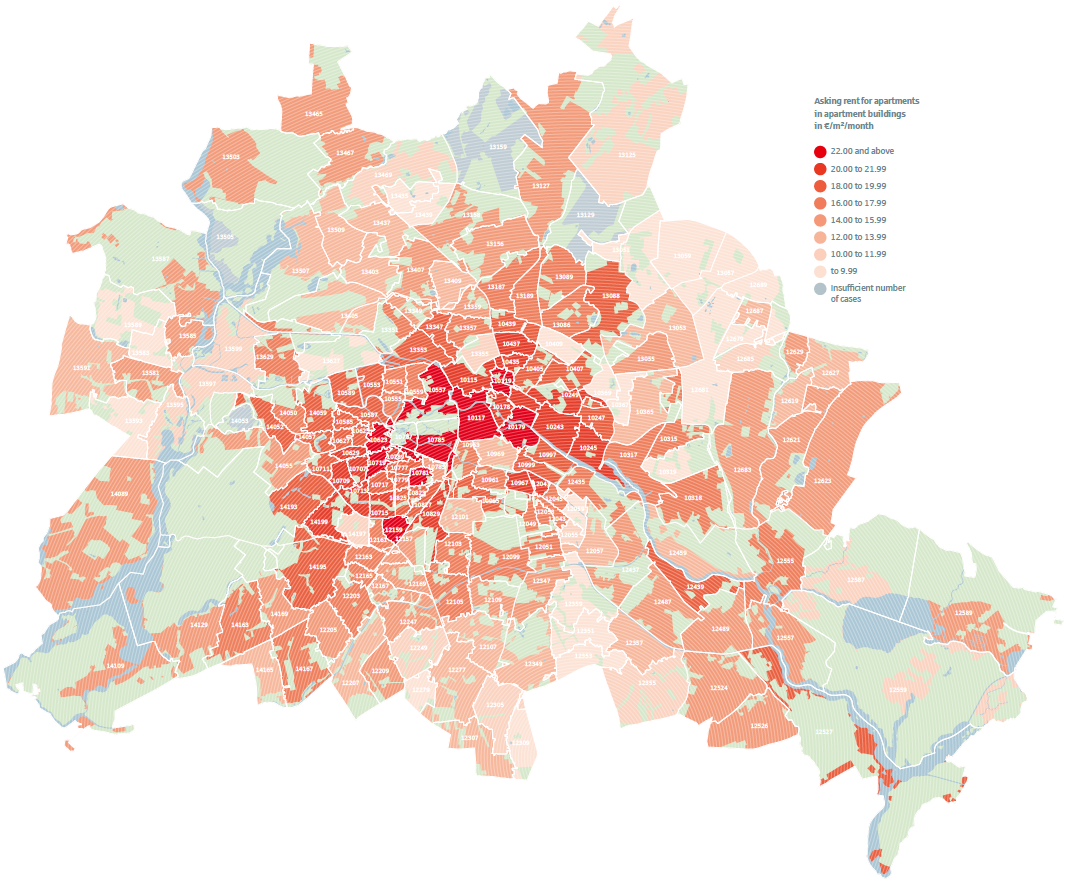

Following the enormous dynamics of asking rents (new contract rents) with double-digit rent increases in some cases in previous years - over 18 per cent from 2022 to 2023 and around 16 per cent from 2023 to 2024 - the Berlin housing market has stabilized at a high level in 2025. Compared to 2024, these have risen only minimally by 0.1 per cent to an average of €15.80 per square metre.

While the average rent across Berlin increased only slightly, the top market segment even declined: Here, the median fell by 2.9 per cent to €28.57 per square metre. One reason for this is the lower number of completed new residential buildings by private developers, which usually dominate the upper market segment. In the segment of privately financed new construction, there was a decline in the average asking rent of three per cent to €20.73 per square metre. The bottom market segment, which is usually publicly subsidized, remained stable with a slight increase of 0.4 per cent to €7.06 per square metre.

The discrepancy between existing rents and new contract rents is getting bigger and bigger. In Berlin, for example, existing rents of large, institutional portfolio holders are on average €8.50 per square metre, and even less than €7.00 on average for state-owned companies. It will be difficult for tenants with new leases. Here, the new contract rents for state-owned and institutional apartments are on average around €8.81 to €10.50 per square metre – and thus at least around a third below the rental apartments offered online at €15.80 per square metre.

The large gap between existing and new contract rents affects not only new tenants but also young households and families with children. It also makes it more difficult for older people to find small, accessible apartments, and explains the very low willingness to move ("lock-in effect") and the resulting extremely low fluctuation.

The main reason for the sharp increases in asking rents for new leases in recent years is the significant excess demand and the lack of available housing. This is clearly shown by the negative correlation between rent developments and vacancy rates. The main driver of the housing shortage is the city's population growth, which is generally a positive development: According to the population register, the number of inhabitants has increased by more than half a million since 2010 and is now around 3.9 million people. This corresponds to an increase of almost 16 per cent and thus also a considerable increase in the number of private households.

On the other hand, there is too little new residential construction: in the same period, only around 159,000 new apartments were built, and a further 27,000 existing units were completed or replaced. This construction activity is far from sufficient to keep pace with the dynamic population growth.

Figure 2: Asking rents Berlin 2025

Source: CBRE based on VALUE market database

Condominiums and apartment buildings segment

After slight declines in previous years due to the rise in interest rates and the resulting reluctance of buyers, asking prices for condominiums saw a moderate increase again in 2025. Across all market segments, prices rose by two per cent to an average of €5,813 per square metre. Price increases were recorded in both the top and bottom market segments. While the top segment increased by 0.3 per cent, the rise in the bottom segment was more significant at 2.9 per cent. Nevertheless, prices have not yet fully returned to pre-crisis levels and the previous high of 2022.

In contrast to the market for condominiums, asking prices for apartment buildings stagnated again in 2025 – by 2.4 per cent compared to 2024 to an average of €2,967 per square metre.

One decisive factor was the increasing number of lower-quality properties offered for public, while very few new construction projects came onto the market. It can be observed that while the private buyer market has recovered, institutional investors remain somewhat hesitant to purchase.

New construction

Fortunately, in addition to the seven state-owned housing companies, some private property developers are still actively involved in planning and building. 214 construction projects with around 44,890 apartments were in concrete planning, development or already in the construction phase in 2025 – a slight increase compared to the previous year with 43,530 units recorded and thus reaching the level of 2022, after a significant decline in new construction activity became visible, especially in 2024.

Currently, only 12.7 per cent of new apartments are being built within the S-Bahn ring, and construction activity is increasingly shifting to the outskirts of the city. The proportion has been declining for years, as greater new construction potential in inner-city locations has largely been exhausted. Despite challenging conditions, the number of projects involving the seven state-owned housing associations rose slightly to 84 (2024: 68). On average, each project comprises around 210 units.

Business Contacts

Michael Schlatterer

Managing Director | Teamleader | Valuation Advisory Services

Sandro Hoeselbarth

Managing Director | Head of Valuation & Advisory Services