Dear reader,

In this benchmark report, where we investigate office market housing strategies, CBRE surveyed more than 100 companies about their strategies. These companies collectively use approximately 2.5 million square meters of office space, providing the panel with a representative view of key trends and developments in office usage. The panel consisted of the housing strategists from the participating companies, ensuring the highest possible quality of results. To obtain a representative view of the market, we approached both SMEs and corporates. Our ambition is to conduct this survey annually to accurately monitor market trends.

Two developments underpin this report:

With remote work now commonplace, many companies are seeking a new balance. What occupancy rate should you aim for? Should you mandate office days, and how do you maintain productivity? CBRE observes that many companies grapple with these questions. We hope this report provides insight into the market and showcases how different parties approach these issues.

The media often reports that the office market is shrinking, but CBRE sees a more nuanced picture in practice: some companies are downsizing, while others demonstrate growth in their housing. It’s too simplistic to draw a single conclusion about the entire market. CBRE aims to tell the complete story.

By comparing your own housing ambitions and challenges to this benchmark, you can better chart your course. For example, if you dream of a higher occupancy rate and notice competitors achieving this by mandating office days, it’s worth considering. Or perhaps you’re curious about how your ESG ambitions compare to the rest of the market? This report provides that insight.

Enjoy reading,

| Frank Verwoerd |

Bart van Eerd |

| Head of Research | Senior Director Agency |

Executive summary

In this benchmark report, we analyze the office space requirements of more than 100 companies, including both SMEs and corporates. Below are the key findings:

Hybrid way of working: Due to the pandemic, a hybrid way of working has become more common – employees are allowed to work from home or other locations more frequently. However, employers emphasize that coming to the office is essential for social interaction, collaboration, and learning.

Quality and accessibility: Quality of office spaces is crucial, and accessibility via public transportation ranks high. Sustainability remains an important factor.

Office occupancy trends: Office occupancy is increasing after a dip during the pandemic. However, the patterns vary significantly between companies, with wide variations across different days.

Differing space needs: SMEs expect growth and increased office space requirements, while many corporates anticipate reduced usage in the coming years.

Corporate focus on sustainability: Corporates prioritize buildings with at least an energy label A. This aligns strongly with concrete net-zero objectives set by over half of our respondents.

Willingness to pay for sustainable offices: Approximately half of the participants express a willingness to pay a premium for net-zero housing.

Facts & Figures

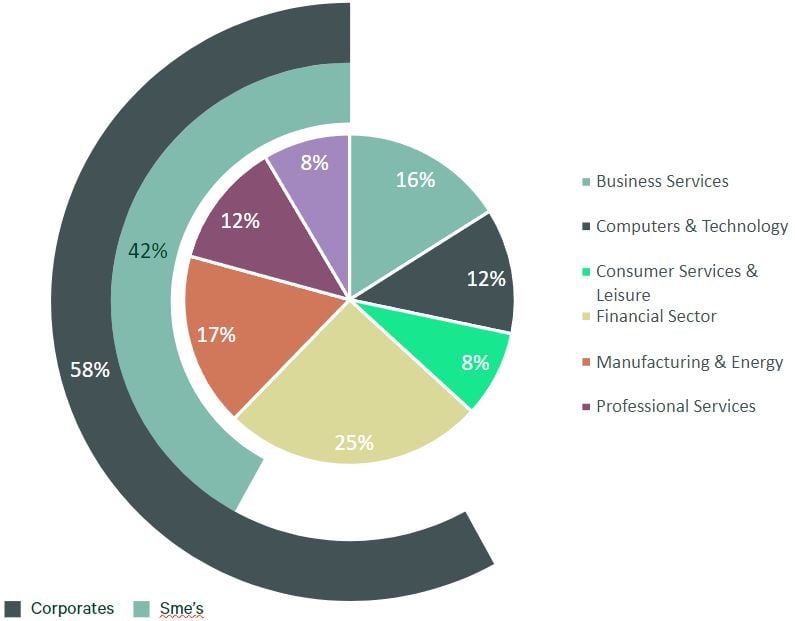

In this benchmark report, you’ll find results from a survey completed by over 100 organizations. These organizations vary in size and represent a diverse range of economic sectors. Of the participating companies, 80 have their headquarters in the Netherlands, 14 in other European countries, and 12 are located outside Europe. Together, they utilize 2.5 million square meters – nearly 6% of the total occupied office space in the Netherlands.

This report provides a clear overview of the key trends and developments in the Dutch office market. Important themes for this edition include policies on the hybrid way of working, the impact of the hybrid way of working on office usage and space requirements, ESG considerations, and changes in office requirements since the pandemic.

General housing strategy

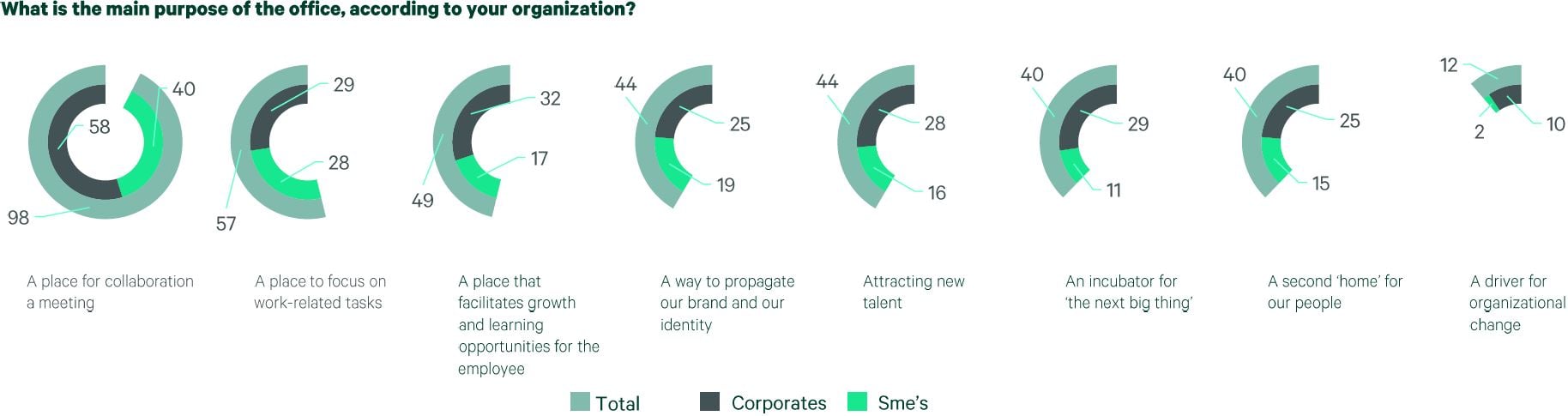

The office: a place to collaborate and learn

In today’s corporate landscape, remote work has become commonplace. Employees spend more time working from home in a quiet environment without distractions. Simultaneously, the participants in the occupier panel emphasize that the office plays a vital role in fostering collaboration, connection, learning and social interaction. The office as a hub where colleagues come together to exchange ideas, engage in brainstorming sessions, discuss projects and build strong team bonds.

Accessibility and quality of the office are crucial for office users

Panel participants clearly emphasize the importance of a healthy workplace – in other words, high-quality office spaces.

Accessibility also ranks high, especially concerning public transportation. Parking remains a hot topic, as does the sustainability of the office building.

Differences Between Corporates and SMEs

Corporates generally prioritize sustainable buildings, accessibility via public transportation, proximity to talented employees, and flexibility in square meters. They also value adaptable spaces. On the other hand, SMEs focus more on costs and parking availability.

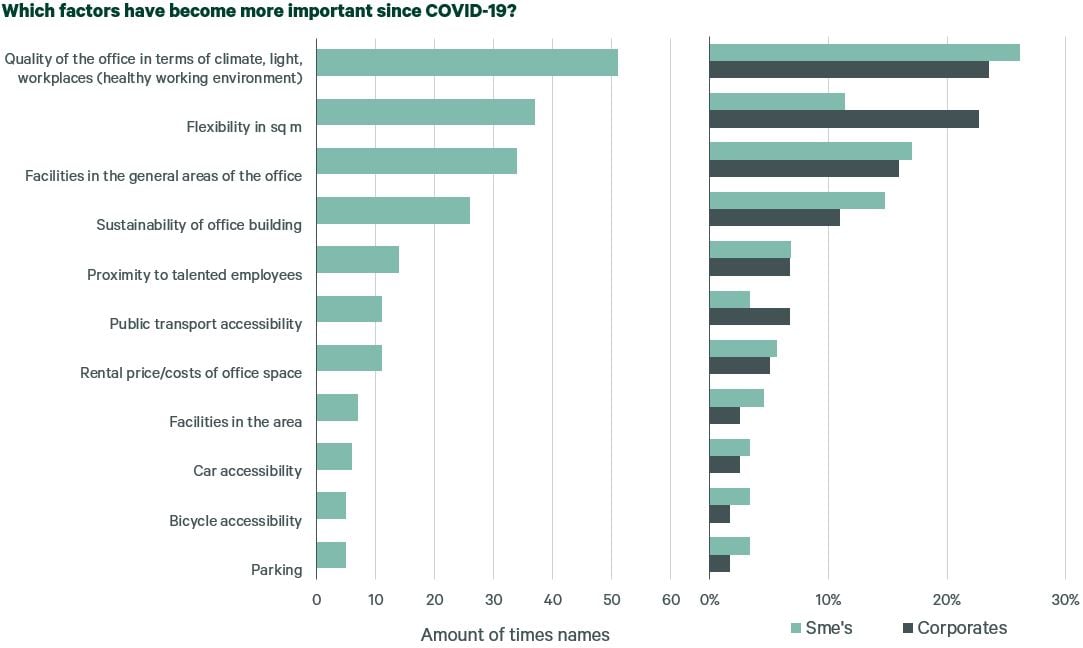

The quality of office space has become even more crucial since the pandemic

Since the pandemic, the quality of office spaces has become even more crucial. But that’s not all: flexibility in square footage, amenities in the general areas of the office, and sustainability have also risen in importance.

As remote work becomes increasingly common, the role of traditional office spaces is evolving. To ensure that colleagues continue to come to the office, it must offer unique advantages that distinguish it from the home workspace.

Differences Between Corporates and SMEs

Corporate participant of this occupier panel indicate that since the pandemic, they have focused more on the quality and flexibility of office spaces. Additionally, amenities in common areas and accessibility via public transportation are considered more important.

SMEs also emphasize the importance of quality offices and associated facilities but prioritize sustainability in office buildings. Flexibility and public transportation accessibility play a lesser role for them.

Employee flexibility is starting to become commonplace

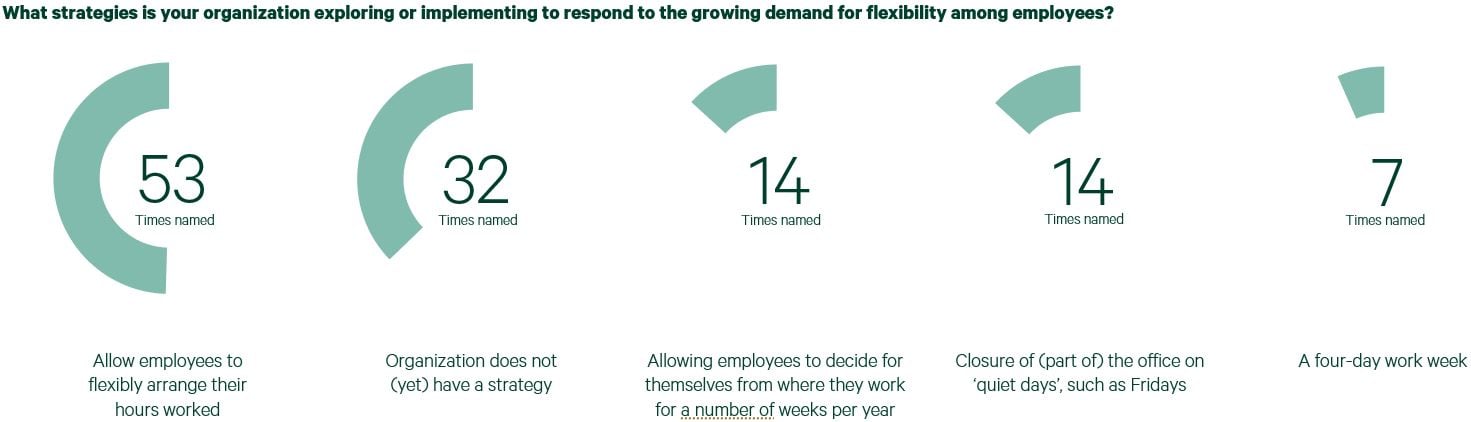

Approximately half of the participants say that employees can flexibly arrange their working hours. Additionally, one-third of organizations report having no strategy to address the growing need for flexibility.

A small number of respondents close part of their offices on quiet days, such as Fridays, or provide employees with the opportunity to work remotely from anywhere in the world for a specific period each year.

The recent attention to the four-day workweek, as AFAS plans to implement it by 2025 while maintaining full-time salaries, is met with limited enthusiasm, as only 7 participants consider it a realistic strategy.

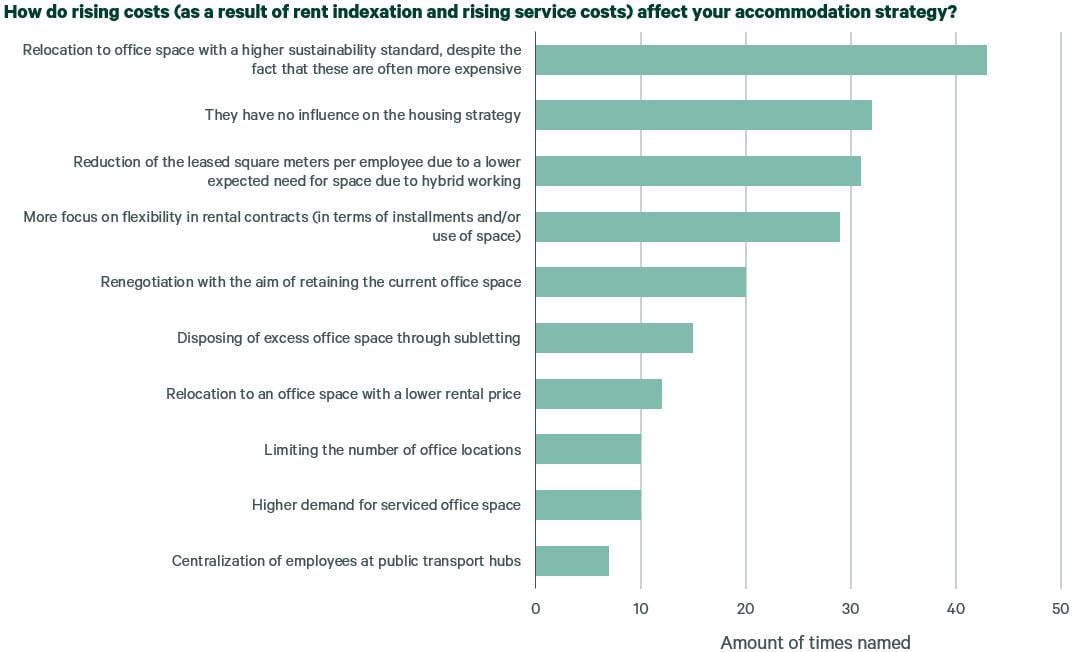

The rising costs have had limited impact on the housing strategy thus far

Office users continue to prioritize sustainability, even in the face of rising rental and service costs. Many are willing to move to office spaces with higher sustainability performance, even if it means paying a higher rent.

Interestingly, increasing costs have not significantly impacted the housing strategy of a significant number of participants in this panel. Instead, companies prioritize space reduction (such as divesting office space or subleasing) and contract flexibility.

Despite the cost increases, only a limited number of office users consider renegotiating their current contracts or relocating to cheaper office spaces.

A decline expected across the board

Among respondents, it is clear that the desk per employee ratio at corporates is significantly lower than at SMEs. The participating SMEs currently report an average of 88 workplaces per 100 employees.

It is expected that SMEs in the Netherlands will retain 71 workplaces per 100 employees. Despite the higher desk per employee ratio in SMEs, a comparable decrease of approximately 20% is expected here.

Impact of hybrid way of working

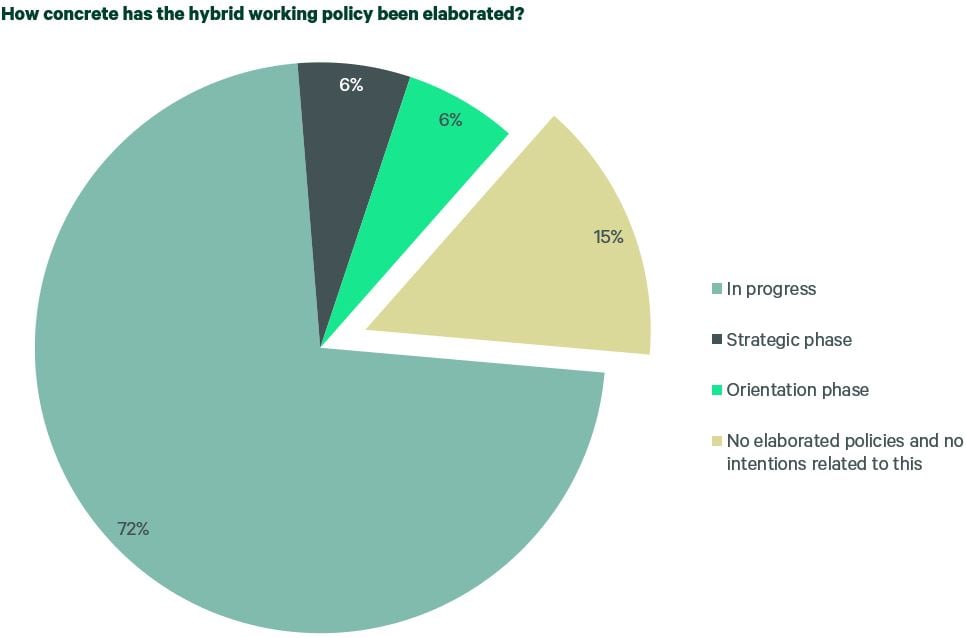

Hybrid work policies have been widely implemented

Approximately three-quarters of the participants have implemented hybrid working policies. A minority is still in the exploratory or strategic phase.

Interestingly, about 15% of participants indicate that they do not currently have a hybrid work policy and have no plans to create one.

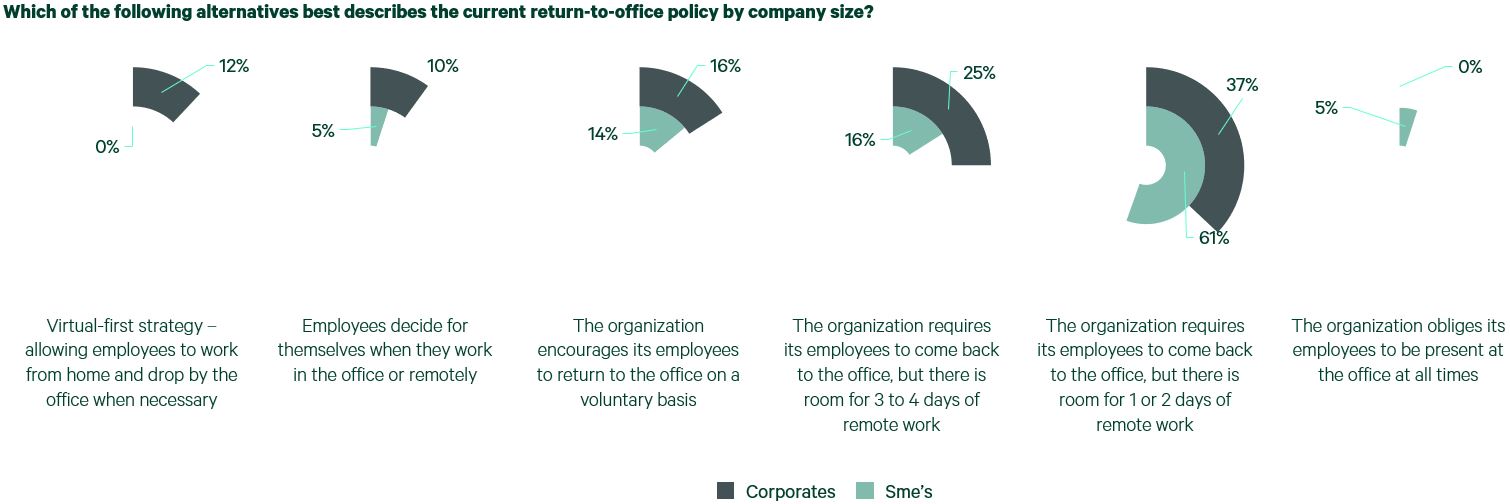

Corporates in particular give employees space to work from home

In contrast to most corporates, which require employees to be in the office for at least 1 or 2 days, SMEs often expect 4 to 5 days of presence. A small percentage of corporates still primarily promote remote work or allow employees to decide when they come to the office, a practice rarely seen among SME respondents.

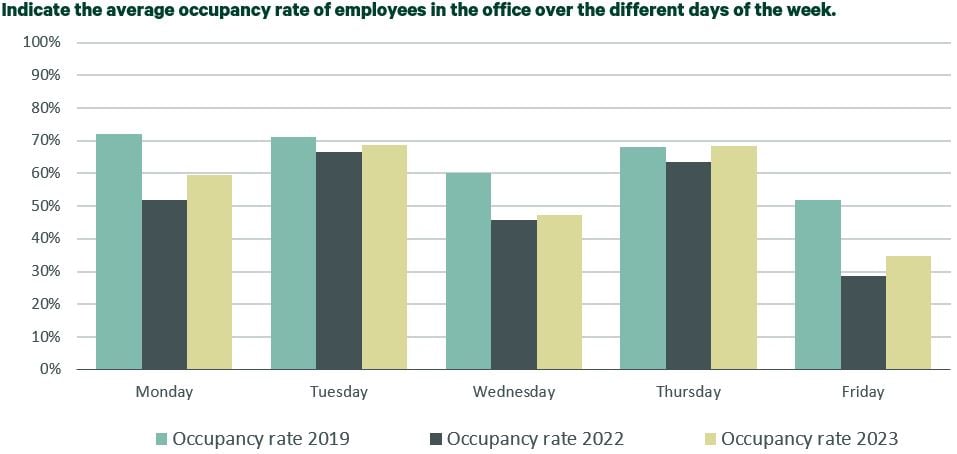

The office occupancy has been increasing since the pandemic, but there is greater variation between days

Tuesday and Thursday are busy days at the office, with high occupancy rates. Friday and Wednesday are quieter, and Mondays is a day with average occupancy.

Analyzing occupancy over the long term reveals two trends:

Gradual return to the office: Since the pandemic dip, office occupancy has been increasing annually.

Shift in busy and quiet days: While Tuesday and Thursday remain the busiest, Monday, Wednesday, and Friday are now quieter than before the pandemic. The variation between busy and quiet days has significantly increased.

Despite the overall increase in occupancy, substantial differences persist between days, making efficient planning challenging.

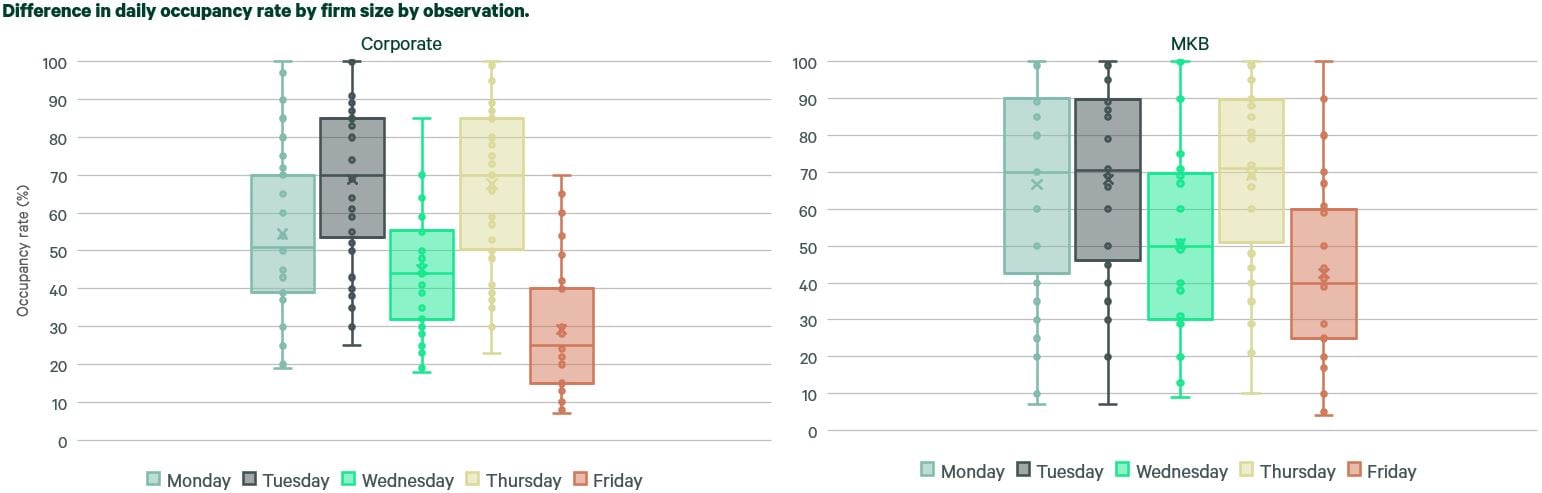

Occupancy rate higher for SMEs

The occupancy rate at small and medium-sized enterprises (SMEs) is higher than at corporations. This trend is particularly noticeable on Mondays and Fridays, and to a lesser extent on Wednesdays. The main reasons for this difference include work schedules, company culture, and commuting patterns.

Additionally, a larger proportion of corporate employees report having the freedom to decide when they work from the office. This is less common among SMEs. As a result, it makes sense that corporate employees work more from home, leading to lower occupancy rates in corporate offices.

Huge differences in occupancy rates

Employees of corporations come to the office significantly less often than employees of SMEs. Interestingly, the occupancy rate at corporations deviates notably on Mondays, Wednesdays, and Fridays compared to that of SMEs. On average, the occupancy rate for SMEs is 59%, while for corporations, it’s 53%. However, what stands out is the variation among different companies. Some still have an average occupancy as low as 20%, while others exceed 80%.

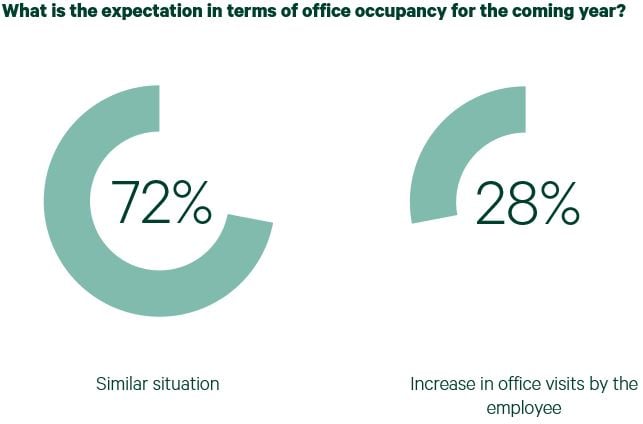

Stability in occupancy is expected

Most office users do not anticipate significant fluctuations in occupancy over the next year. However, approximately a quarter of respondents expect the trend of increased office usage to continue. As a result, occupancy rates may move even closer to pre-pandemic levels.

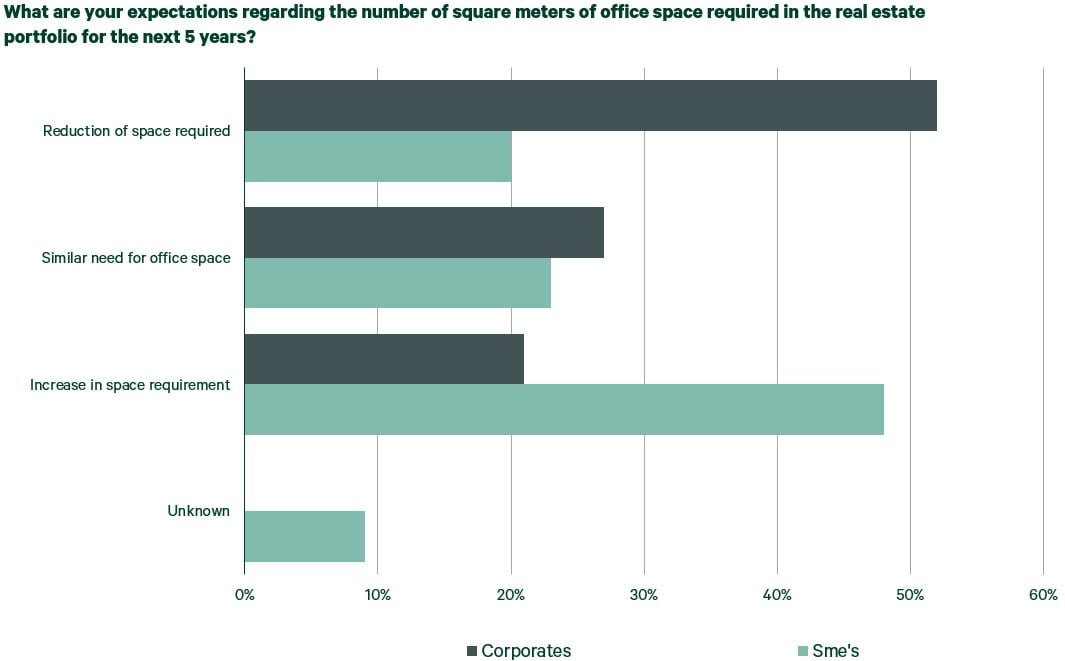

Corporates expect a decrease in space requirements, many SME participants expect growth

About half of SME respondents expect to need more floor space in the next five years. Meanwhile, 23% expect their office space to remain the same, and only 20% anticipate needing a smaller office.

Just over half of the larger corporates expect to need less office space. Most participants expect to use approximately 20% less floor space over the next five years. Only 21% expect to need more office space.

These divergent expectations between SMEs and corporates highlight how office space planning can differ based on the size of the organization.

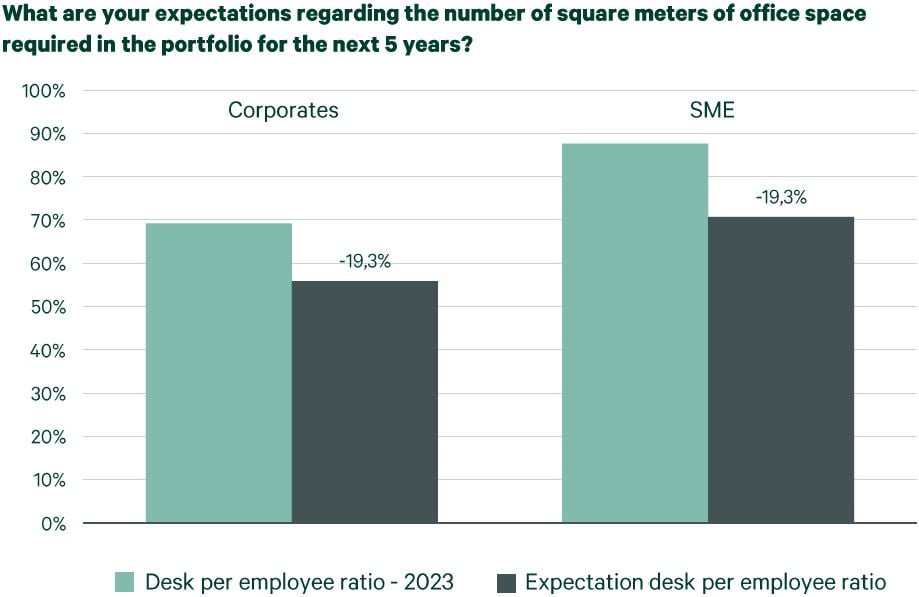

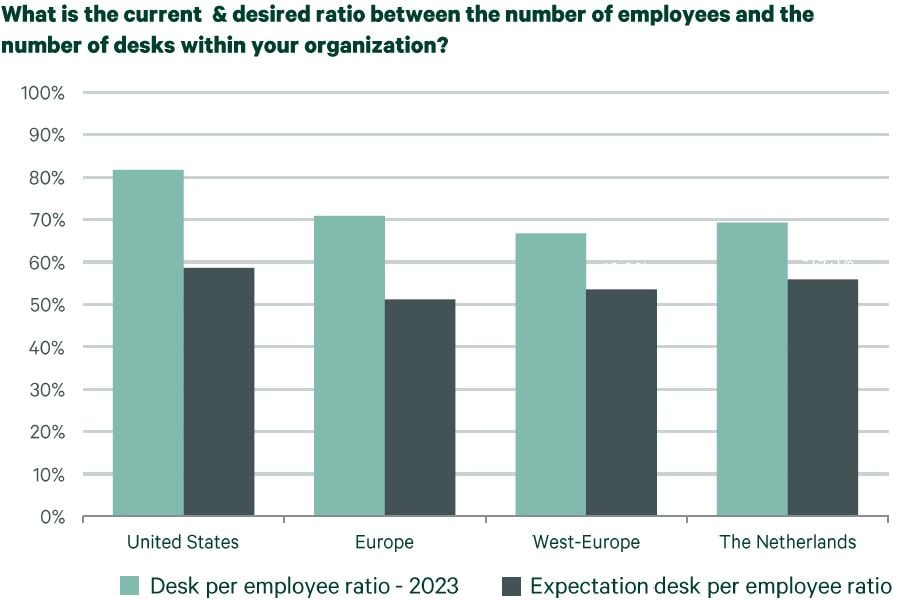

Workplace per employee ratio continues to decline

Corporates indicate that they currently allocate 69 workplaces per 100 employees. This ratio is similar to the European average (based on previous user surveys), but significantly lower than in the United States.

According to these participants, this ratio drops to around 56 workplaces per 100 employees in the Netherlands. That would mean a decrease of almost 20%.

A decline expected across the board

Among respondents, it is clear that the desk per employee ratio at corporates is significantly lower than at SMEs. The participating SMEs currently report an average of 88 workplaces per 100 employees.

It is expected that SMEs in the Netherlands will retain 71 workplaces per 100 employees. Despite the higher desk per employee ratio in SMEs, a comparable decrease of approximately 20% is expected here.

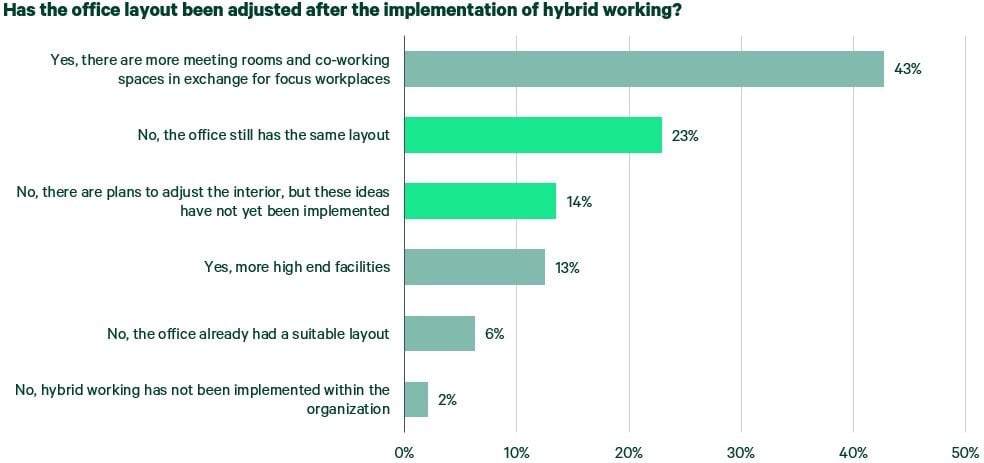

Not all companies have adapted their office design to hybrid working

Most office users have adjusted their workplace layout to support hybrid working. A smaller proportion of users have added high-quality facilities.

It is striking that just over 20% of users indicate that the office layout has remained unchanged.

In addition, 14% of office users indicate that they have plans to adapt the interior, but these changes have not yet been implemented.

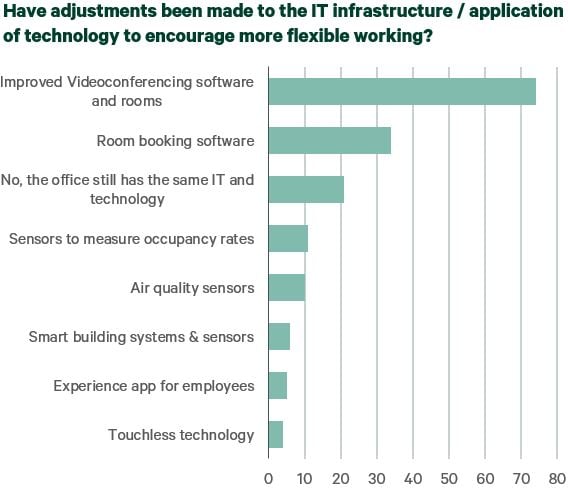

Many companies have upgraded their IT infrastructure

Most office users have upgraded their IT infrastructure. For example, by improving video conferencing software and setting up meeting rooms to support hybrid working. A smaller group of office users report that they have implemented software that allows you to reserve spaces. About 20% of office users made no changes to their IT infrastructure.

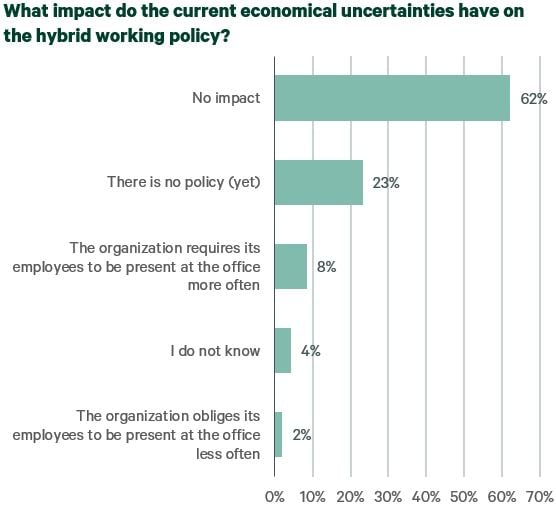

Economic uncertainty does not influence hybrid working policy

According to the panel, the current economic uncertainties do not have a significant impact on the hybrid work policy. Only 8% of respondents see economic uncertainty as a reason to require employees to be more present in the office.

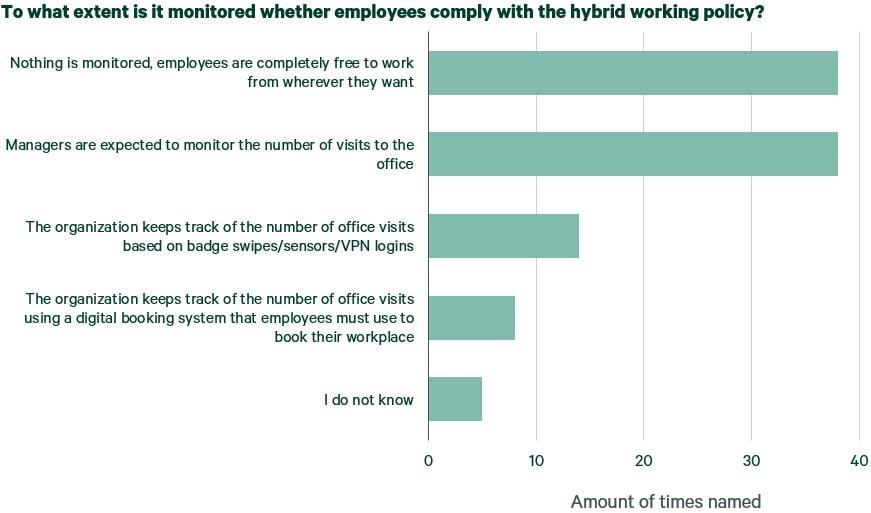

Employees are predominantly free in where they work

Most office users state that they do not monitor anything and that employees are free to work wherever they want.

Some organizations give managers the responsibility to monitor office visits, while the large-scale implementation of technological solutions such as badges, sensors, VPN logs or digital booking systems remains limited.

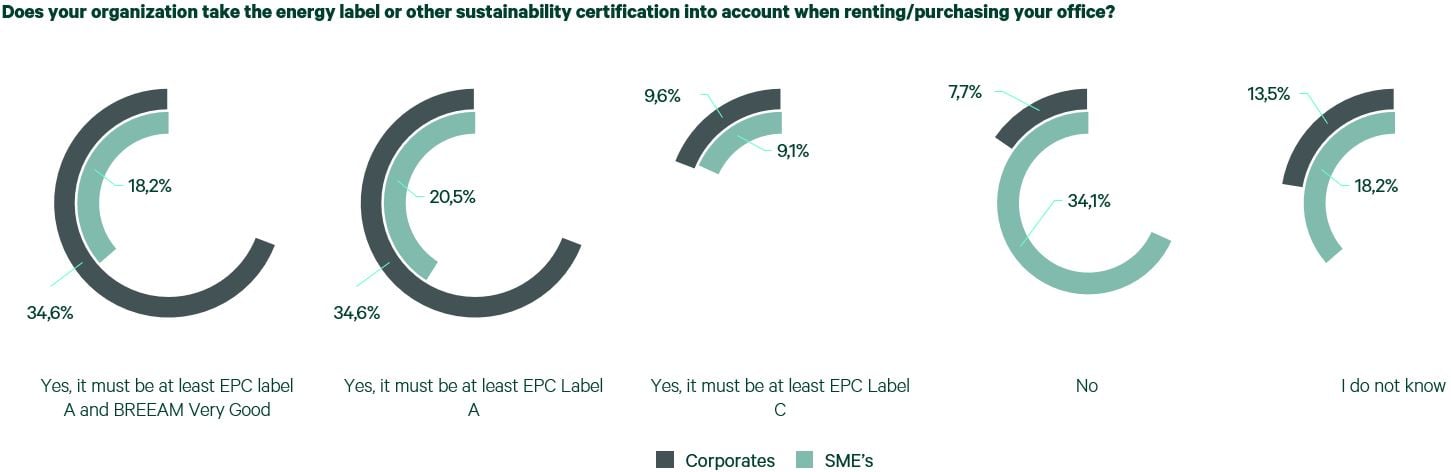

Sustainability certification is especially important for corporates, SME sustainability ambitions are lagging behind

Among corporate office users, 69% give priority to offices with at least energy label A when renting or purchasing. Among SMEs, this figure drops to 38%.

About a third of SME office users do not take energy labels into account at all.

A significant proportion of smaller office users indicate that they do not have a clear opinion about energy labels.

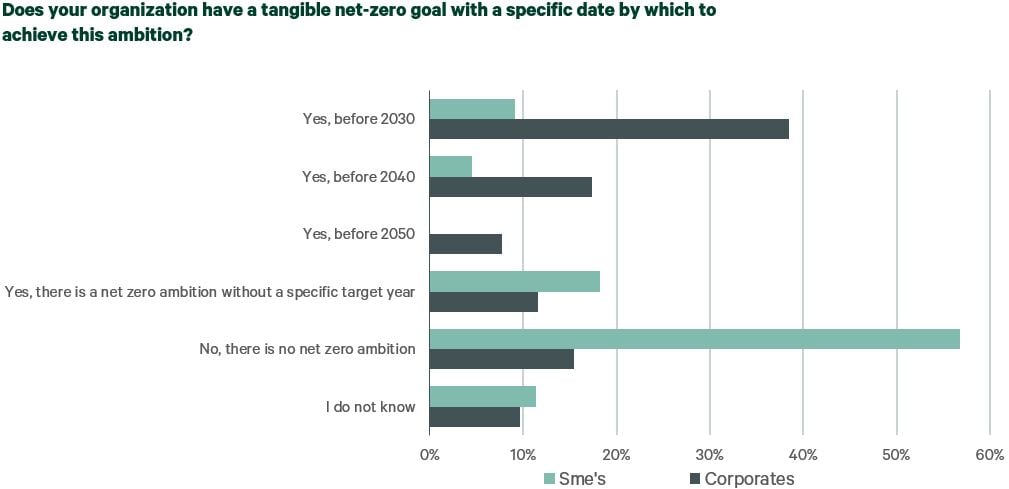

Corporate companies actively pursue ambitious and concrete net-zero goals

More than half of the participants have set a net zero target before 2040, with 38% of corporates even indicating that there is a net zero target for 2030.

Most SMEs, on the other hand, have no or less specific net zero objectives. This is because in 2023 they were not yet obliged to report these objectives in annual reports, in line with the CSRD.

Willingness to pay rental premium for net-zero housing

About half of the respondents indicate that they are willing to pay a rental premium to achieve a net zero target - although most also indicate that this should not be too high.

Interestingly, 36% are unsure about their willingness to pay more, while only 15% indicate that they do not want to pay a rental premium.

Interestingly, there are no clear differences between corporates and SMEs.

Key recommendations

- Employees are still coming to the office less than before the pandemic, but returns are steadily increasing. More than a quarter of respondents expect a further increase in the coming years. However, the peaks are still very spread over the different days of the week. This is partly because companies are implementing increasingly concrete policies regarding working from home, although monitoring and enforcement are still largely informal. There are opportunities to increase occupancy rates by making the office more attractive for employees (magnetize) or by better spreading the peak (mandate), so that less office space is needed.

- Sustainability and high quality of the building are the most important building features for users, while accessibility (via public transport) is the most important location factor. As remote working becomes more common, the role of traditional office spaces is evolving. To move with this shift, offices must prove their value compared to home workplaces through distinctive propositions.

- Interaction and collaboration are central to the housing strategy of most office users. To facilitate this, they want more flexible layouts and spaces. Moreover, desk sharing is becoming even more common. 37% of participants indicate that the layout of their office has not (yet) been adjusted. At the same time, investments are being made in technologies necessary to support the transition to new working styles. For example, many office users have already implemented improved software for video conferencing and meeting room reservations.

- Sustainable (net zero) offices are of great interest, especially among large corporates. However, the supply in this segment is limited, which means there is a risk of a shortage in the Netherlands. To avoid problems with set net zero targets, office users must anticipate this shortage in a timely manner. This can be done by capturing the available office space at an early stage, entering into discussions with the current owner, adjusting ambitions or realizing them in another way - outside of housing.