Intelligent Investment

U.S. Seniors Housing & Care Investor Survey 2022

Valuation & Advisory Services

April 5, 2022 8 Minute Read

Key Findings

Looking for a PDF of this content?

This 11th edition of CBRE’s Seniors Housing & Care Investor Survey had a record number of respondents, whose insights provide actionable market intelligence.

This survey identifies new trends in the Seniors Housing & Care industry. The data is based on market sentiment of the most influential seniors housing investors, developers, lenders and brokers throughout the U.S.

Recent surveys have provided a much-needed window into on-going changes in market conditions due to the COVID-19 pandemic. The H1 2020 survey, conducted in late February, provided insights into pre-pandemic market sentiment. Comparing this and the 2021 survey with our 2022 results provides a benchmark for the seniors housing industry’s recovery.

Figure 1: Survey Respondent Categories (%)

Source: CBRE Seniors Housing Investor Survey, 2022.

Senior Housing Trends

- Class B cap rates showed the most improvement with a 17-bp year-over-year decrease on average, followed by Class A with a 14-bp decrease and Class C with a drop of 9 bps.

- Active Adult (AA) communities once again led the survey’s “top investor opportunity” category, with cap rate decreases of 26 bps and 31 bps in the core and non-core Class A segments, respectively.

- Skilled Nursing (SN) and Continuing Care Retirement Community/Life Plan Community (CCRC/LPC) cap rates showed the greatest improvement with average decreases of 19 bps and 20 bps, respectively.

- The average seniors housing capitalization rate fell by 2 basis points (bps) from its pre-pandemic 2020 level, indicating slightly higher asset values.

- Staffing was ranked as the greatest headwind within the seniors housing industry.

- For AA, Independent Living (IL), Assisted Living (AL) and Memory Care (MC), the greatest percentage of respondents expect underwriting rental rate increases of between 3% and 7% over the next 12 months.

The Terraces at CC Young Dallas, Texas

Photography: HKS

Investor Survey Results

The average seniors housing capitalization rate fell by 13 bps year-over-year and is now below the H1 2020 pre-pandemic average.

Class B assets led the market with average cap rate compression of 17 bps, followed by Class A assets with a 14-bp drop.

Based on acuity, Skilled Nursing and CCRC/LPC cap rates showed the most significant movement on aggregate, compressing by 19 bps and 20 bps, respectively.

During the COVID-19 pandemic, lower acuity communities have faired best. However, cap rates among all acuity communities improved this year. Independent living showed the least movement, with an overall compression of 5 bps.

Figure 2: Seniors Housing & Care Capitalization Rates

Source: 2022 CBRE Seniors Housing Investor Survey results, change from 2021.

Cap rate spreads between asset classes were relatively flat, up by only 3 bps on a cumulative basis. The biggest movers in these spreads were the Active Adult segment with an increase of 31 bps and the CCRC/LPC segment with a decrease of 29 bps. Core Assisted Living assets also showed significant compression between A-B and A-C classes.

These investment class spreads show a trend of overall compression in core, Class B and Class C assets, or expansion in the investment appetite for non-Class A assets.

Location spreads between core and non-core assets were essentially flat at 48 bps, down by just 2 bps from the H1 2021 survey. As with investment class spreads, a similar ”search for yield” is evident in location spreads, with Class A core vs. non-core having the highest rate of compression at 9 bps.

Figure 3: Seniors Housing & Care Capitalization Rate Spreads & Internal Rate of Return

Source: 2022 CBRE Seniors Housing Investor Survey results, changes from 2021.

The Legacy at Midtown Park Dallas, Texas

Photography: HKS

Capitalization Rate Trends

Figure 4a: Historical Cap Rate Trends – Independent Living, Assisted Living & Memory Care

Note: Time periods represent when surveys were done.

Source: CBRE Seniors Housing Investor Survey results, 2022.

Figure 4b: Historical Cap Rate Trends – Skilled Nursing

Note: Time periods represent when surveys were done.

Source: CBRE Seniors Housing Investor Survey results, 2022.

Figure 4c: Historical Cap Rate Trends – CCRC/LPC

Note: Time periods represent when surveys were done.

Source: CBRE Seniors Housing Investor Survey results, 2022.

The Vista at CC Young Dallas, Texas

Photography: HKS

Lower for Longer

CBRE has a “lower-for-longer” outlook for U.S. cap rates, based on continued record annual investment volume. In addition to unprecedented investor demand for U.S. commercial real estate, liquidity in debt capital markets will further stabilize or compress cap rates even as interest rates rise.

While capital continues to flow from both domestic and foreign sources, their targets seem to be shifting. Particularly for multifamily, investors find non-coastal markets more acceptable than ever. There is a growing trend toward favoring ESG-compliant assets, and CBRE’s investor surveys indicate there is also a push to deploy more capital into alternative sectors like Seniors and Student Housing.

Figure 5: Cap Rates to Remain Lower for Longer

Source: CBRE Research, Federal Reserve, CBRE Econometric Advisors, Q1 2022.

As with multifamily, cap rates have compressed across key segments of the Seniors Housing sector. Cap rates for Class A IL/AL assets have fallen 80 bps since 2014. Note that we did not collect data for the Active Adult segment in 2014.

Figure 6: Cap Rates Compressed Across Key Seniors Housing Segments

Source: CBRE Seniors Housing Investor Survey, 2022.

Class A cap rates across the key Seniors Housing segments have kept pace with traditional multifamily cap rate compression.

However, there is a 190-to-260 bp spread between average Class A IL/AL and traditional multifamily cap rates, which investors see as an opportunity to achieve higher yields.

Looking ahead, we expect a greater proportional increase in Seniors Housing investment, a reduction in spreads to traditional multifamily cap rates and increased pricing of Seniors Housing Class A assets.

Figure 7: Seniors Housing Cap Rate Compression Keeps Pace with Multifamily

Source: CBRE Seniors Housing Investor Survey, 2022.

Survey respondents were asked a series of questions regarding near-term expectations

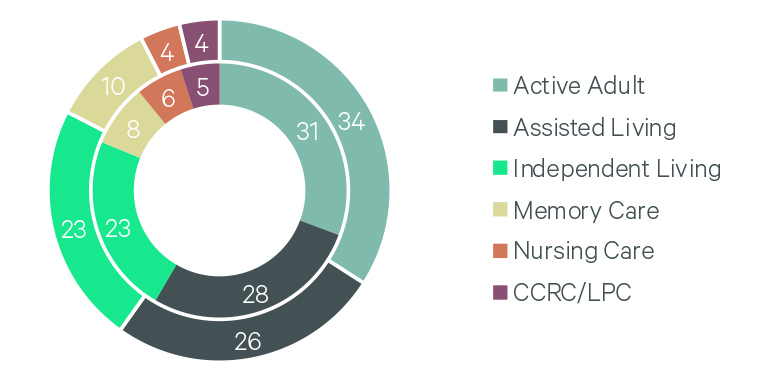

What seniors housing care level do you see as the biggest opportunity for investment?

Active Adult remained the most favored sector by survey respondents. Active Adult communities are benefiting from the leading edge of the baby boom generation, typically comprised of younger, lower-acuity residents.

The Assisted Living and Independent Living sectors ranked second and third, respectively, on the opportunity list.

Figure 8: Biggest Opportunity for Investment (%)

Source: CBRE Seniors Housing Investor Survey, 2021 (Inner Ring) and 2022 (Outer Ring).

What is your 12-month outlook for seniors housing cap rates?

Despite rising interest rates and inflation, nearly 50% of respondents expect capitalization rates to remain flat this year, compared with 27% expecting increases. Offsets to market headwinds include prospective post-pandemic rate increases and rising construction costs (replacement costs).

Figure 9: 12-Month Cap Rate Outlook (%)

Source: CBRE Seniors Housing Investor Survey, 2022.

Operational & Underwriting Trends

Respondents were asked how they were underwriting rental rate trends during the next 12 months.

For Active Adult, Independent Living and Memory Care assets, more than 70% of respondents indicated they were underwriting rental rate increases of between 1% and 7%, with 42%+ utilizing an increase of 3% to 7%. Furthermore, 80%+ of Active Adult and 90%+ of Independent Living and Memory Care underwriting used a 1%-to-7%+ increase in rental rates.

Skilled Nursing and CCRC/LPC communities indicated applied rate increases of 0-7%, with the highest percentage of respondents reporting a range of 1% to 3%. The Skilled Nursing Care level is highly subsidized, with less direct control over increasing rates compared with lower-acuity communities.

Figure 10: Underwriting Rental Rate Trends

Source: CBRE Seniors Housing Investor Survey results, 2022.

For communities that lost residents during the COVID pandemic, what is your projected period to reach pre-COVID levels?

86% of respondents expect Active Adult and Independent Living communities to reach pre-pandemic resident levels within 18 months. For higher-acuity communities, the reabsorption period extends to 24 months, according to 89% of respondents. When compared with the 2021 survey, there was a 6% overall increase in respondents expecting a 0–18-month range, while there was a 102% increase in respondents expecting a 0-6-month range.

Figure 11: Pre-COVID Stabilization Period Projections

Source: CBRE Seniors Housing Investor Survey results, 2022.

For communities that lost residents during the COVID pandemic, what absorption rate are you underwriting?

More than 90% of respondents expect absorption of one to nine units per month for Active Adult and Skilled Nursing communities. 85% expect a pace of one to six units per month.

Figure 12: Absorption Rate Underwriting

Source: CBRE Seniors Housing Investor Survey results, 2022.

Seniors Housing Market Headwinds

For the first time in the Seniors Housing & Care Investor Survey’s history, respondents were asked to rank the highest perceived threats to the industry over the next year.

Figure 13: Highest Perceived Threats to Seniors Housing Industry

Source: CBRE Seniors Housing Investor Survey, 2022.

Querencia at Barton Creek Austin, Texas

Photography: HKS