Intelligent Investment

Connections & Disconnections of Commercial Property Cap Rates

January 16, 2024 8 Minute Read

Executive Summary

- Commercial property capitalization rates (cap rates) arguably are the most closely watched valuation and overall return metrics particularly for major property types.

- Since 2001 cap rates for all property types have remained within a range of under 500 basis points (bps), experienced very low volatility, and are highly correlated. The magnitudes of some outcomes are likely affected by smoothing in the data but not in a meaningful way.

- Cap rate movements reflect both changes in macroeconomic factors and significant changes in property type fundamentals, such as the impact of short-term rentals on hotel assets, e-commerce sales on retail stores, remote or hybrid working on office buildings, and supply chain challenges on warehouse & distribution facilities. Investors should adjust property portfolio weightings when such changes first appear.

- The national data findings, while informative, require verification to be useful for investment decisions in local markets. Local cap rates respond differentially to changes in macroeconomic condition.

Commercial real estate cap rates, a closely followed measure of overall return and a convenient property valuation metric, exhibited low volatility and remained within a narrow range during the past two decades. Cap rate data aggregated across office, retail, multifamily, industrial and hotel properties from Q1 2001 through Q4 2022 averaged 6.29% with a standard deviation of 1.12%. The minimum and maximum cap rates were 4.88% and 8.87%, respectively1. Real Estate Research Corporation (RERC), a data source extending back to Q1 1989, produced close to the same results with an average cap rate of 7.85% and standard deviation of 1.31%2. The RERC data are introduced throughout this Viewpoint as checks for robustness of the CBRE data.

Because the commercial property industry, including investment funds, REITs, brokers and appraisers, is largely organized by property type, cap rates are commonly separately reported for multifamily, industrial, office and retail, representing the four main types, and hotel, health care and specialty real estate uses. These category-specific cap rates are thought to contain useful information, such as rental and supply conditions in each category, that is obscured by relying on the aggregate cap rate, a problem often referred to as aggregation bias.

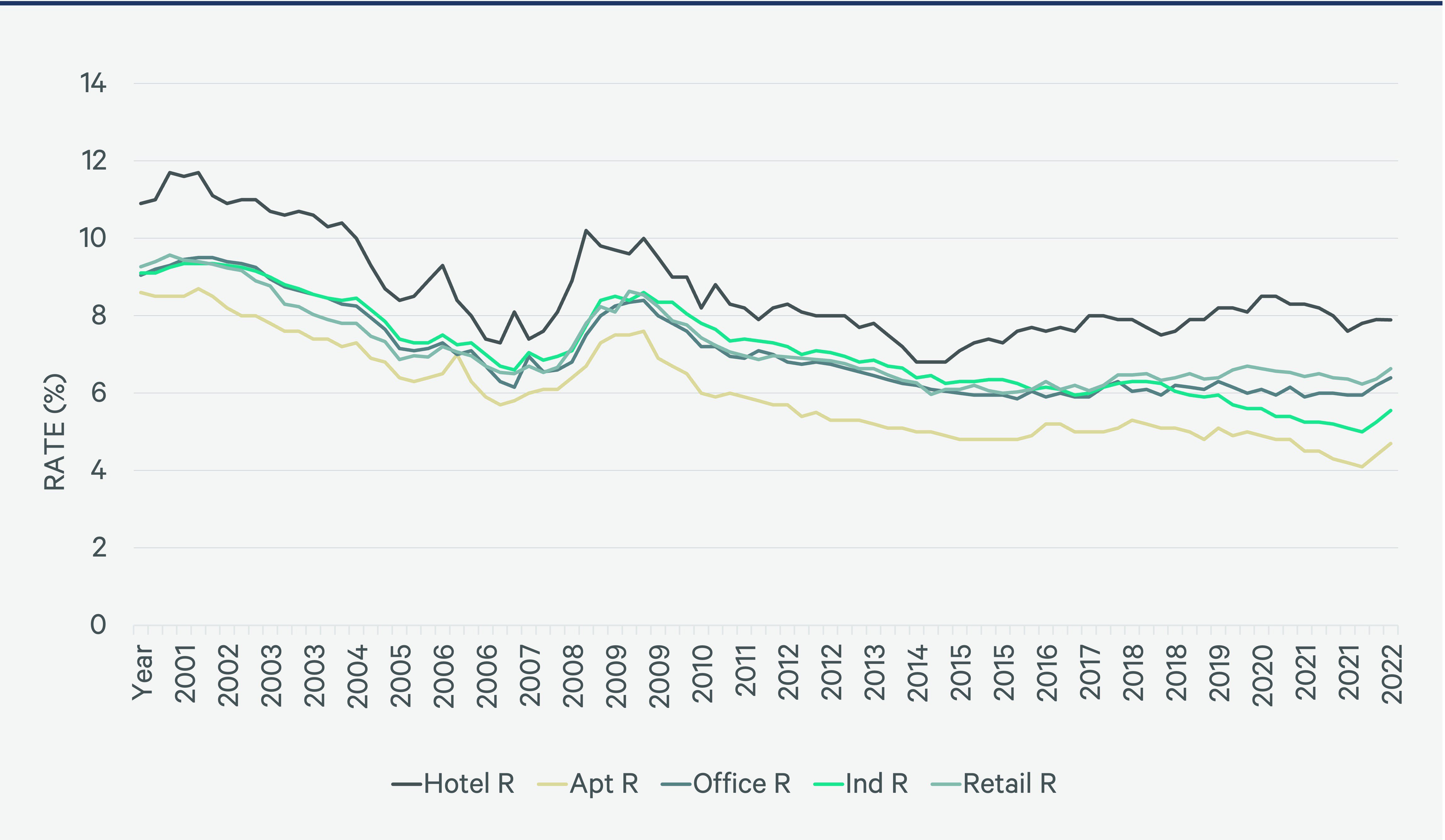

Historical cap rate data exhibit differences across property types, yet the paths through time are quite similar. Figure 1 shows the pattern of property type cap rates reported by CBRE from 2001 through 2022. Declining interest rates meaningfully contribute to the downward trend in cap rates beginning in the early 2000s until recently. The movements across all property types in Figure 1 are remarkably consistent except for hotel cap rates, which departed from the prevailing pattern beginning in the early 2010s. Figure 2 shows the RERC data for the same property type cap rates over the same period. These time series closely resemble those in Figure 1, although the departure of hotel cap rates appears approximately two years later.

A plausible hypothesis to explain the upward movement of hotel cap rates away from trend since the early 2010s is the contemporaneous rise of online short-term rental availability. In 2009 Airbnb logged revenues of $850,000. By 2012 revenues grew to $45 million, and in 2017 they were $2.5 billion. The emerging supply surge of paid accommodation properties during the 2010s may have caused investors to rethink future hotel performance thus elevating overall return requirements. A growing share of the 140 million U.S. homes suddenly became competitors to traditional hotels.

Figure 1: CBRE Commercial Real Estate Cap Rates, Q1 2001 — Q4 2022

Figure 2: RERC Commercial Real Estate Cap Rates, Q1 2001 — Q4 2022

Why Property Type Cap Rates Should Differ — The Conventional Wisdom.

If the levels and period-to-period changes across property type cap rates are statistically different from one another, then aggregate cap rate data disguise important information regarding differences in the financial performance of individual property types. Relying on aggregate commercial property metrics would distort return comparisons with securities, misrepresent portfolio allocations, and lend credence to property type return reporting and diversification.

The rationale for commercial property portfolio diversification is based on the existence of different demand drivers and institutional arrangements across the sectors. Few REITs, for example, own more than one type of property in part due to the high information costs of investing in more than one sector, but mainly because securities investors can practice homemade diversification across specialized firms.

Why Property Type Cap Rates Should Be Similar.

Important commonalities across the commercial real estate spectrum exist in both the space and capital markets. The space market commonalities argument comes from the recognition that all real estate generates income through utilization of the built environment and is subject to the same macro and regional economic forces. J. Gyourko uses these arguments to explain why he finds evidence that commercial property and housing values “within the same metropolitan market behave quite similarly over time. They move together contemporaneously and have similar time-series patterns.3”.

Commonalities across property types also are evident in the capital markets because all real estate is subject to prevailing credit conditions emanating from the macroeconomy. D. W. van Dijk and M. K. Francke recently performed a study on the liquidity of commercial real estate across property types and cities4. They report that both the space and capital markets across divisions are highly integrated – capital markets more so than the space markets. This means that investors need not incur the costs of diversifying away liquidity risk by managing portfolios of commercial real estate with different property types and cities because “liquidity may dry up in all markets simultaneously.”

Finally, capital market integration underlies the construction of CBRE’s cap rate forecasting models for property types and cities5. The model, fashioned after the Gordon Growth formula, makes cap rates a function of two capital market measures and one space market measure (theoretical signs in parentheses),6

- The risk-free rate (+)

- The risk premium or difference between corporate bond and risk-free rates (+)

- A measure of income growth such as the change in a rent index (-)

These discussions regarding property type cap rates lead to the following null hypotheses:

- There is no statistical difference in the means, standard deviations, and period-to-period changes of commercial property type cap rates.

- There is no statistical difference in commercial property type cap rate movements over time as measured by their correlation coefficients.

Conventional wisdom leads to expectations that both hypotheses will be rejected.

2 From quarterly investor surveys. Real Estate Research Corporation (SitusAMC), Real Estate Report.

3 J. Gyourko, “Understanding Commercial Rel Estate. How Different from Housing is it?” Journal of Portfolio Management, 2009, vol. 35, p.23.

4 D. W. van Dijk and M. K. Francke, “Commonalities in Private Commercial Real Estate Market Liquidity and Price Index Returns.” Journal of Real Estate Finance & Economics, 2021 published online.

5 See S. Chervachidze, J. Costello, and W. Wheaton, “The Secular and Cyclic Determinants of Capitalization Rates: The Role of Property Fundamentals, Macroeconomic Factors, and Structural Changes.” Journal of Portfolio Management, 2009 Special Real Estate Issue, p. 50.

6 An availability of credit measure for commercial real estate investment also appears in these regression equations but plays a relatively minor role.

Analyses of Cap Rate Data

Property Type Cap Rate Data and Study Notes

The CBRE cap rate data come from the NCREIF portfolio that is mostly comprised of NOIs and asset pricing information from investment-grade properties contributed by its member fiduciary investment managers. These data, therefore, underrepresent Class B and C quality properties. In addition, because the asset pricing metrics are a mix of transaction prices and appraised values, some amount of smoothing of the cap rate time series should be expected. The CBRE hotel cap rates, however, come entirely from transactions and tend not to be as concentrated as the NCREIF data in investment-grade properties and much less subject to smoothing.

Differentially, the RERC surveys from which the cap rates originate include respondents involved with first-, second- and third-tier properties. While the aggregate data for each property type may be smooth to some degree due to repeat respondent anchoring, they are not over weighted in investment-grade assets.

The results reported from this study rely on quarterly cap rate information extending more than two decades. While an analysis is performed on the quarter-to-quarter changes in property type cap rates, the focus is on long-run movements. This orientation aligns with the widely held belief that non-securitized commercial real estate is a long-term investment. High transaction costs severely limit short-term profit taking.

Descriptive Statistics and Analysis of Cap Rate Levels

The statistical story about property type cap rates from 2001 through 2022 begins with descriptive statistics and correlations presented in Panels A and B of Figure 3. Both CBRE and RERC cap rate statistics appear. The information in Panel A confirms that cap rates across all property types experienced low volatility as evidenced by the standard deviations relative to the means. These coefficients of variation (C.V.) are .25 or smaller in all cases across both data sets. The results align with NCREIF experience over the same period. Publicly traded real estate securities by contrast have higher C.Vs.

In addition, the data period encapsulates different market conditions including three recessions (i.e., 2001-2002, 2007-2010, and 2020) yet none of the property type cap rates varied by more than 500 bps from highest to lowest during these periods. As seen in Figures 1 and 2, all property type cap rates exhibit some upward movement during the 2007-2010 recession, but very little change occurred during the COVID period.7

Figure 3: Property Type Capitalization Rate Statistics, Q1 2001 — Q4 2022

The correlation coefficients in Panel B provide evidence of how closely aligned property type cap rates have been since 2001. Most combinations exceed .95. The relationships between hotel cap rates and other property types are weakest, although the correlated coefficients are high from both sets of data.

Statistical tests of differences in means and standard deviation provide mixed results regarding the commonality of property type cap rates. Figure 4 shows the T-test and F-test statistics for these tests. The following are observations about these results:

- Most of the means tests across both samples indicate that property type cap rates embody unique information about a property category’s valuation and overall return fundamentals. Office/retail and industrial/retail combinations are notable exceptions.

- Importantly, hotel cap rate means are consistently different in a statistical sense from all other property type cap rates. Given that hotels have the only non-lease protected income streams in the numerator of the cap rate equation, statistical and economic significance coincide.

- Regarding standard deviations, the null hypothesis cannot be rejected for nearly all property type combinations. This means that over the long-run, and likely short-run, property type cap rates move in concert through time.

Figure 4: Property Type Capitalization Rate Statistical Tests of Differences, Q1 2001 — Q4 2022

Source: CBRE and RERC.

Quarterly Changes in Property Type Cap Rates

The possibility exists that the cap rate data disguise information about property type fundamentals that may be uncovered by examining quarterly cap rate movements. Seasonality might affect quarter-to-quarter changes without adjustments, especially for hotels. Tests for seasonality failed to show any irregularities in the patterns of property type cap rates within annual periods. Figure 5 presents correlation coefficients and difference in means test statistics for quarterly changes in property type cap rates (only CBRE data results shown). The correlations again are strong although decidedly lower for quarterly changes than levels across hotel combinations for the reason described above. The difference of means tests indicates that over the long run property cap rates move in sync quarter-to-quarter. The changes do not identify any unique, underlying property type trends.

Figure 5: Property Type Capitalization Rate Quarterly Changes, Q1 2001 — Q4 2022

Source: CBRE and RERC.

Conclusion

Both independently derived data sets analyzed in this study show that certain property type cap rates are higher than others, but they all demonstrated similar movements through time as indicated by high correlations and statistically significant quarterly changes. One exception is the hotel cap rate increases and deviation from cap rate trend beginning in the early 2010s. Another exception has been observed during recent years as retail and office cap rates began rising above industrial cap rates for the first time this century. The likely causes are online retailing and COVID plus a concurrent technological advancement that promoted increases in remote or hybrid working. Beginning late last decade, retail and office cap rates rose above industrial cap rates for the only time this century (see Figures 1 and 2). A change in how consumers purchase goods benefited the warehouse component of the industrial sector while disadvantaging traditional retail performance.

The persistence of the hotel cap rate break from trend suggests a structural shift. The recently observed relationships between retail, industrial and office cap rates may indicate other structural shifts yet to be supported by persistence.

Suspected smoothing in both data sets represents a possible limitation on strict interpretations of the results. Smoothing could be responsible for the very low standard deviation and high correlation estimates. However, hotel cap rates based entirely on independent quarterly samples of transaction behaved similarly to other property type cap rates during the sample period. This suggests that smoothing effects may lower standard deviations and elevate correlations but not in a meaningful way. Note that smoothing does not affect the means. In addition, the two samples have different contributions of Class A, B, and C properties yet the visual patterns and statistics are indistinguishable.

Academic research has put forward the idea that all real estate performance is driven by the same forces (i.e., commonalities) such as land economics, other physical production input prices, and capital market conditions. The statistical evidence presented herein aligns with this proposition and not the conventional wisdom that idiosyncratic fundamental forces result in property type performance measures that show very different patterns over time. The fundamental forces underlying each property type cap rate suddenly appear as either short-term movements or structural shifts. These deviations from long-run trend are obscured.

Some implications for commercial property investment emerge from this study.

- The results of this study affirm the long-term nature of commercial real estate investment with respect to macroeconomic conditions. The cap rate analytics indicate that investors should not divest of any property type for another during economic downturns because modern cycles tend to be short in duration and all property type cap rates respond in similar ways.

- The departures from the pattern all property type cap rates followed during most of this century either occurred because of short-term events or structural shifts. Private commercial real estate investors are unable to profit from short-term movements but have opportunities for excess returns by early recognition of structural changes and subsequent portfolio rebalancing. No easy task as recognition of structural changes is more art than science.

- One limitation on interpretations of findings from analyses of national data is their lack of direct transferability to local investment markets. The cap rates in these markets respond to changes in macroeconomic conditions in different ways and local economic conditions affect property type cap rates. Investors can benefit from the reporting of national cap rates to understand local market pricing by performing statistical analyses of the relationships between national and local market cap rate time series and structural shifts.

Related Service

- Property Type

Hotels

CBRE Hotels delivers bottom-line impact to hotel clients globally by providing advisory, capital markets, investment sales, research & valuation s...