Intelligent Investment

Retail’s Hidden Gem: Open-Air, Non-Grocery-Anchored Centers

May 19, 2022 5 Minute Read

Looking for a PDF of this content?

Executive Summary

Continued caution about the retail sector has masked an opportunity in open-air, non-grocery-anchored retail, which offers some of the best risk-adjusted returns in commercial real estate today. The pendulum has swung too far against open-air and, in the coming years, both rent growth and cap rate compression may surprise on the upside. Open-air, grocery-anchored centers remain an attractive investment option. At the same time, the risk discount associated with non-grocery-anchored (when compared with grocery-anchored) open-air centers may be too wide and creates a buying opportunity at an attractive, risk-adjusted return.

This optimism is based on three factors:

- The Worst Is Over

Open-air retail has gone through a period of great consolidation and transformation, the e-commerce growth rate is flattening and brick-and-mortar is now poised for growth. - Strong Consumer Balance Sheets

Thanks in part to COVID stimulus, most consumer balance sheets (savings and debt levels) haven’t been this strong in decades. Additionally, the adoption of hybrid working strategies means employees will more frequently be working from home offices, which will increase foot traffic in nearby suburban retail, including open-air, non-grocery-anchored retail. - Cap Rates Too High Relative to Rent-Growth Projections

When compared to the cap rate/rent-growth-projection relationship of other commercial real estate asset types, retail is significantly undervalued. Growing institutional interest will provide additional opportunity for cap rate compression in the sector.

These factors combine to present open-air, non-grocery-anchored retail as a compelling opportunity with upside from both expected rent growth and declining cap rates.

Is the coast clear?

No doubt it takes strong conviction to declare “the coast is clear” for brick-and-mortar retail after the challenges of the last decade. But underpinning such optimism are the ongoing improvement of brick-and-mortar retail sales, the lack of new supply coming on the market and the slowing of e-commerce sales growth, which is now below trend. Retailers are also, on balance, healthier: In 2021, new store openings surpassed closings for the first time in four years.

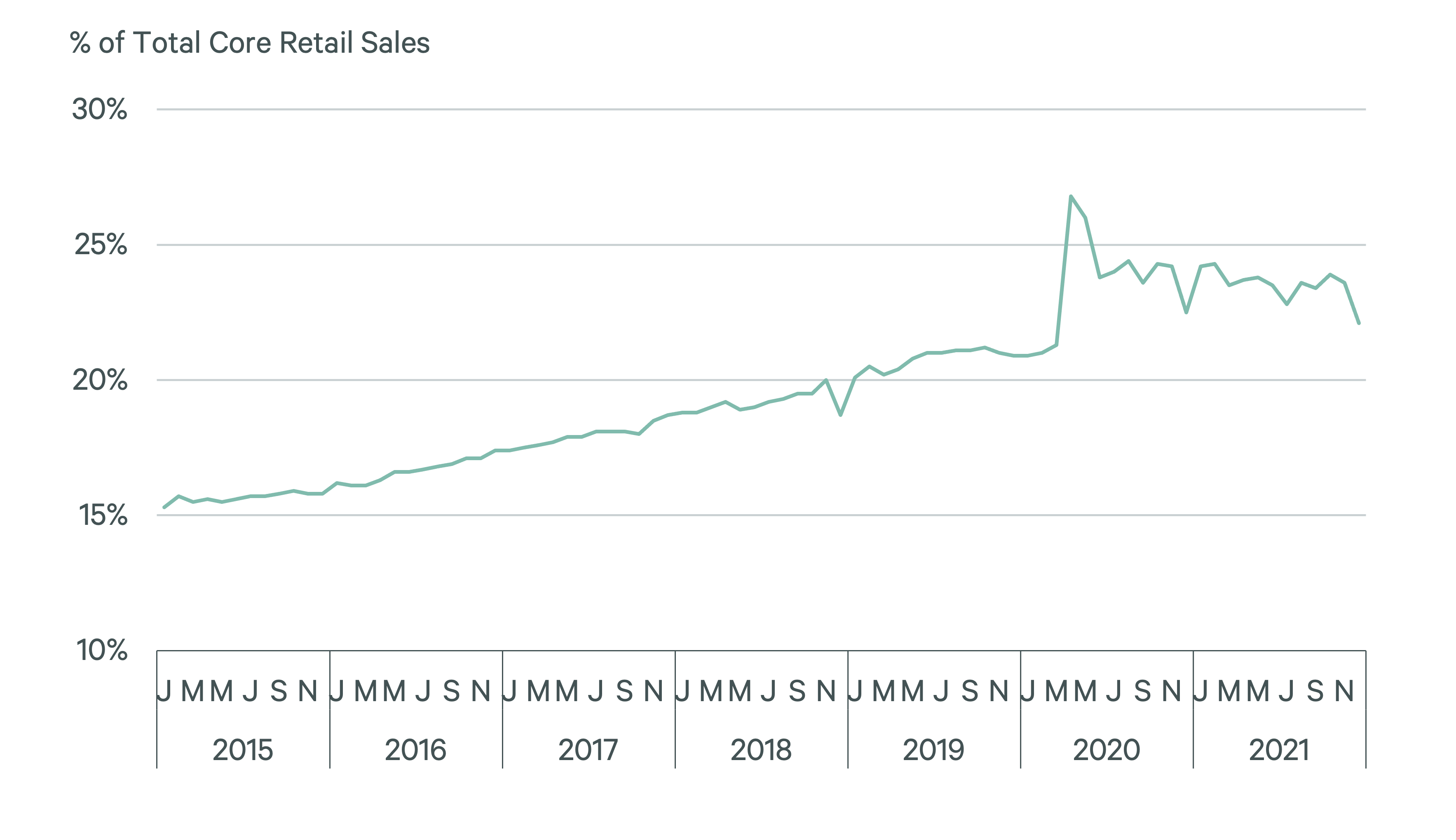

Figure 1: Internet Sales Spiked During Covid but Are Already Flattening and Below Historic Trend

Source: U.S. Census Advance Monthly Retail Sales, CBRE Research, Q4 2021.

People are spending again

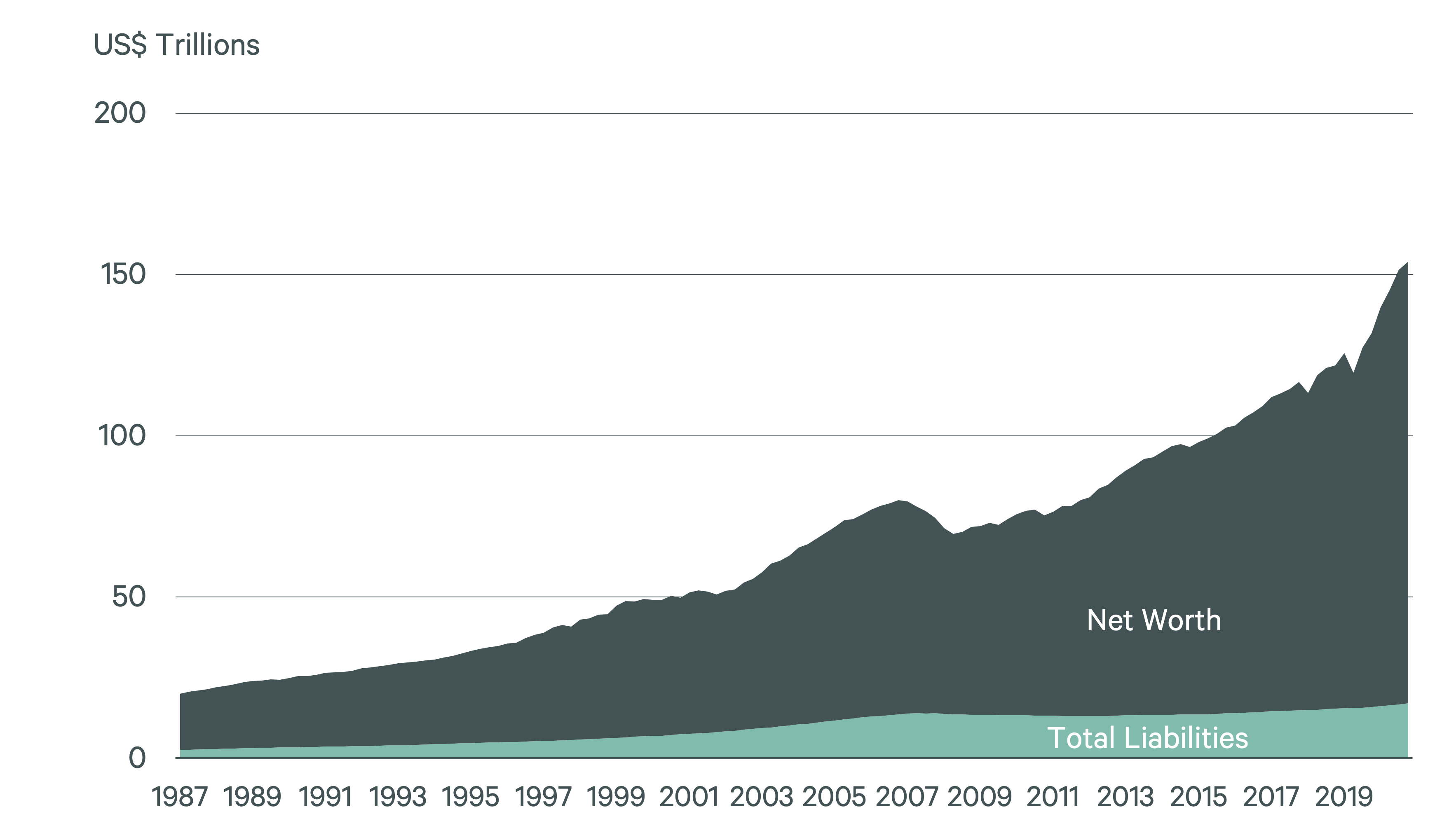

There are few silver linings to the COVID-19 crisis, but one is that consumer balance sheets are the strongest in decades, thanks to government support and the pay down of debt.

Figure 2: U.S. Household Wealth Has Surged

Source: St. Louis FRED, CBRE Research, 2022 Q1.

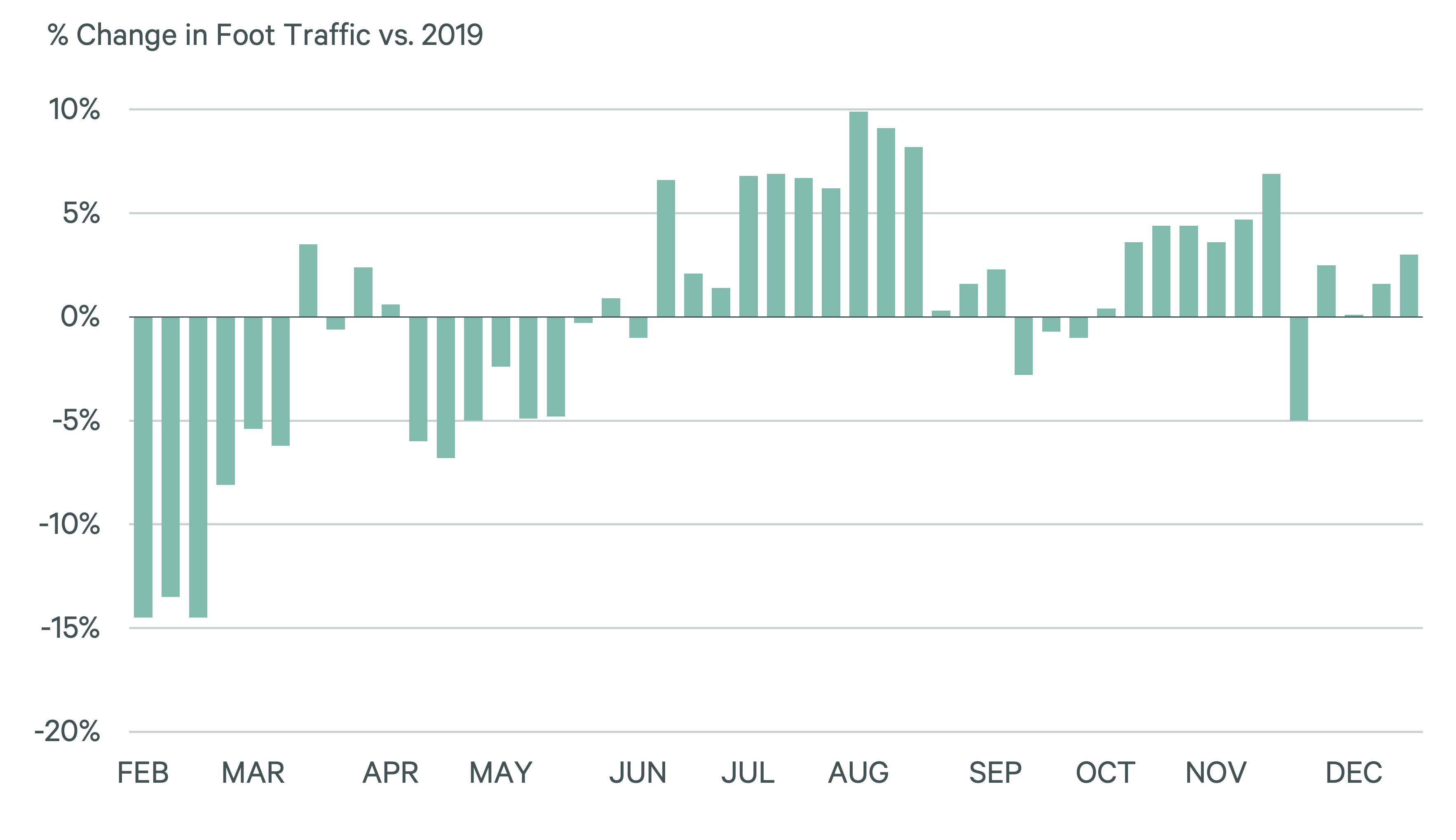

These factors, combined with post-COVID pent-up demand, should stimulate higher traditional retail sales. According to the March 2021 PwC Global Consumer Insights Pulse Survey, purchasing physical goods in a physical store is the preference of most consumers.

Figure 3: Consumer Retail Foot Traffic Is Already Coming Back

Source: Placer.ai.

Institutional investors are raising the bar

A familiar adage in commercial real estate is that “it takes as much time to underwrite a $20 million asset as a $200 million one.” This is why institutional investors continue to raise their minimum threshold for asset purchases. Institutions’ collective turn away from retail assets in the past decade helped to drive cap rates higher.

Figure 4: Unsuccessful Property Bids by Company Type

Source: CBRE Connector.

Now we are starting to see more institutions bid for deals in the market, which will be reflected in the data in the coming quarters. An analysis of losing bids for investment properties in retail shows a clear trend of growing institutional interest in the sector.

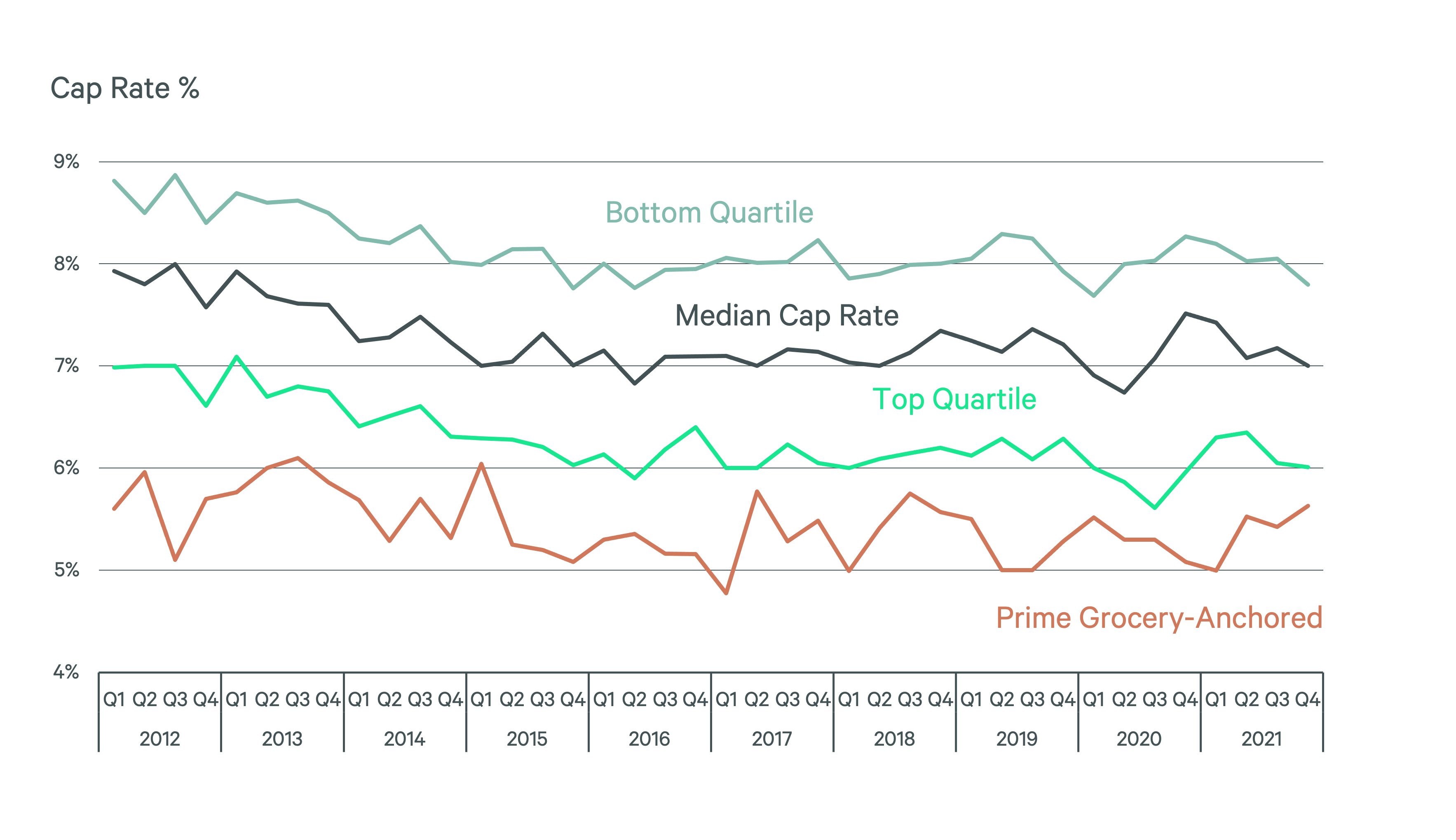

Why not include grocery?

Grocery-anchored retail has been a port in the storm over the past decade. These have been among the few retail assets, along with the most well-situated malls, to garner consistent institutional investor interest. As a result, they are priced at a premium—typically 100 to 300 basis points more than non-grocery-anchored retail.

Figure 5: Significant Yield Premium for Grocery-Anchored Retail

Source: Real Capital Analytics, Q4 2021.

The investment case for open-air, non-grocery-anchored retail is buoyed by most retailers’ embrace of omnichannel solutions, including reformatting stores and culling unprofitable locations. Grocers, by contrast, typically enter into anchor leases with below-market rents at terms ranging from 20 to 30 years, as their presence helps to attract additional tenants. Because of the long-lease term, some grocers have not yet evolved their footprints to account for omnichannel. Furthermore, grocers have the lowest e-commerce penetration among all major retail types, and their online sales are expected to grow the fastest. The outlook for grocery stores may not justify the continued yield premium over other forms of retail.

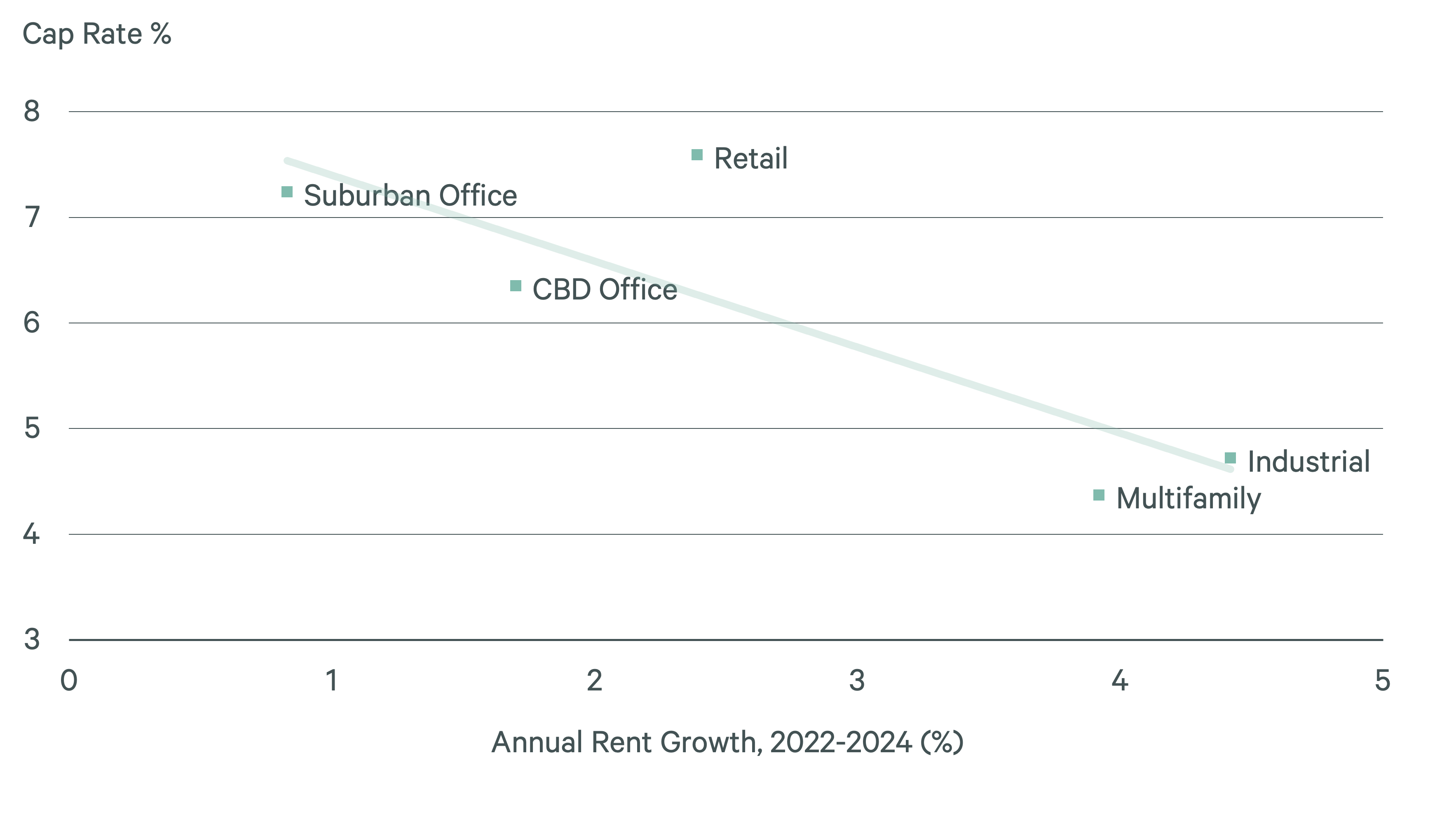

Conclusion - CBRE's Cap Rate Survey reveals risks and opportunities

Figure 6: Asset Pricing Relative to Forecast Rent Growth

Source: CBRE Econometric Advisors.

Optimally, commercial real estate investors most desire assets with potential upside from both market fundamentals and capital flows. Based on CBRE’s most recent Cap Rate Survey, retail appears to be well positioned on both and valued significantly below other commercial real estate asset types when comparing cap rates and rent-growth projections.

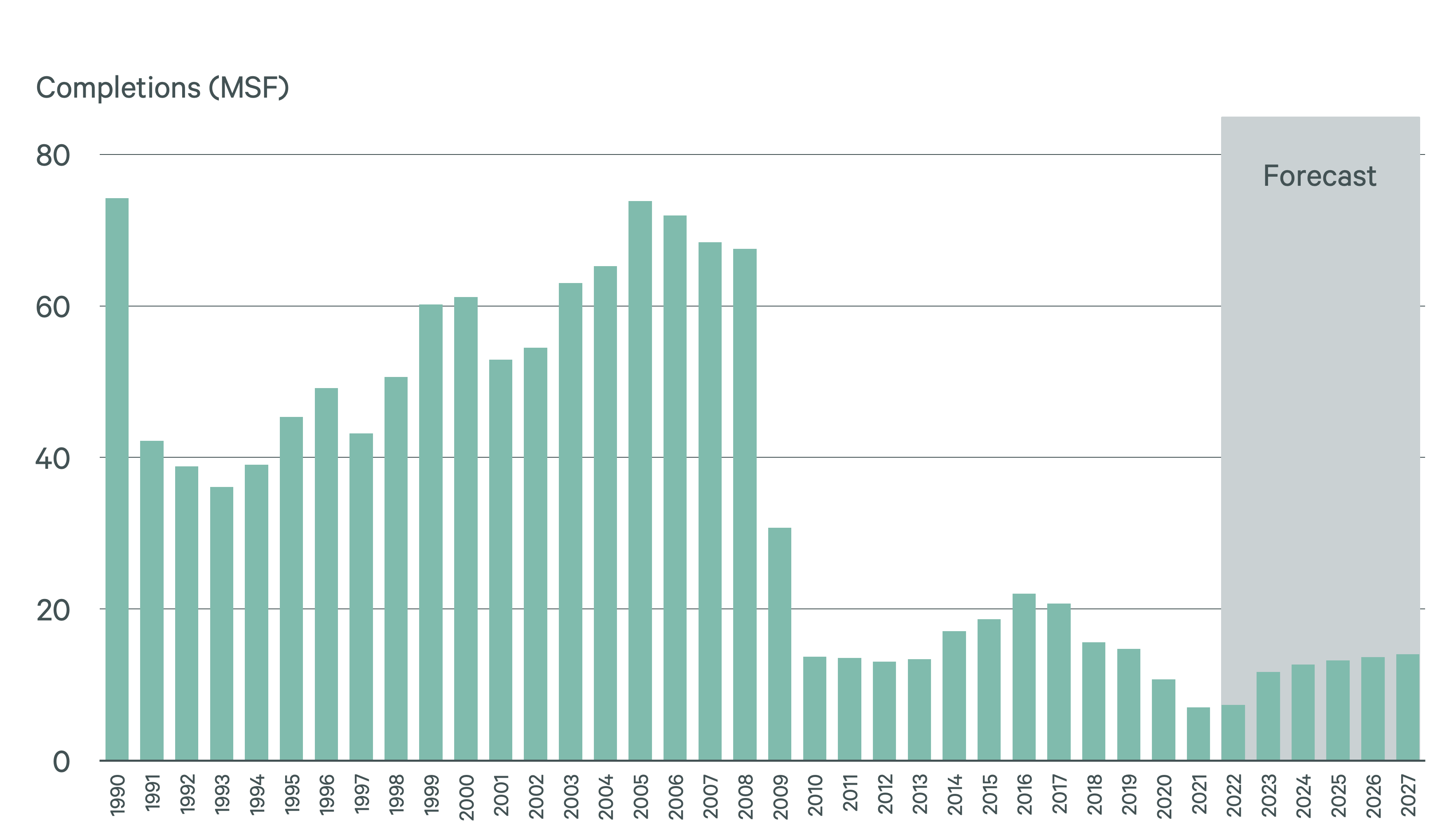

Figure 7: New Construction, Neighborhood & Strip Retail

Source: CBRE Econometric Advisors.

Up until 2009, retail had been a magnet for new development. However, the growth of e-commerce has curbed new construction sharply, particularly neighborhood and strip centers. We expect new retail construction to remain modest. The lack of supply growth, coupled with improved fundamentals, will constrain available supply and undergird continued rent growth.

For years, commercial real estate investors have struggled to find high-yielding assets. Now open-air, non-grocery-anchored retail is emerging as a significant buying opportunity. Retail sector fundamentals are improving and as more institutional investors rediscover open-air, non-grocery-anchored assets, we expect a wave of capital to compress cap rates.

.jpg)