Intelligent Investment

The Flight to Quality Quantified

Prime assets have outperformed non-prime since the start of the pandemic.

August 12, 2022

Receive EA Insights Directly in your Inbox

Executive Summary

The trend of “flight to quality” has gained momentum since the pandemic started and employee work patterns shifted to an increasingly virtual model. And the reimagination of office space, along with virtual work trends, will only accelerate tenant moves to prime office properties. The virtual-work-induced shortfall in office demand is felt almost exclusively in non-prime buildings.

- Demand has shifted to the top of the market, at the direct expense of more commoditized office stock. The average prime net absorption rate from Q2 2021 to Q2 2022 for five observed downtowns is 0.2%, compared with -0.7% for the non-prime assets in these downtowns.

- Rents for prime assets have continually outpaced those of non-prime assets, with cumulative prime rent growth over 13% since 2018.

- After Q1 2020, the vacancy rate for non-prime assets increased much faster than that of prime assets. The non-prime group’s vacancy rate increased 8.2% while the prime group increased 5.1% from Q1 2020 to Q1 2022.

- A high-quality building with sustainable features will carry less transition risk going forward, making it more valuable than its peers and easier to attract environmental-conscious tenants and investors.

- The competitive advantage of individual prime buildings will vary by market depending on current and future inventory of top-quality buildings.

Pandemic Accelerates Outperformance of Prime Office Assets

With the local expertise of our CBRE colleagues, we identified a set of prime assets in five major U.S. downtowns (San Francisco, Boston, Manhattan, Washington, D.C. and Seattle) to study flight-to-quality trends. We analyzed activity and performance among prime and non-prime office properties. In our case study, the stock of prime assets amount to more than 122 million square feet (MSF), around 17% of the total stock of these five downtowns.

Rent

We first examined taking rents (the first-year rent on closed transactions, not accounting for concessions), collected from our local research teams. The prime buildings recorded cumulative rental growth of 13.4% from 2018 to 2021, compared with only 2.5% from non-prime Class A buildings. If we factor in inflation, non-prime rent growth would be non-existent. Boston is an exception, with non-prime Class A starting rents showing double-digit growth.

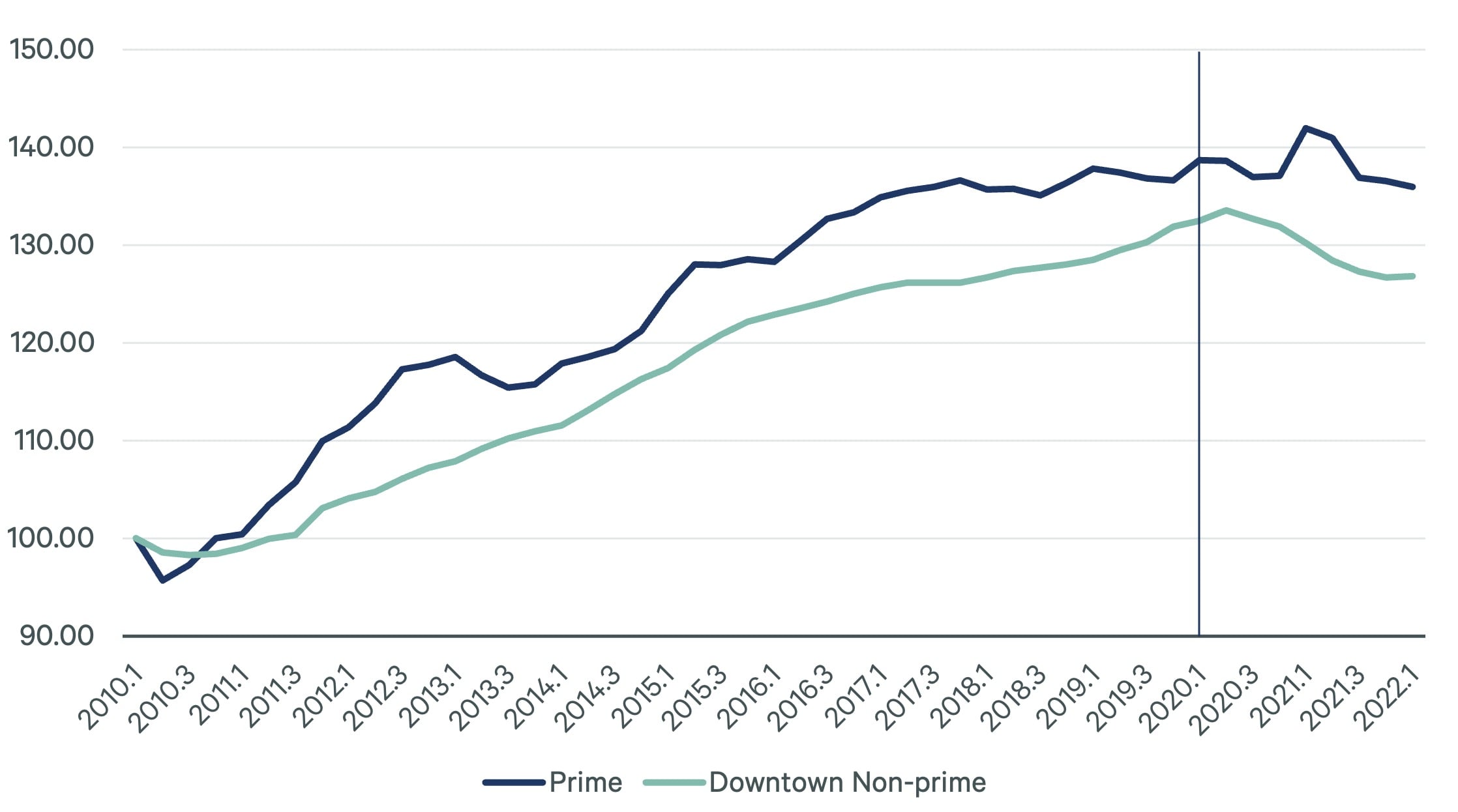

To better show the trendline, we indexed Q1 2010’s rent as the baseline for each of the downtowns and calculated a simple average of these five series. Figure 1 shows that the two building sets head in different directions after Q1 2020. Non-prime buildings show a clear decline in rent levels beginning in 2020, but the prime set seems to retain value relatively well. Prime rents as of Q1 2022 declined 1.3% compared with Q1 2020, but the rest of the buildings in these downtowns saw rents drop 5.2% over that period.

Figure 1: Select Metros’ Downtown Asking Rent (2010.1=100)

Source: CBRE Econometric Advisors.

Net Absorption and Vacancy

We aggregated building-level vacant spaces and stock data to calculate net absorption, focusing on Q2 2021 to Q2 2022 . For prime buildings, all but Seattle are seeing prime net absorption higher than non-prime. The net absorption rate is consistently positive across the cities we chose (except for Seattle and Manhattan, which has a few large outliers that impacted the total prime net absorption rate). For non-prime assets, net absorption was negative in San Francisco, Manhattan and Seattle but stayed positive in Boston and D.C. Boston benefited from its diversified industry and flourishing bio-tech and pharmaceutical firms which also take on traditional office spaces; Washington, D.C. benefited from federal government related entities (for example, General Service Administration recently leased more than 300,000 sq. ft. in a non-prime asset). On average, the net absorption rate from Q2 2021 to Q2 2022 for the five downtowns is 0.2%, compared with -0.7% for the non-prime assets.

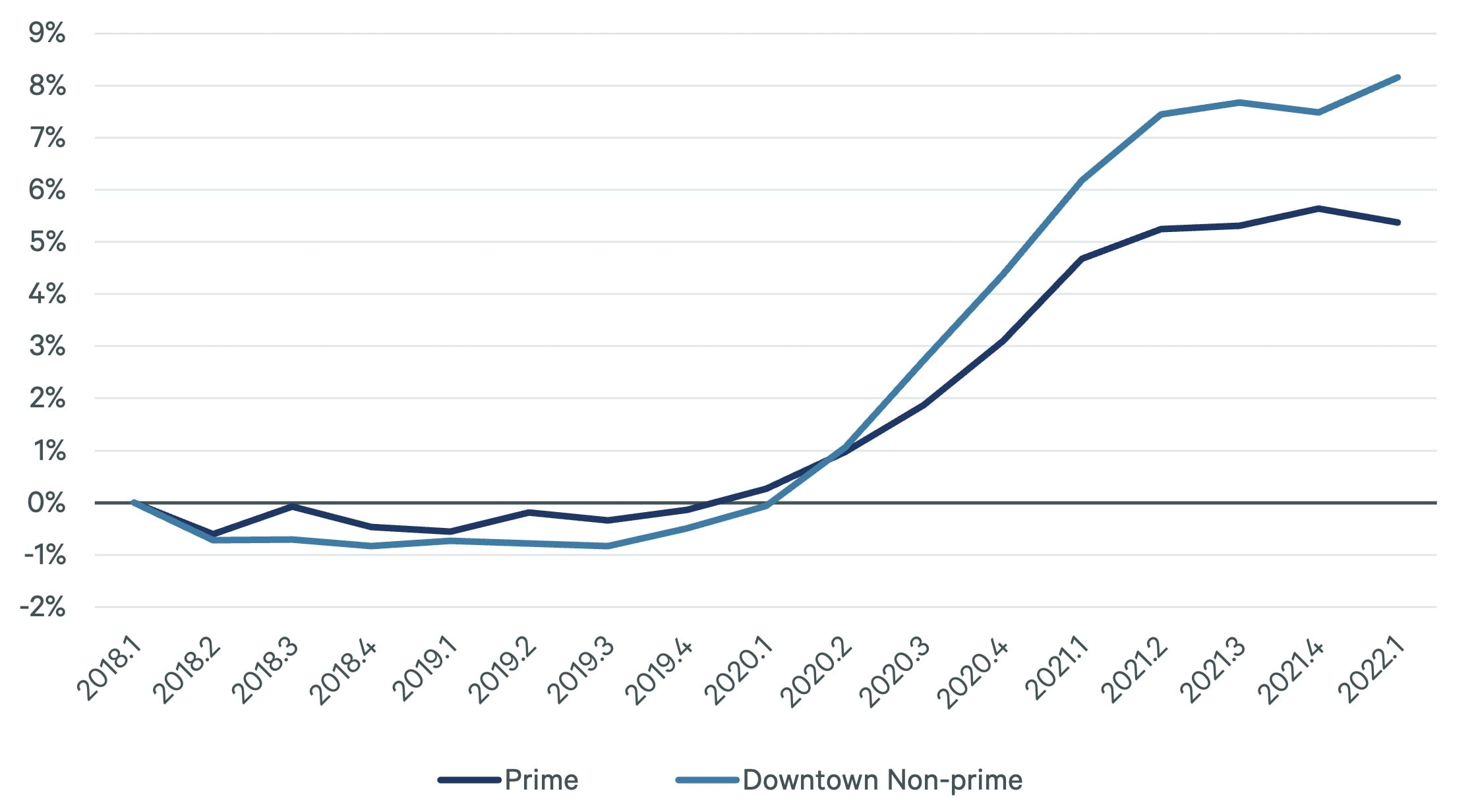

The average vacancy rate from Q1 2018 to Q1 2022 for prime and non-prime assets in those five downtowns (aggregated) did not show significant difference before the pandemic but after Q1 2020, the vacancy rate for non-prime assets increased much faster than that of prime assets (figure 2). The non-prime group’s vacancy rate increased 8.2% while the prime group increased 5.1% from Q1 2020 to Q1 2022. This vacancy outperformance occurred even as the prime set added 1.6 MSF of stock since Q1 2020 via new construction or major renovation. The different trajectory is another indication that market preference has shifted, with tenants putting more emphasis on experience, new technology etc. rather than simply viewing offices as a place to work.

Figure 2: Vacancy Rate Change (Q1 2018 = base)

Source: CBRE Econometric Advisors.

Risks to Existing Prime Assets

Although construction completions will decrease in the coming years, these highest-quality assets will pose stiff competition to existing prime assets. Understanding supply-side pressure is key to assessing the future competitiveness of prime assets in certain markets.

Although prime assets are the best of Class A and a much more selective group, it is fluid. Newly built Class A assets potentially could be a strong competitor if they provide what tenants demand. In some markets, a large amount of new construction has been taking place in recent years, offering more quality spaces for tenants to choose from, thus creating more risks of quality spaces being unoccupied or having less relative pricing power as competitive options remain available. Some markets have seen very few new projects over the past decade, making the current quality spaces scarce.

Along with expected construction as a headwind to existing prime stock, we’ve analyzed the amount of Class A space that has been built since 2015 in downtowns across the U.S. With an average lease term of seven to nine years, those buildings built (and leased) around 2015 will see their tenants’ leases expiring soon, potentially releasing large amounts of competitive space to the market.

Understanding supply-side pressure is key to assessing the future competitiveness of prime assets in certain markets.

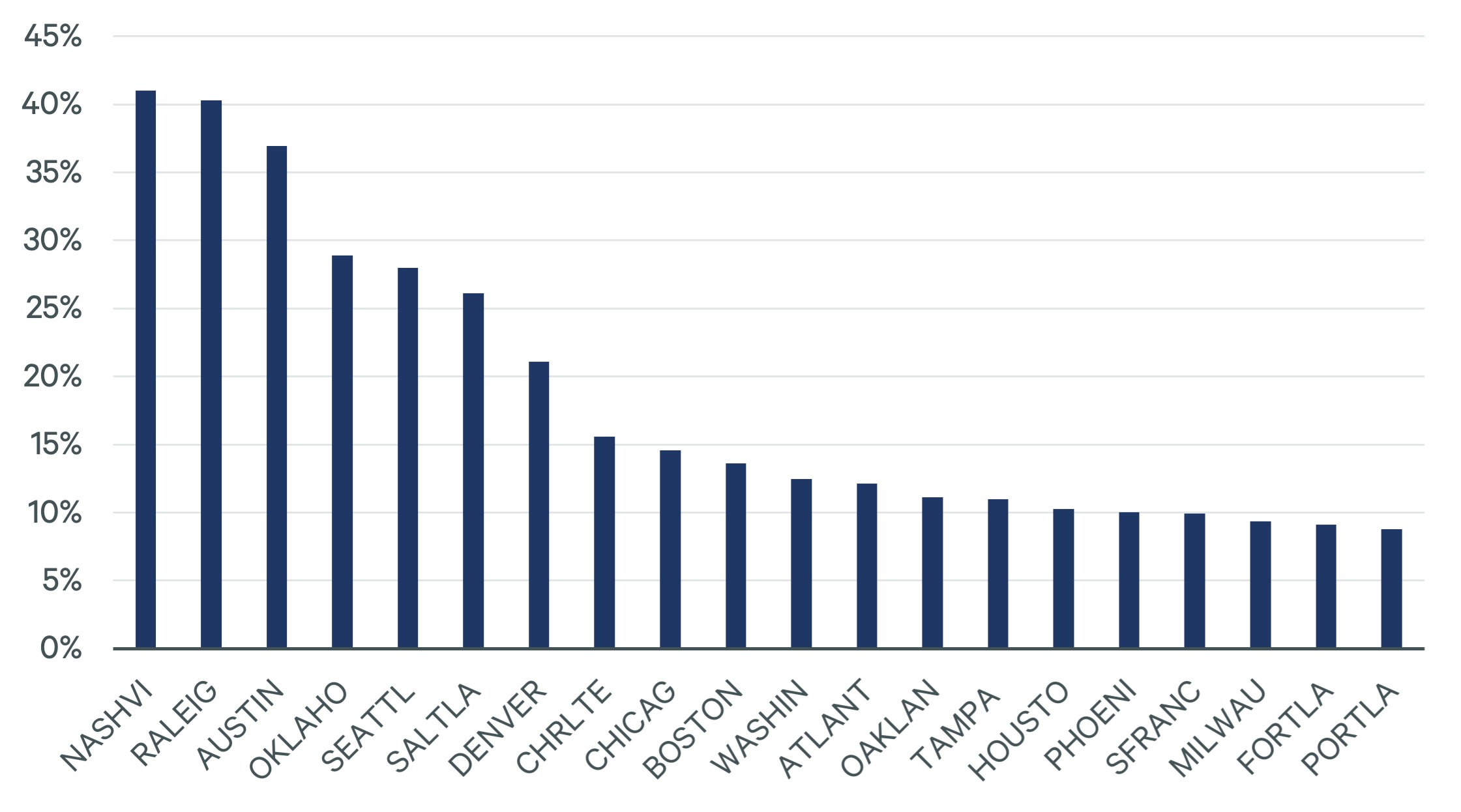

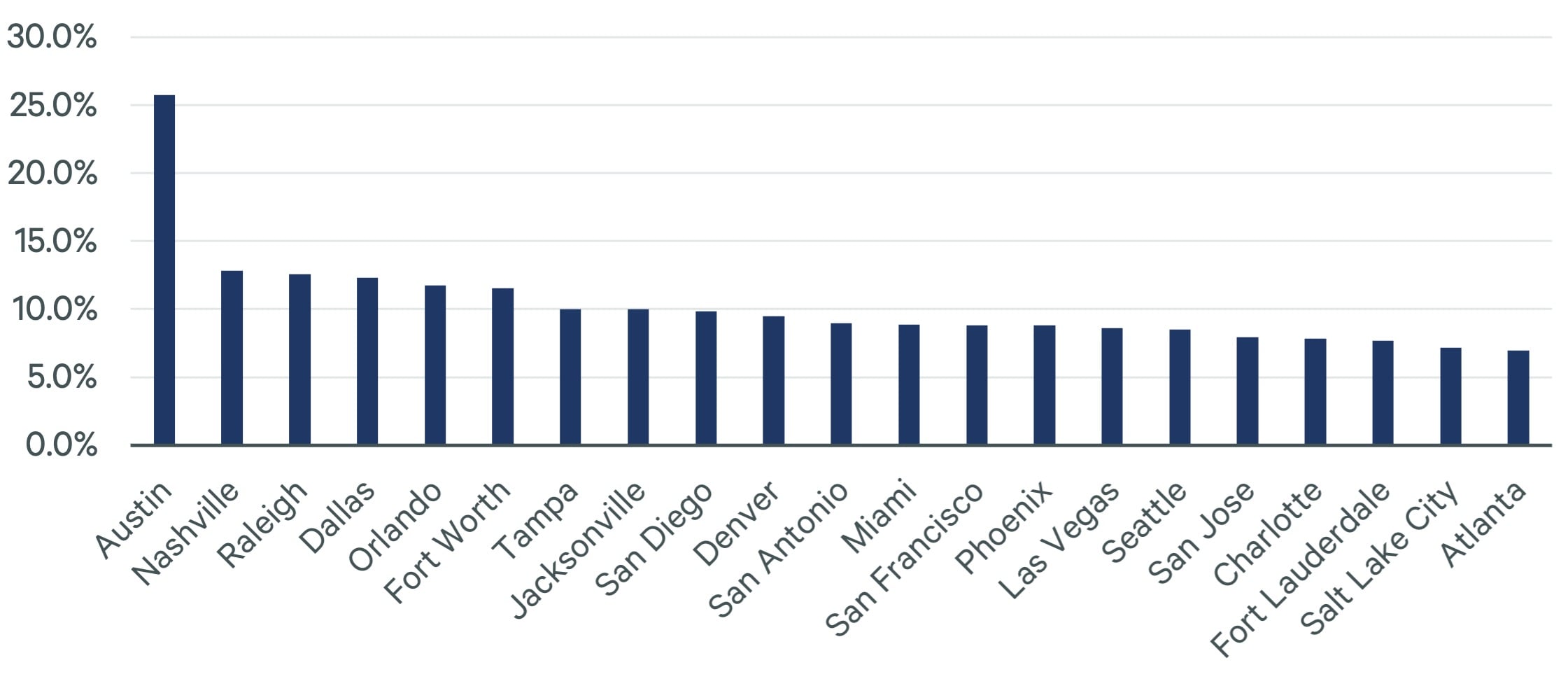

Figure 3 shows the 20 markets with the highest percentage of Class A stock downtown that was built after 2015. More than 35% of the Class A stock in the top three downtowns (Nashville, Raleigh and Austin) was built after 2015. Many of the top 20 markets are Sun Belt markets that have become investors’ darlings in the past few years because of their affordable real estate and strong in-migration. Gateway cities like Seattle, Washington, D.C., Boston, Chicago, Houston and San Francisco were also on the list with more than 10% of their downtown Class A stock built after 2015.

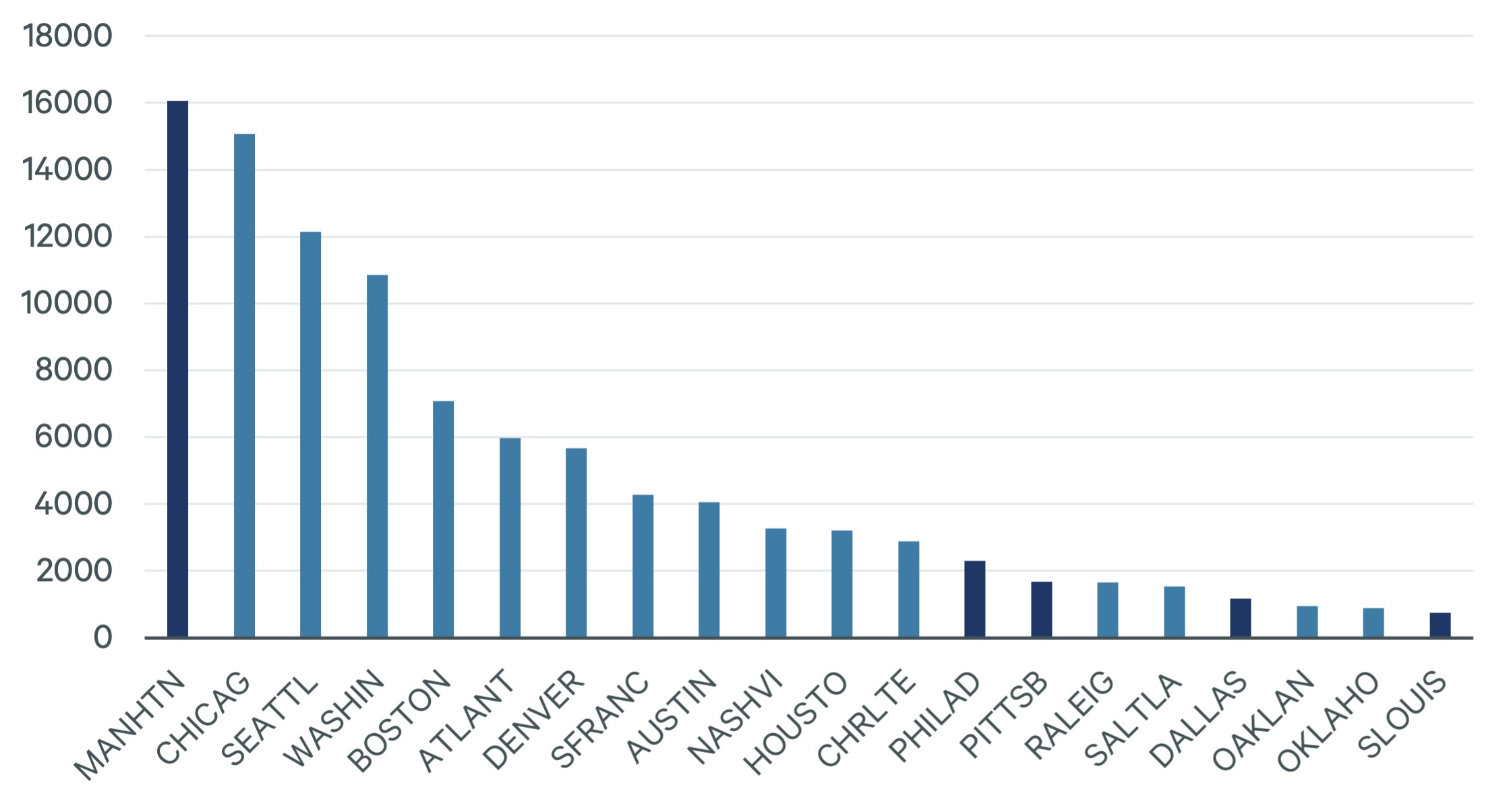

In terms of square footage (figure 4), we see more Gateway cities entering the top 20. Manhattan has more than 16 MSF of Class A space built after 2015 but because the market is so large, this makes up only 5% of downtown Class A stock.

The differences in the makeup of current stock in each metro signals that flight-to-quality will vary by market. Depending on how fierce the competition is, landlords will have to work harder to attract tenants in markets where more Class A new construction or renovated buildings are available or about to be available.

Figure 3: Percentage of Class A Stock in Downtown Built after 2015

Sources: CBRE Econometric Advisors.

Figure 4: Square Footage of Class A Stock in Downtown Built after 2015

Sources: CBRE Econometric Advisors.

Demand also plays a role. Markets like Austin, with strong office-using employment, will likely see spaces being absorbed quickly. Markets like Oklahoma, where office-using employment remains weak and with a high percentage of stock built recently, would likely see less strength at the top of the market.

Figure 5: Cumulative Office-Using Employment Growth (Q1 2020 to Q1 2025)

Sources: CBRE Econometric Advisors.

Is ESG Playing a Role in the Flight-to-Quality Story?

Tenants and investors are increasingly seeking assets with Environmental, Social and Governance (ESG) measures incorporated, and we believe there will be an accelerated obsolescence in commodity assets where tremendous upgrade is needed to comply with ESG standards. We also believe new or recently renovated sustainable prime assets will face much less transition risk going forward.

For the commercial real estate sector, which contributes 30% of the world’s annual greenhouse gas emission and consumes 40% of the world’s energy1, the move toward “net zero” will create a lasting impact.

In January 2020, several U.S. state and local governments launched a coalition to strengthen building performance standards. The Building Performance Standards Coalition aims to reduce emissions across the real estate sector and make buildings cleaner, healthier, greener and more efficient. As of July 2022, 33 state and local governments had joined the partnership with more expected to join.

In March 2022, the U.S. Securities and Exchange Commission (SEC) proposed rules that would require publicly traded companies to disclose how climate change risk affects their business. In May, the SEC proposed two changes to prevent “greenwashing” (misleading claims from ESG fund managers). It’s reasonable to assume investors and property owners are becoming more aware of this trend and of the risks in investing in or owning assets without ESG measures in place.

We believe there will be an accelerated obsolescence in commodity assets where tremendous upgrade is needed to comply with ESG standards.

Tenants are also reviewing their carbon footprints. According to a report from ECIU and Oxford Net Zero in 2021, 21% of companies worldwide (representing 14 trillion in sales, 33% of total sales across the top 2,000 public companies) have committed to net zero in some way. As we are getting closer to 2050, more players in the market will re-evaluate their real estate strategies with an eye toward ESG. Most Class B & C properties and some older Class A assets that need large-scale upgrades will face more pressure than those that are newer or recently renovated. Market participants can expect to see accelerated obsoleteness in this sector over the next several years.

Conclusion

We believe the flight-to-quality trend will continue to intensify for several reasons.

With a tight labor market, it’s important to listen to employees and satisfy their needs, from flexible open space to sustainable building features, onsite cafés or outdoor amenities. Employers who are eager to bring their workforce back into the office need to focus on providing the experience employees need. And to do that, being in a quality building to provide those attributes along with cutting edge technology will help a great deal.

With high vacancy rates and record-high concessions, tenants are also able to reduce their footprints and upgrade to smaller but better spaces, leading to outsized demand at the top of the market. Largely due to virtual work, we are predicting muted construction completions in the next decade, which will reduce the supply of prime office spaces.

Further, as companies become more aware of ESG requirements, and with regulations in the U.S. becoming tighter, the performance gap between sustainable buildings and ‘the rest’ will continue to widen. A high-quality building with sustainable features will carry less transition risk going forward, making it more valuable than its peers and easier to attract environmental-conscious tenants and investors. This trend will only accelerate as we get closer to 2050 and more entities (tenants, investors and customers) take a stand on ESG.

The competitive advantage of individual prime buildings will vary by market depending on current and future inventory of top-quality buildings and will certainly be driven by the underlying growth in employment. While we’re seeing a flight to quality, landlords/investors will have to view this trend from a more holistic and long-term lens when deciding its implications for their real estate portfolios.

Contacts

Dennis Schoenmaker, Ph.D.

Global Head of Forecasting and Strategic Insight, Head of Data Centre of Excellence