Article

NOVA’s Data Center Market: 3 Trends to Watch

21 Sep 2021 6 Minute Read

The data revolution has forever changed real estate. Strong data center demand—which predated the pandemic—has continued to skyrocket. The steep development trajectory in Northern Virginia (NOVA) is akin to building out the first two blocks in Manhattan in the 1920’s. There’s nowhere to go but up. Which is why the intense need for space is causing a shift in growth of new locations and designs of data centers of the future.

H1 2021 North American Data Center Trends Report

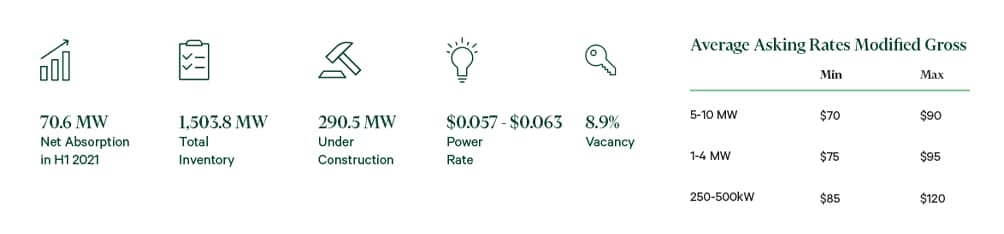

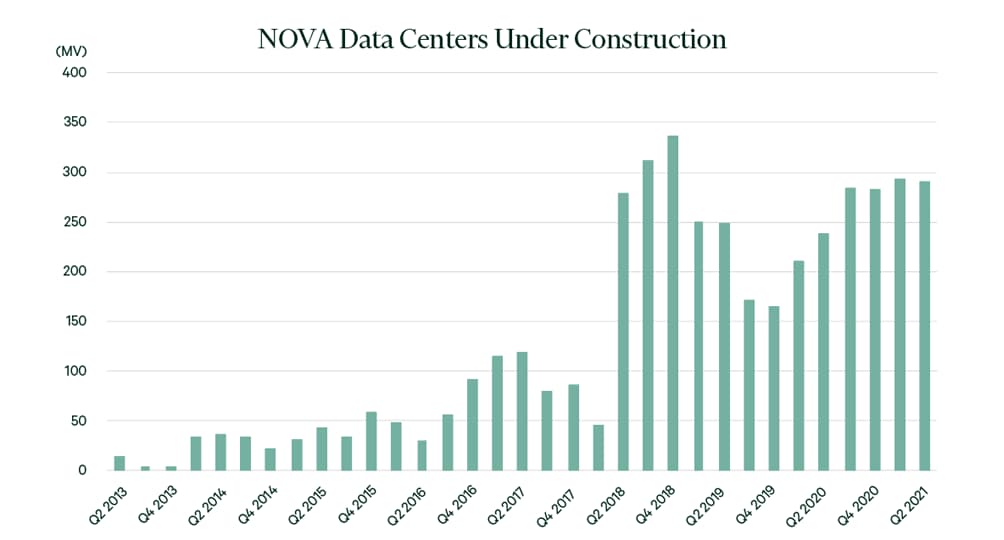

H1 2021 NOVA Data Center Market Statistics

CBRE recently released the H1 2021 North American Data Center Trends Report, here are three takeaways impacting our local market and three trends that will change data centers of the future.

Source: CBRE Data Center Solutions, H1 2021

- NOVA Growth Continues to Dominate

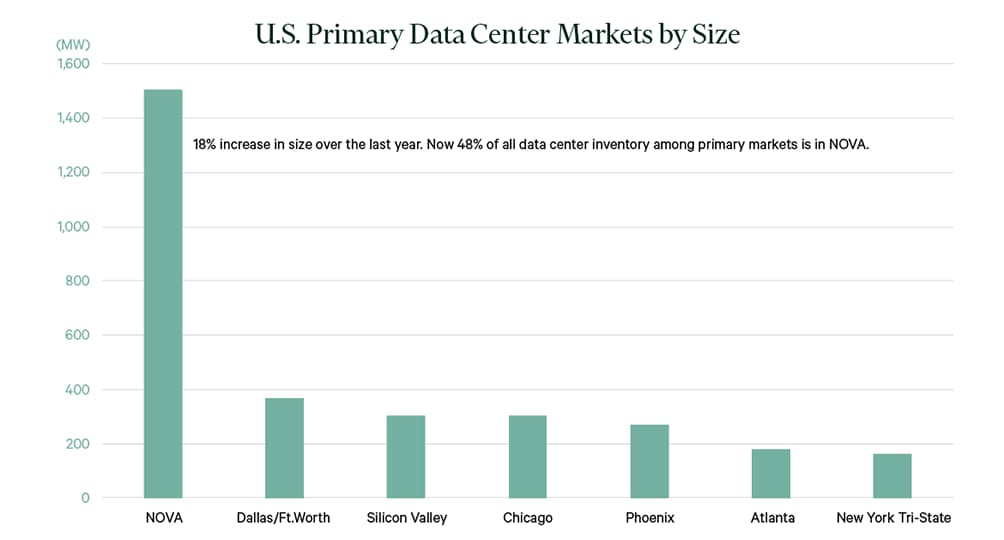

Despite its impressive footprint, NOVA’s dominance in the global Data Center market continued to grow over the last year. As the largest data center market in the world, NOVA is nearly four times the size of the next largest data center market in the United States, Dallas, TX. Absorption and power demand continue to increase at a faster rate than any other market in the world.

Over the past year, the inventory of Northern Virginia data centers surged 18% and now comprise over 48% of all data center inventory in the U.S. primary markets, compared to 47% in H1 2020.

This dynamic growth is a result of three drivers: superior infrastructure, reasonably priced power, and incentives. Its best-in-class network infrastructure is a result of its proximity to, and influence over, the federal government in Washington, D.C. Relatively inexpensive and clean power, compared to many other major metros on the eastern seaboard, also continues to favor NOVA’s data center growth. Finally, attractive policy and tax incentives set up by regional development boards has created a path for some of the world's most well-connected digital infrastructure assets.

Source: CBRE Data Center Solutions, H1 2021

- Vacancy Limited, Despite a Growing Inventory of Space

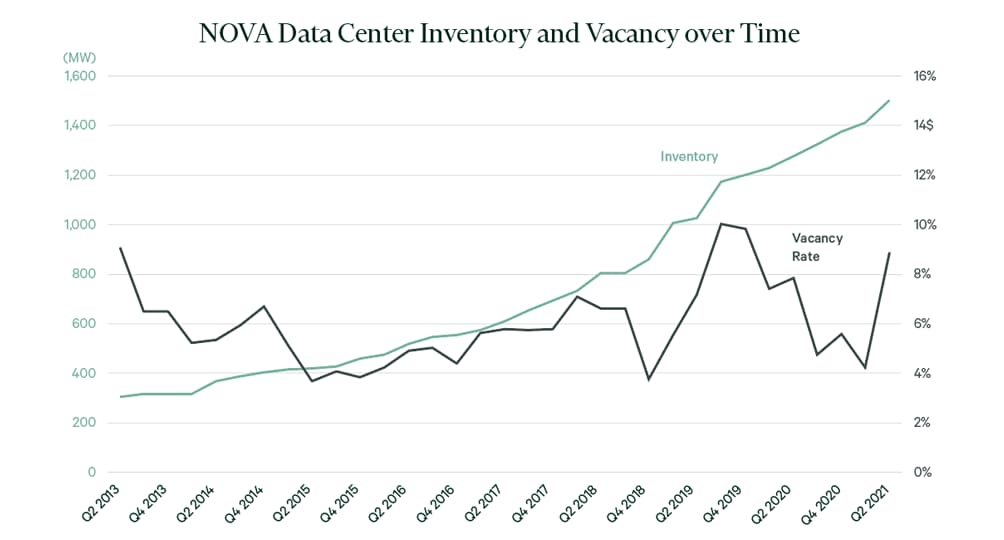

Northern Virginia’s data center dominance will continue to grow in the near-term, but vacancy remains in the single-digits.

In H1 2021, 127.1 MW of new supply was added to NOVA’s market, growing the market’s footprint more than 9%. Over 290 MW of wholesale colocation capacity is under construction, 130 MW of which is anticipated to deliver by the end of 2021 and is fully pre-leased.

NOVA’s data center vacancy rate, though, remained in the single digits in H1 2021, at 8.9%. With persistent, unprecedented demand facing increasing constraints on future development, it is likely that vacancy in the local market will remain relatively tight for users to obtain ideal space.

Source: CBRE Data Center Solutions, H1 2021

- Demand Remains Consistent as Pre-leasing Rates Grow Higher

With over 70 MW of positive net absorption in H1 2021, NOVA retained its position as the preferred location for wholesale colocation demand in the U.S., accounting for nearly half of total net absorption among primary markets and more than 3.5 times above the next primary market’s level.

Financial services firms, global technology companies, and cloud providers were the most active verticals for colocation leasing in H1 2021. The increased need for data center capacity by the U.S. federal government and government contractors in H1 2021 was a direct contributor to the growth of cloud and colocation demand.

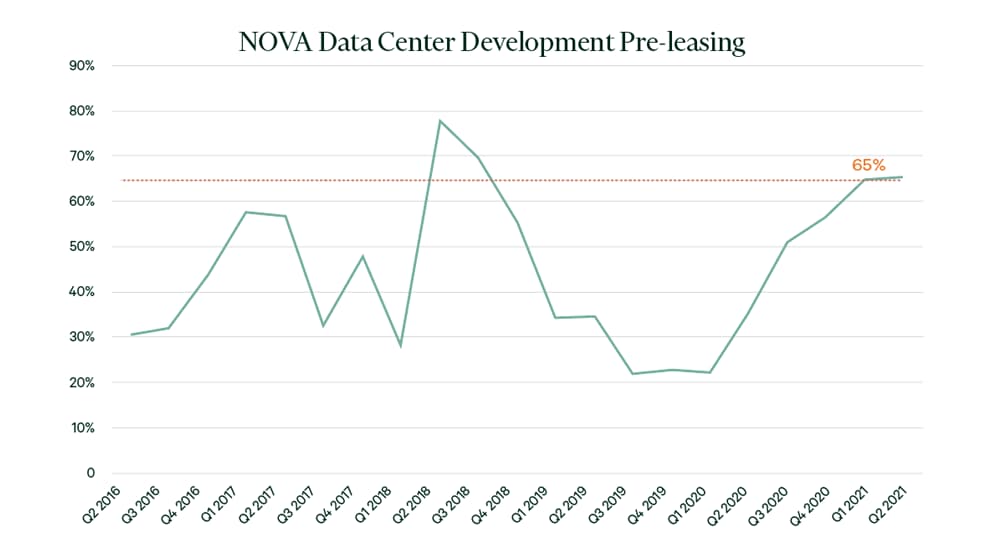

Large preleasing volume, mostly single-tenant hyperscale transactions, will boost absorption in the second half of 2021 and into 2022. The amount of development pre-leased in NOVA grew marginally higher by mid-2021 to 65.4%, demonstrating the depth of demand and health of the local market.

Source: CBRE Data Center Solutions, H1 2021

3 Data Center Trends to Watch

- Unrelenting Network Demand Forced to ‘the Edge’

Massive and unrelenting technological change, driven by new technologies such as 5G, artificial intelligence, blockchain, and growing media content traffic, is fueling ever-growing demand from end users and aggressively pressuring data center providers and operators to accommodate the surge of activity.

As a result, hyperscalers and enterprises continue to focus on edge computing platform readiness to meet the demand for higher-quality services and content. Edge computing occurs when the storage and computing of data is moved to locations closer to the originating source, similar to the Ma Bell sub-stations that connected our telephone exchange systems many years ago. In addition to better application performance and quicker data analysis, this decentralized model enables lower latency, as the 5G standard is less than 10 milliseconds (ms), which will require upgrades for existing fiber (12-20 ms) and cable (15-34 ms) networks. The edge computing emphasis has many data center operators looking to establish new footprints for smaller, higher power density edge data centers to capture the demand.

Hyperscalers and enterprises are executing extensive network evaluations which are focused on:

- Strategically reviewing existing power and fiber capabilities to identify overlays and new needs

- Managing costs as there is limited scale in smaller sites and high competition for key locations

- Building solutions that can limit erratic connectivity and create long-term reliability

- Securing edge and associated networks against risks arising from faster data transport and more locations and access points

Northern Virginia is positioned to capture more large-scale demand as the preeminent data center market in the world in the push towards edge computing.

- Power and Land Constraints Push Data Center Formats Vertically

With more supply under construction in Northern Virginia than all primary markets combined, local data center providers will keep expanding their footprint into 2022 and beyond.

While there is no shortage of future supply to meet the growing demand, power constraints and new development limitations will increasingly have an influence in the nation’s largest data center market. It’s not just Northern Virginia that is facing these constraints; Silicon Valley and Phoenix are also scrutinizing water and power usage much more closely which will impact future development trends and likely cause space to be more expensive. We expect providers to keep adapting their strategies to evolve with environmental requirements in the form of power usage effectiveness efficiencies, water conservation and continue to focus on sourcing clean, affordable power.

The effect of these growing constraints will likely change Northern Virginia’s data center market in two ways. One, the specter of higher asking rates is likely as some inventory bottlenecks occur. Two, data centers will likely become more vertical, growing into multi-story facilities, similar to the vertical growth and higher clear heights of warehouse distribution centers to accommodate surging demand.

- Increased Speed to Market Spec Space

Despite increasing land and power constraints, developers are as aggressive as ever in ensuring adequate space is being delivered for users’ needs in Northern Virginia. The amount of data center space under construction by mid-2021 was near record, aside from a brief surge of activity in 2018. With pre-leasing improving and demand steady, developer confidence is bringing more speculative space to market as well driving the speculative acquisition of land to meet future supply needs. The growing emphasis of “speed to market” of space was one reason that market vacancy increased in the first half of 2021.

Source: CBRE Data Center Solutions, H1 2021

As one of the world’s largest data center real estate practices, CBRE has solved for these future challenges. Contact an expert to discuss solutions.