Dallas, TX

CBRE Report: Core Data Center Markets Across the Globe Race to Increase Supply as Competition Heats Up

Widespread adoption of artificial intelligence accelerated the sector’s growth, leading to record-high leasing activity despite persistent power constraints

June 24, 2025

Media Contact

Sr Corp Communications Manager

Demand from hyperscalers and cloud service providers fueled record leasing volume in the first quarter of 2025 amid widespread adoption of artificial intelligence and persistent power constraints, according to CBRE’s Global Data Center Trends report.

Strong demand and limited availability in core markets led hyperscalers to turn to secondary markets, creating new hotspots like Richmond, Va., Santiago, Chile, and Mumbai, India. The global data center vacancy rate declined by 2.1 percentage points from a year earlier to a record low 6.6% in the first quarter.

“Rising demand from AI and hyperscale users is shrinking vacancy and operators with available capacity in key markets are commanding premium rates,” said Pat Lynch, executive managing director for CBRE’s Data Center Solutions. “As supply tightens in core markets, we’re seeing rapid growth and investor interest in emerging markets, which are becoming central to global deployment strategies.”

CBRE’s Global Data Center Trends Report 2025 analyzes key variables in the top four data center markets in each of North America, Europe, Asia-Pacific and Latin America, as well as emerging markets across the globe. Those variables include total inventory, vacancy rates, net absorption, pricing and rental rates, and availability.

North America Claims Most Construction, Lowest Vacancy

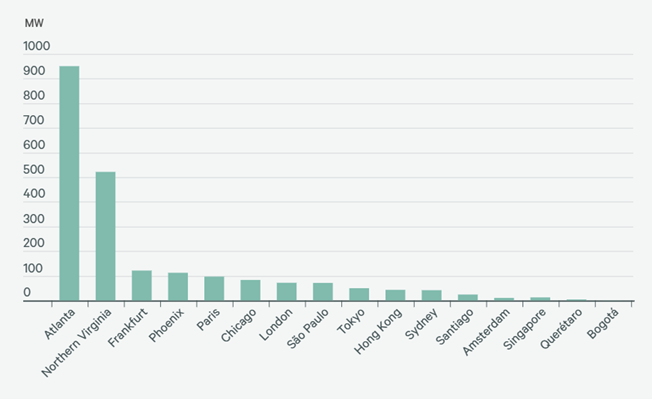

North America had the largest year-over-year inventory increase in Q1 2025 (43%). Northern Virginia remains the largest North American data center market. Atlanta and Phoenix are now the second and third largest data center markets in North America, respectively, surpassing Dallas and Silicon Valley, now fourth and fifth, for the first time.

Latin America had the second largest year-over-year inventory increase (13.7%), followed by Europe (7.2%), and Asia-Pacific (4.3%). Lack of new development, power and land constraints in major Asia-Pacific markets have shifted demand to secondary markets such as Johor, Malaysia; and Melbourne.

North America had the lowest average vacancy (2.3%), followed by 7.4% in Europe, a record low for the region. Latin America vacancy dropped to 8.8% from 9.1% due to its proximity to hyperscalers and large users in the U.S.

In Asia-Pacific, the average vacancy was 14%, with Singapore recording the lowest vacancy in the region at 2% due to strong demand and government environmental and sustainability regulations on new supply.

“Power constraints in legacy markets are forcing hyperscalers to seek new frontiers for development, spreading workloads across multiple smaller locations with faster power availability timelines. While improvements in fiber connectivity have reduced latency concerns and supported this shift, it’s power that ultimately determines where infrastructure can scale,” said Gordon Dolven, Director of CBRE Americas Data Center Research.

Record Leasing Activity, Higher Rents

North America led all regions with 1,668.5 megawatts (MW) of net absorption between Q1 2024 and Q1 2025, double the year-ago figure due to hyperscale expansion and new power availability across key markets. Europe followed with 300.4 MW in net absorption, the second highest in the region’s history.

Latin American leasing activity increased to 99.9 MW in Q1, up from 73.3 MW a year earlier. However, energy restrictions limited net absorption in Querétaro, Mexico and Bogotá to less than 5 MW. Tokyo led Asia-Pacific in net absorption (49.8 MW), but Sydney, Osaka, Melbourne and Johor are well positioned to capitalize on AI-related demand due to available land and scalable power.

Rental rates climbed in North America and Europe due to constrained supply and high construction costs. However, Latin America saw declines in Santiago and São Paulo due to increased availability. Other markets such as Querétaro registered increases due to power constraints. Pricing in Asia-Pacific remained relatively stable.

The report also looks at emerging markets that have attracted large users because of their power availability, proximity to major fiber or cable networks, and new construction. New emerging markets include Des Moines and Richmond (North America); Brussels and Zurich (Europe); Rio de Janeiro and Fortaleza, Brazil (Latin America); and Mumbai and Seoul (Asia-Pacific).

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.