Dallas, TX

Commercial Real Estate Lending Activity Reaches Five Year High: CBRE

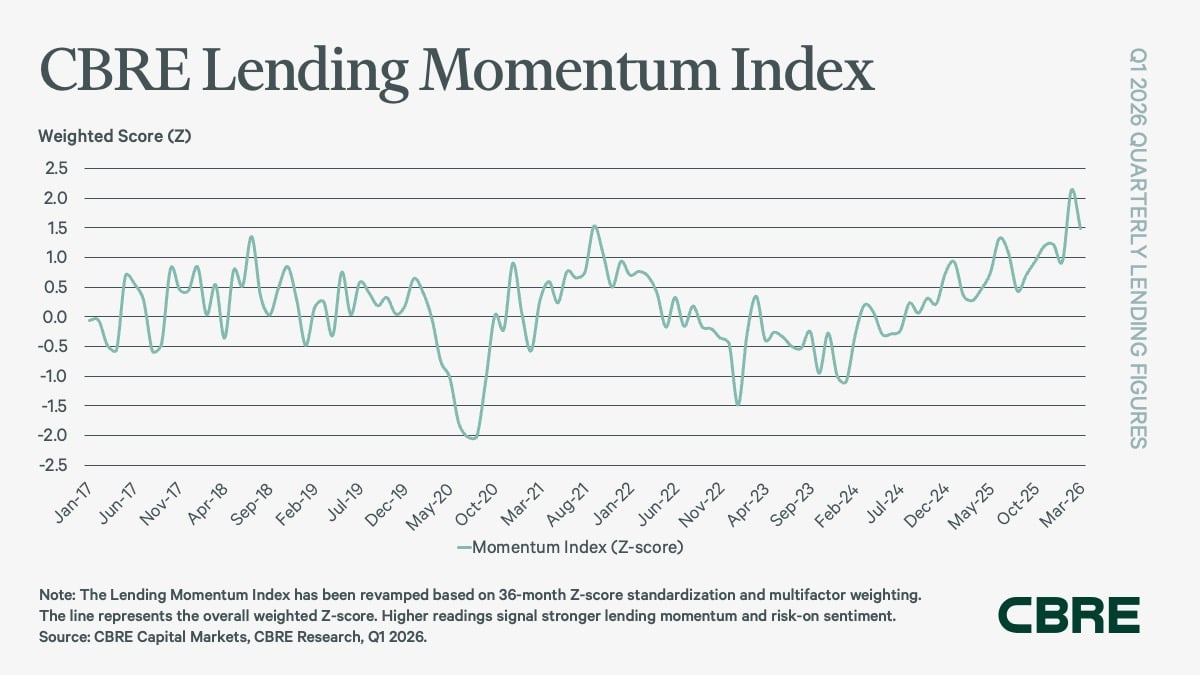

‘CBRE Lending Momentum Index’ Increases to 1.5 in Q1 2026 Alternative Lenders, Banks Lead Top Non-Agency Deals

May 11, 2026

Media Contact

Senior Director, Corporate Communications, Capital Markets/VAS

Commercial real estate lending activity improved further in the first quarter of 2026, reaching its highest level in five years, supported by increased average loan sizes, more non-agency loans, and relatively stable spreads and improved loan-to-value ratios, according to the CBRE Lending Momentum Index.

The CBRE Lending Momentum Index tracks the pace of CBRE originated commercial loan closings in the U.S. over a 36 month period; higher readings signal stronger lending momentum and improved sentiment. The Index rose to 1.5 at the end of Q1 2026, up from 1.2 in Q4 2025 and 0.3 a year earlier—its highest level since 2021. The average loan size increased by 14% year-over-year in Q1 2026.

Commercial mortgage loan spreads declined by 2 basis points (bps) year over year to an average of 181 bps in Q1 2026, while multifamily loan spreads declined by 13 bps year over year to 136 bps. These figures are based on fixed rate, seven to 10 year loans with 55 to 65% loan to value (LTV) ratios.

“We continue to see a more disciplined, yet increasingly healthy commercial real estate lending environment. Rising acquisition activity is driving meaningful price and value discovery, while fresh equity is helping rebalance lender and securitized portfolios,” said James Millon, President & Co-Head of Capital Markets, U.S. & Canada, for CBRE.

“Recapitalizations, particularly involving larger assets and portfolios, remain active, with well-structured financings often serving as the foundation for new joint ventures. Today, property owners and investors have a broader set of options to create liquidity beyond traditional sales, supporting strong market participation and capital absorption.”

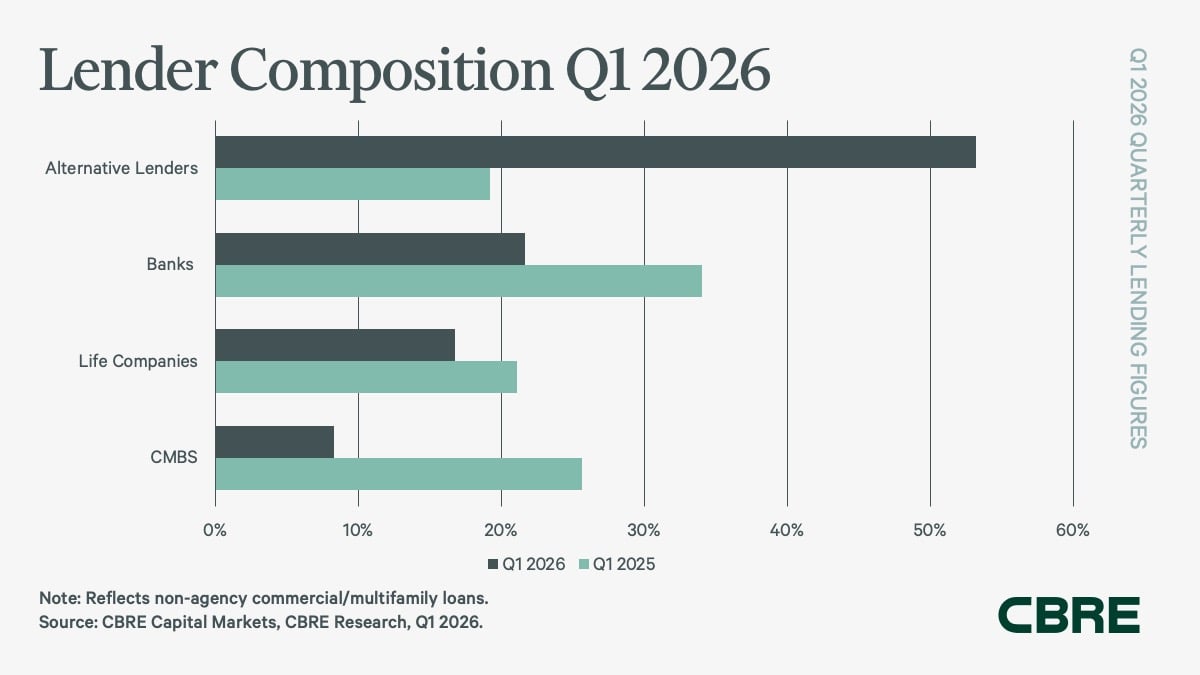

Alternative lenders, including debt funds and mortgage REITs, led CBRE’s non-agency loan closings in Q1 2026, accounting for 53% of total volume, up from 19% a year ago. Debt funds were the primary driver of this increase, with lending volume increasing 280% year-over-year.

Banks held the second-largest share of non-agency loan closings at 22%, down from 34% a year ago, while life companies accounted for 17%, compared with 21% a year ago. CMBS lenders represented the remaining 8% of non-agency loan volume, down from 26% a year ago.

Key underwriting metrics remained stable, with modest easing in borrowing costs, in Q1 2026. Loan constants declined by 10 bps quarter over quarter to 6.7%, while average mortgage interest rates fell by 110 bps quarter-over-quarter to 5.7%. Debt yield also remained within a stable range at 9.5% in Q1 2026, compared with 9.8% in Q4 2025 and 10.3% a year ago.

Average commercial loan to value (LTV) ratios increased to 61.5% in Q1 2026, up from approximately 59% a year earlier, while multifamily LTV ratios rose to 67.2% from 65% a year ago, indicating a modestly less conservative approach by lenders.

Government agency lending for multifamily assets remained strong. Agency origination volume from Fannie Mae and Freddie Mac increased 35% year-over-year to $29.9 billion in Q1 2026. CBRE’s Agency Pricing Index, which tracks average fixed agency mortgage rates for 7-to-10-year permanent loans, fell by 42 bps year-over-year to 5.4%.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services. The company has more than 155,000 employees serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, critical infrastructure); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.