Dallas, TX

Commercial Real Estate Lending Market Fundamentals Improve in Q2 2024

Alternative Lenders Are Largest Contributors to Non-Agency Loan Closings

August 19, 2024

Media Contact

Senior Director, Corporate Communications, Capital Markets/VAS

The commercial real estate lending market continues to show signs of improvement, driven by acquisition financing in the industrial and multifamily sectors, reduced credit spreads with expectations of interest rate adjustments, and the growing demand for large-scale data center construction loans due to advancements in AI technology, according to the latest research from CBRE.

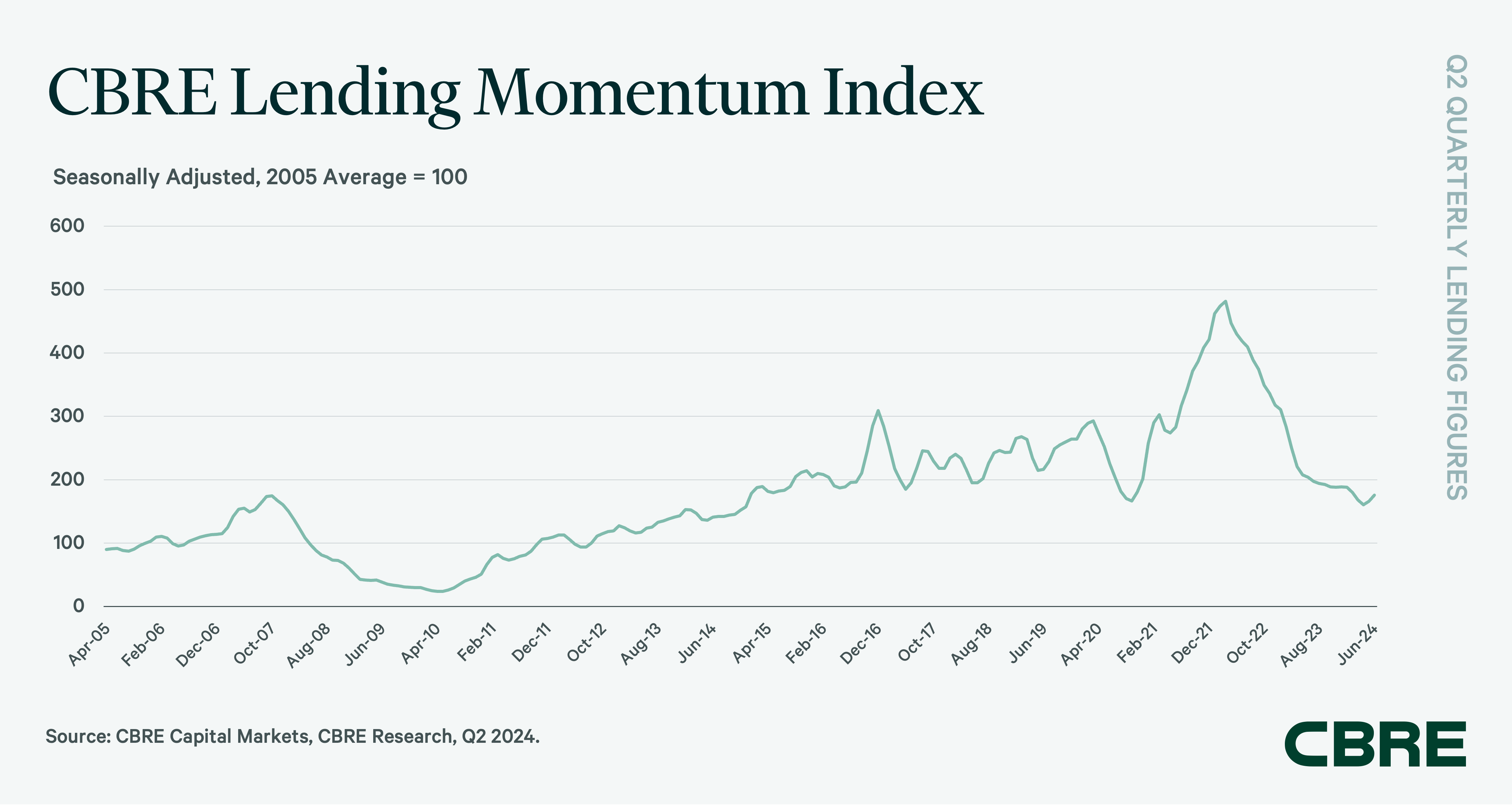

The CBRE Lending Momentum Index, which tracks the pace of CBRE-originated commercial loan closings in the U.S., rose by 4.3% from Q1 2024 after falling for the five previous quarters. The index saw a decline of 14% compared with the strong loan volume of Q2 2023 as high rates continued to weigh on lending activity. The index closed Q1 2024 at a value of 175.

The spread on closed commercial mortgage loans averaged 183 bps in Q2 2024, down by 29 basis points (bps) from Q1 2024 and 44 bps year-over-year. Industrial assets accounted for the largest share of Q2 2024 loans, which typically carry lower spreads compared to other commercial properties.

“Commercial real estate origination volumes have been steadily increasing, driven by factors such as 2021 floating rate maturities, heightened acquisition financing activity concentrated in the industrial and multifamily sectors, stabile spreads, and generally strong availability of credit,” said James Millon, U.S. President of Debt & Structured Finance for CBRE.

“Looking forward, we expect continued strength in origination activity driven by large institutional financings and greater GSE participation, underpinned by declining treasuries and base rates. Anticipated interest rate cuts are expected to further drive deal-making, leading to reduced borrowing costs, improved credit availability, and higher asset valuations. The explosion of data center development to meet the growing demand for AI is also contributing to the quantum of debt capital and further bolstering origination activity.”

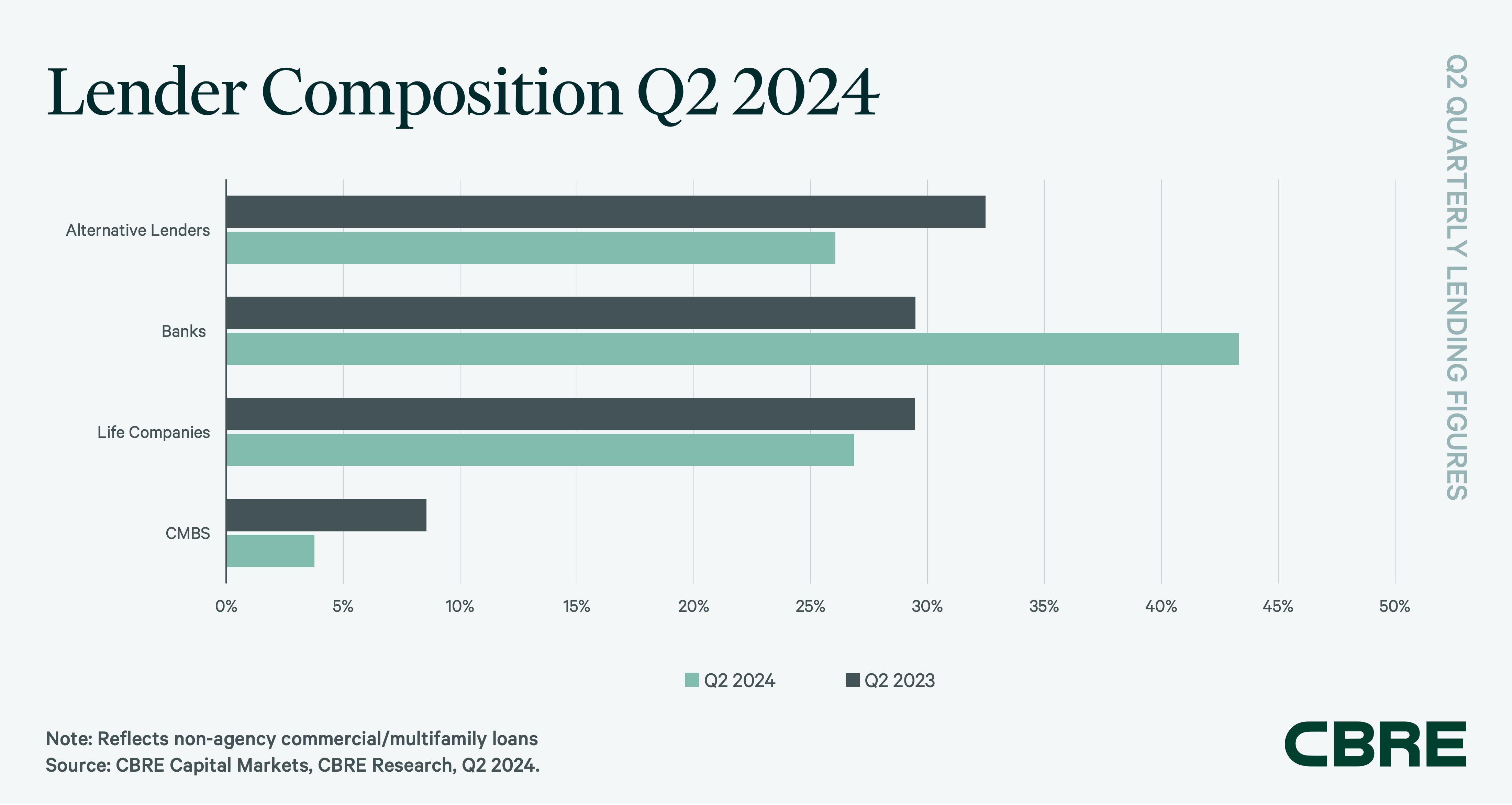

Alternative lenders, such as debt funds and mortgage REITs, remained the leading contributors to CBRE's non-agency loan closings, accounting for 33% of the total in Q2 2024 and up from their 26% share a year earlier. Among alternative lenders, debt funds increased their origination volume by 71% year-over-year.

Banks were the next most active lending group with 30% of non-agency loan closings in Q2 2024, down from their 43% share a year earlier. Banks are expected to remain cautious due to the increase in loan extensions, limited liquidity and the potential for increased regulatory pressures.

Life insurance companies contributed 30% of origination volume in Q2 2024, up from 27% a year earlier. While still active, life insurance companies continue to adopt a more selective approach this year.

CMBS conduits represented the remaining 8.6% of origination volume in Q2 2024, up from 3.8% a year earlier, but slightly down from 8.8% in Q1 2024.

In Q2 2024, there were slight changes to underwriting criteria. Average underwritten cap rates and debt yields fell to 5.9% and 9.7%, respectively on lower LTV ratios. The average LTV ratio decreased by 65 bps to 61.6% but was up by 1 percentage point from a year ago.

Government agency lending on multifamily assets increased by $1 billion in Q2 2024 to $20 billion. CBRE’s Agency Pricing Index, reflecting average fixed agency mortgage rates on 7–10-year permanent loans, rose by 26 bps quarter-over-quarter and by 57 bps year-over-year to 6%.