Dallas, TX

Commercial Real Estate Lending Momentum Reaches Highest Level Since 2018

‘CBRE Lending Momentum Index’ Increases 112% in Q3 2025 Alternative Lenders, Banks Top Non-Agency Deals

November 10, 2025

Media Contact

Senior Director, Corporate Communications, Capital Markets/VAS

Commercial real estate lending showed strong improvement in the third quarter of 2025, as stabilizing borrowing costs and tighter credit spreads helped bridge pricing gaps between buyers and sellers and boosted deal activity across asset classes, according to the latest research from CBRE.

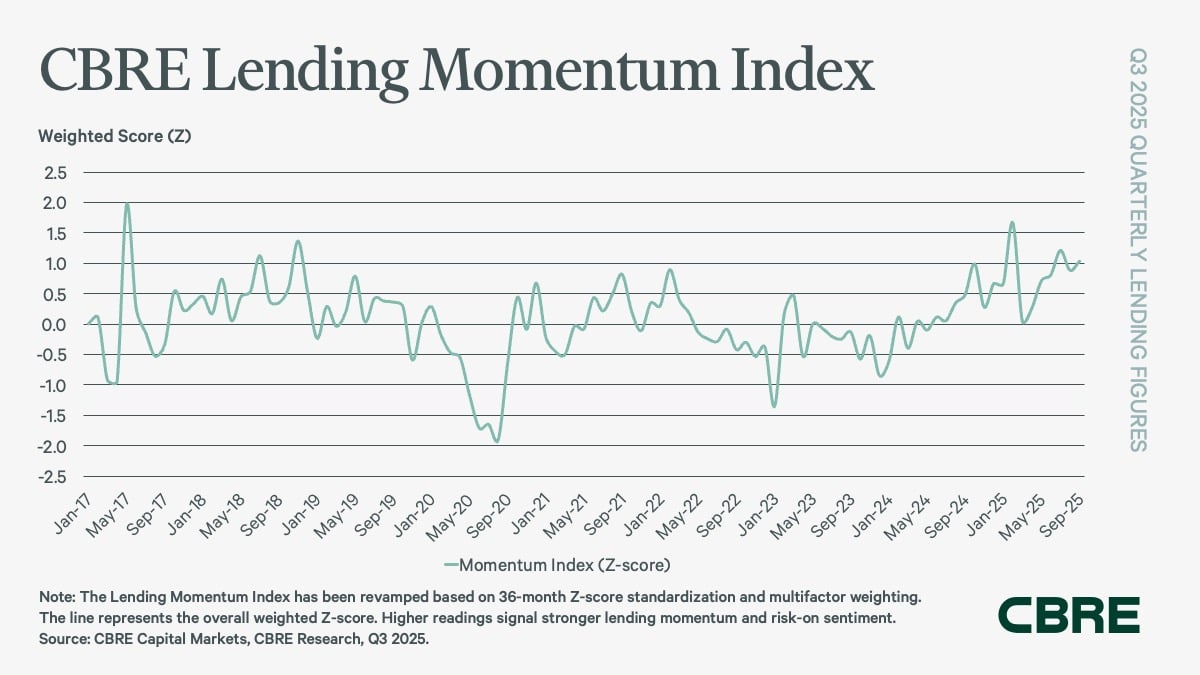

The CBRE Lending Momentum Index, which tracks the pace of CBRE-originated commercial loan closings in the U.S., increased 112% year-over-year (up 0.55 points) to 1.04 at the end of Q3 2025, reaching levels last seen in 2018. This growth was driven by a 36% year-over-year increase in permanent loan financing, with particularly strong activity in September.

Commercial mortgage loan spreads widened slightly to an average of 197 basis points (bps) in Q3 2025, up by 4 bps quarter-over-quarter and 14 bps year-over-year. In contrast, multifamily loan spreads tightened by 27 bps year-over-year to 141 bps, reflecting increasingly competitive agency loan pricing. These figures are based on fixed-rate, seven-to-10-year loans with 55-to-65% loan-to-value (LTV) ratios.

“We’re seeing a broad recovery in investment sales across all major asset classes, led by high-conviction sectors like multifamily and industrial. Core capital is beginning to return selectively, shaping equity pricing in key markets and building momentum. Stabilizing financing costs, with the five-year Treasury in the 3.5% to 3.6% range, combined with tightening credit spreads and a shift toward floating-rate financings, are narrowing the bid-ask gap. This dynamic is fueling transactions and unlocking new opportunities,” said James Millon, President & Co-Head of Capital Markets, U.S. & Canada, for CBRE.

“Office financing and sales volumes have surged by multiples, not percentages, driven by strong fundamentals in the best assets in high-growth markets. Construction activity also remains robust, especially for build-to-core multifamily and large-scale data centers. We expect current momentum to carry into 2026.”

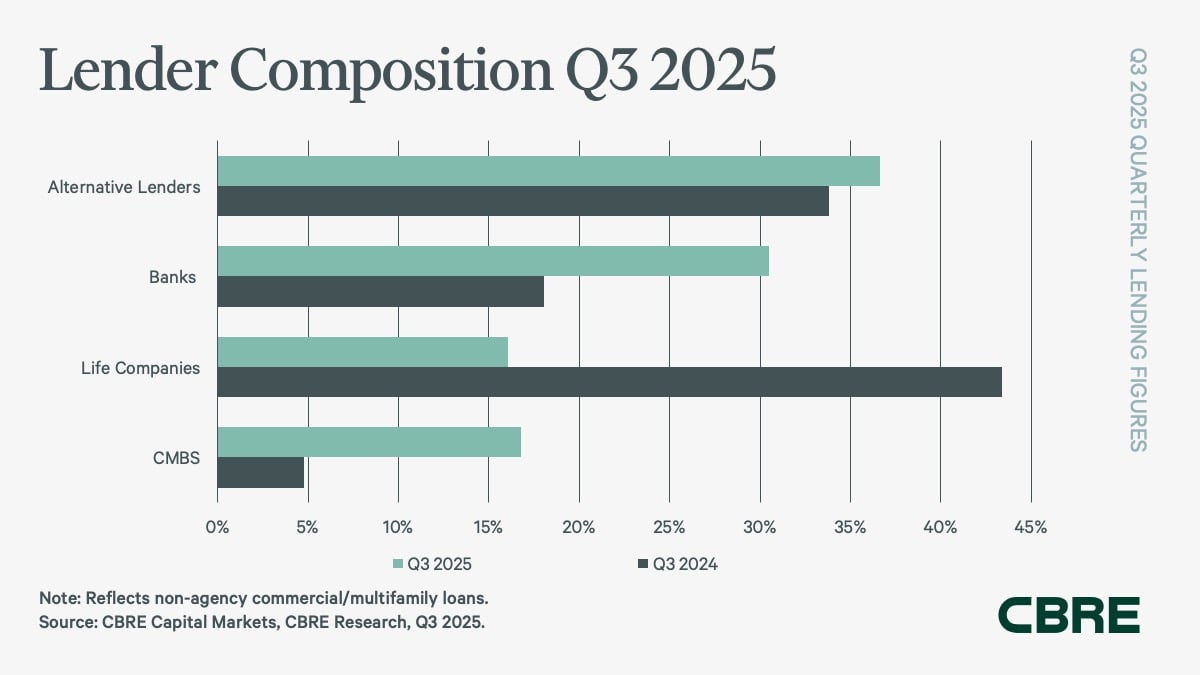

Alternative lenders, including debt funds and mortgage REITs, led CBRE's non-agency loan closings in Q3 2025, capturing a 37% share, up from 34% in the same period last year. Debt funds were the primary driver, with lending volumes up 68% year-over-year.

Banks held the second-largest share of non-agency loan closings at 31%, a sharp increase from 18% last year, as origination volumes surged 167%, marking a strong reentry into the market. CMBS lenders also saw substantial gains, with their share rising to 17% from 5% a year ago, driven by a fivefold increase in lending volume.

Life companies accounted for 16% share of non-agency loan volume in Q3 2025, down from 43% a year ago.

Key metrics point to a more favorable lending environment. Loan constants decreased by 20 bps quarter-over-quarter, while mortgage interest rates fell by 28 basis points. The average LTV ratio rose slightly to 63.8%, up from 63.3% in Q2 2025, indicating a modestly less conservative approach by lenders.

Government agency lending for multifamily assets reached $44.3 billion in Q3 2025, reflecting a 53% quarter-over-quarter and a 57% rise year-over-year. CBRE’s Agency Pricing Index, which tracks average fixed agency mortgage rates for 7–10-year permanent loans, fell to 5.6%, down 13 bps from the previous quarter and by 27 bps from the same period last year.

Notes to Editors

The CBRE Lending Momentum Index tracks commercial real estate loans that are either originated or brokered by CBRE. It uses a 36-month Z-score standardization to show how current lending activity deviates from its 36-month historical average. The Index incorporates multi-factor weighting, taking into account variables such as loan size, type, and borrower profile, to provide a more comprehensive view of lending trends. Higher readings for the Index indicate stronger lending momentum and a greater appetite for risk in the commercial real estate market.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.