Dallas, TX.

Rent Growth for Suburban Retail Outpacing High Street Rent Growth in Many Markets

May 8, 2025

Media Contact

Corporate Communications

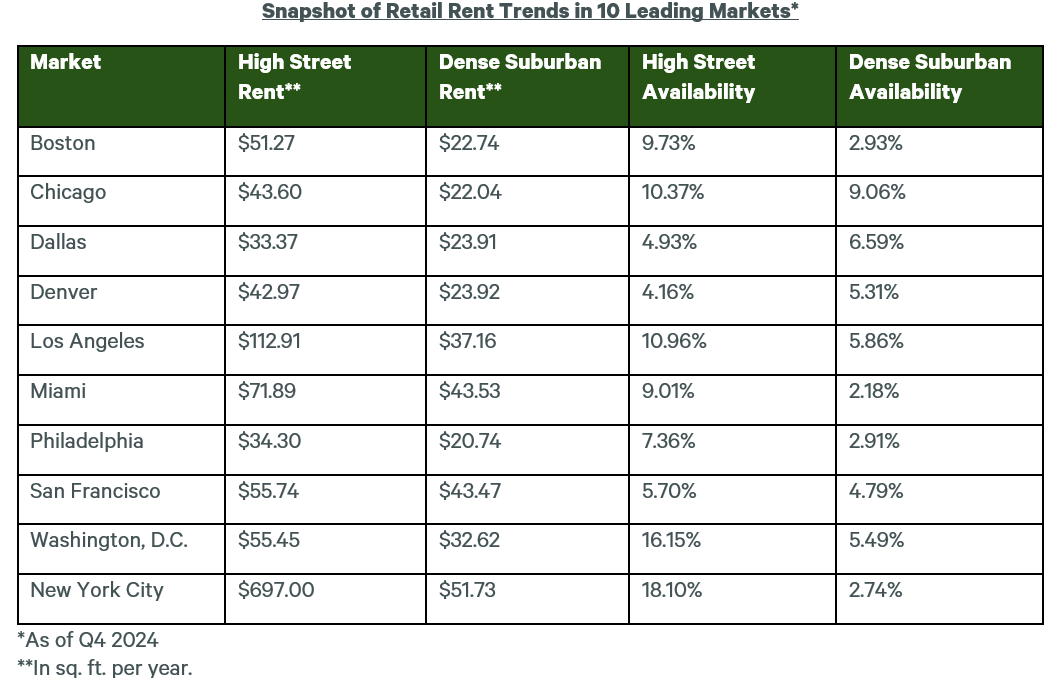

Retail rents in dense suburbs are growing faster than downtown rents in many cities, though downtown, high-street rents still command hefty premiums, according to a new report from CBRE.

CBRE’s analysis in its 2025 Retail Rent Dynamics report found that suburban retail rent growth has outpaced downtown rent growth in six of 10 major cities. Among the cities with the widest gaps in rent growth over the past five years are New York (2.1% growth in dense suburbs vs. 0.7% growth in downtown high streets), Boston (2.1% vs. 1.4%) and Denver (2% vs. 1.5%).

“In many cases, retailers are expanding into dense suburbs, especially live-work-play districts with large populations, strong employment and complementary residential development,” said Amanda Ortiz, CBRE Director of Americas Industrial and Retail Research. “That’s partly because people on hybrid work schedules are spending more time close to their homes in the suburbs than they did previously. Meanwhile, rents still are growing in most downtown, high-street districts, just at a slower pace and off a higher base.”

In the 10 major cities, the rent premium for high streets over suburban markets ranges from 12 times as large in New York City to 200% in Los Angeles to 28% in San Francisco in last year’s fourth quarter. Even so, high streets still are registering rent gains, including Miami with a five-year gain of 3.9%, Dallas with 3% and Los Angeles with 2.8%.

The challenge for high streets is hefty availability, given that hybrid work schedules depleted foot traffic in many downtowns, which in turn made replacing departed retailers more challenging. In eight of the 10 markets, high street availability exceeded suburban availability in the fourth quarter. The largest differences are in New York City, where high street availability is 15.36 percentage points higher than suburban availability; and Washington, D.C., with a 10.66 percentage-point gap.

The opposite holds in Dallas and Denver, where suburban availability exceeds high-street availability. In Dallas, that’s partly due to robust construction of suburban retail centers to keep pace with population growth. In Denver, demand for leasing in suburban centers slowed.

Live-work-play districts that combine retail with residential and office are outperforming the broader market. Rents in LWP districts in the 10 markets range from $27.80 per sq. ft. per year in San Francisco to $91.40 in New York City. The national average across all retail formats was $24.54 in the fourth quarter.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.