Intelligent Investment

Commercial Loan Losses to Create Short-Term Pain, Long-Term Opportunities

July 13, 2023 5 Minute Read

Executive Summary

- As higher interest rates, economic uncertainty and structural changes in demand lower property values, particularly for office assets, we expect distress to emerge in commercial real estate.

- While challenging in the near term, emerging distress will present some unique opportunities for commercial real estate investors.

- Office assets account for $748 billion or 17% of the $4.5 trillion in outstanding commercial real estate loans.

- CBRE estimates that commercial real estate loan losses for all lenders could total up to $125 billion over the next several years, with office loans accounting for approximately $53 billion.

- For banks alone, total CRE loan losses could be $60 billion, including $26 billion in office loan losses.

- While especially troubling for small community banks, these potential loan defaults are not expected to be enough to destabilize the U.S. financial system.

Fears of Distress

Reports have suggested that the nearly $2 trillion in commercial real estate (CRE) loans maturing over the next three years could cause more bank failures and destabilize the financial system. CBRE estimates that bank loan losses could reach nearly $60 billion, with $26 billion attributed to office loans. This will create challenges for some banks but won’t be enough to destabilize the financial system since office loans held by banks make up only 1.5% of assets in the banking system.

Root Causes

Rising interest rates and a worsening economic outlook have weakened commercial real estate fundamentals, with the office sector hit particularly hard. The pandemic-induced shift to remote working arrangements has lowered office demand, causing vacancy rates to rise and rent growth to decline. As a result, investors have generally become wary of office acquisitions.

However, CBRE has found that a relatively small subset of downtown buildings (generally no more than 300,000 sq. ft. in size, built between 1980 and 2010, located in higher crime areas and with fewer nearby amenities) account for a disproportionate share of the deterioration in office fundamentals.

Lender Exposure

Office loans account for approximately $748 billion1 of the $4.5 trillion in outstanding CRE loans held by life insurers, government agencies, credit companies, asset-backed security vehicles, traditional banks and other lenders.

Banks account for about 45% of outstanding office debt, with the remainder provided by other lenders, including commercial mortgage backed securities, life insurers and credit companies. We expect that all lenders will incur office loan losses.

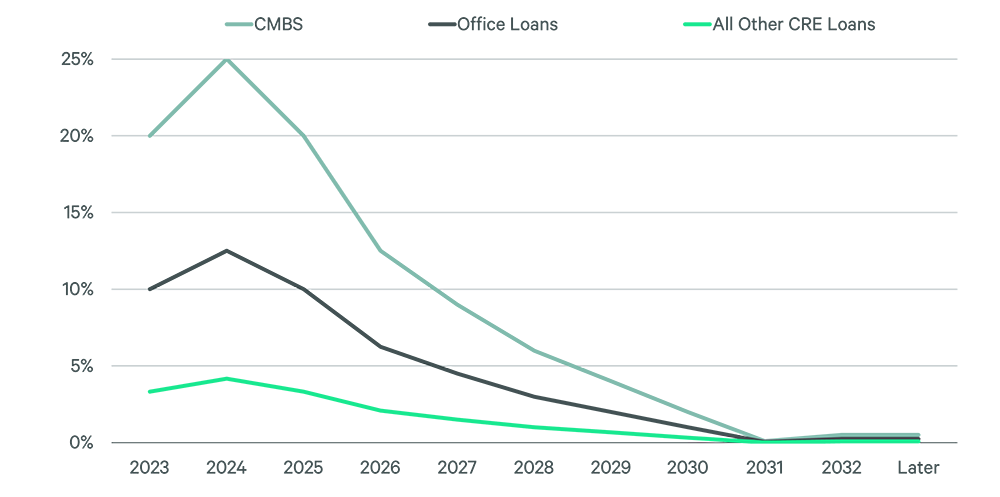

Figure 1: CRE Loan Maturities by Year

Note: % values represent office sector share of total annual CRE loan maturities.

Source: Mortgage Bankers Association, January 2023.

Focus on Banks

In the wake of notable bank failures earlier this year, there are concerns that banks’ exposure to CRE loans could cause financial sector instability. Bank exposure to CRE loans totals $1.7 trillion, of which $340 billion is for office assets.2 Almost half of those office loans will mature before next year.

Our analysis suggests lenders could face CRE loan losses across all property types of up to $125 billion. Almost half of these losses would be concentrated in the banking sector, with office loans accounting for approximately $26 billion. Losses will be greatest in 2023 and 2024, then ease as broader market and financial conditions improve.

Figure 2: Annual CRE Loan Maturities for Banks

Note: % values represent office sector share of total annual CRE loan maturities.

Source: Mortgage Bankers Association, January 2023.

Financial Crisis Unlikely

To project potential loan losses, we looked at how CMBS and bank loans performed during the Global Financial Crisis (GFC). CMBS had a loan default rate of 9%, compared with 4.5% for banks. Bank loan default rates were moderated during the GFC by accommodative regulatory policy3 and low interest rates. However, interest rates are much higher today as the Fed combats excessive inflation.

We have calculated likely loan loss rates for outstanding commercial real estate loans, taking into account conditions that are notably different than during the GFC. Our analysis takes into account higher interest rates and stronger fundamentals in every CRE sector (except office). We also account for the potential of a moderate recession beginning in Q4 2023 that is not expected to be as severe as the one that occurred during the GFC.

Our analysis suggests lenders could face CRE loan losses across all property types of up to $125 billion. Almost half of these losses would be concentrated in the banking sector, with office loans accounting for approximately $26 billion. Losses will be greatest in 2023 and 2024 then ease as broader market and financial conditions improve.

Figure 3: Projected Loan Loss Rates

Source: CBRE Research, July 2023.

Figure 4: Annual Office & Total CRE Loan Losses ($ Billions)

Note: All lenders include asset-backed securities, life insurers, government agencies, credit companies and banks.

Source: CBRE Research, July 2023.

Figure 5: Loan Losses as a % of Maturing Loans

Source: Mortgage Bankers Association, CBRE Research, July 2023.

Office loan losses, while challenging for banks, are unlikely to destabilize the broader financial system since office loans held by banks make up only 1.5% of assets in the banking system. The banking sector’s projected losses on all CRE loans account for only 3% of banks’ equity capital and disclosed reserves. We do not see this as comparable to the GFC when banking system stress was largely driven by residential real estate, which in 2007 made up 20%4 of bank assets compared with commercial real estate accounting for 10%5 of bank assets today. Nevertheless, CRE loan losses could be particularly problematic for some smaller community banks, potentially leading to more bank failures. In the short-term, we expect loan losses will lead to stricter lending standards and lessen credit availability for commercial real estate assets.

Figure 6: Bank Loan Losses as a % of Tier 1 Capital

Note: Tier 1 capital includes banks’ equity capital and disclosed reserves.

Source: FDIC, CBRE Research, July 2023.

Other Impacts & Opportunities

We expect that high interest rates and less credit availability will continue to weigh on commercial real estate investment activity. Additionally, many assets will experience a debt funding gap as investors are forced to refinance at lower loan-to-value ratios that necessitate funding through mezzanine debt or even equity investment. CBRE Econometric Advisors forecasts that office owners will face a financing gap of nearly $73 billion between 2023 and 2025.

However, this constrained lending environment will present some investment opportunities across all property types, particularly from motivated sellers unable to refinance their maturing loans. Other potential opportunities for investors include properties valued at between $30 million and $50 million—as outlined in CBRE’s recent Investment Approaches Viewpoint—that are too large for smaller banks to finance and too small for many debt funds. Notably, we have even observed this in assets with strong rent growth prospects in healthy markets.

1 Mortgage Bankers Association, January 2023.

2 Mortgage Bankers Association, January 2023.

3 Banks did not have to take charge-offs on commercial real estate loans so long as borrowers made minimum debt service payments.

4 Federal Reserve, July 2023.

5 Federal Reserve, July 2023.

Research Contacts

Insights in Your Inbox

Stay up to date on relevant trends and the latest research.