Intelligent Investment

Economic Watch: Fed Makes First Rate Cut of 2025

September 17, 2025 4 Minute Read

Executive Summary

- As expected, the Federal Reserve lowered the federal funds rate by 25 basis points (bps) today to a range of 4.00% to 4.25%.

- CBRE forecasts that lower borrowing costs will boost commercial real estate investment volume by approximately 15% this year, up from an earlier projection of 10%.

- Income-focused strategies will become more important amid limited cap rate compression.

- Leasing demand may be impacted due to a weaker labor market. However, continued flight-to-quality and gateway market recovery, especially in the office sector, should drive moderate leasing growth for the rest of this year and into 2026.

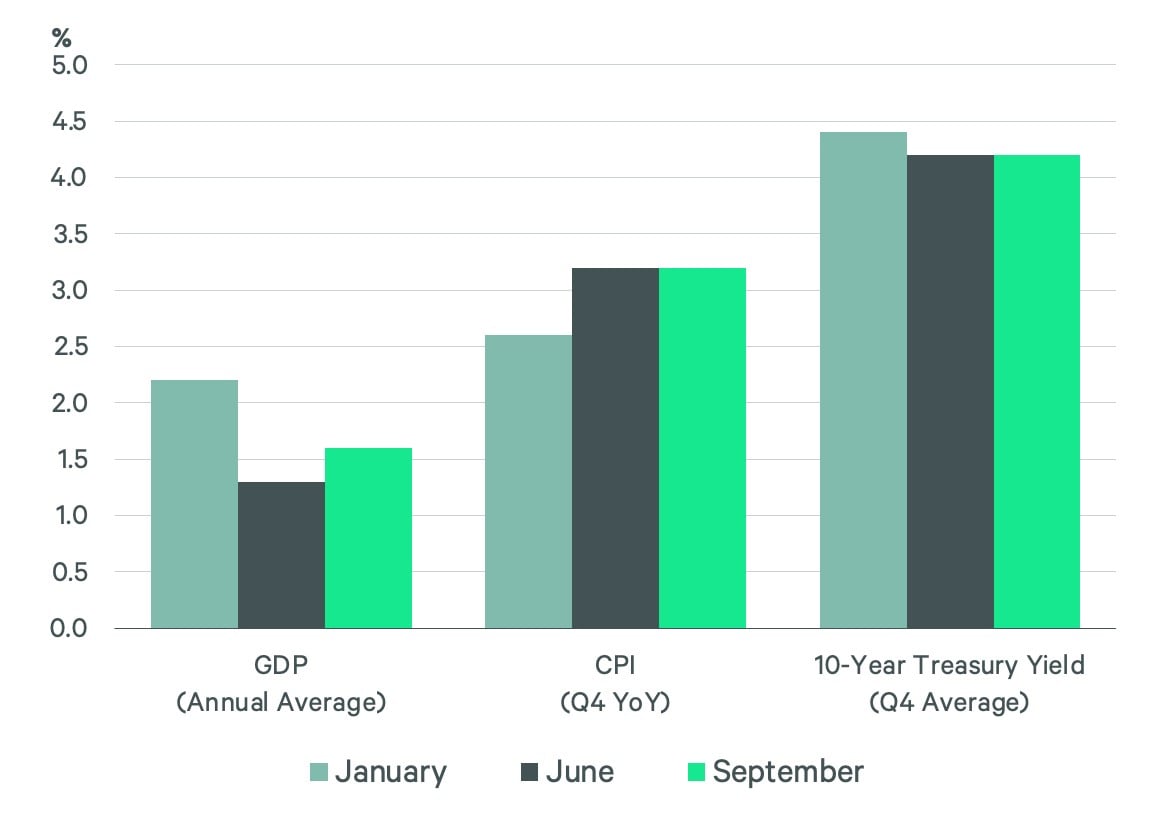

As expected, the Federal Reserve lowered the federal funds rate by 25 bps today to a range of 4.00% to 4.25%. We expect two more rate cuts this year, reducing the federal funds rate to between 3.50% and 3.75%.

We expect that the 10-year Treasury yield will remain around 4% through the end of the year, reflecting investor concerns about the federal budget deficit. CBRE projects a slight deceleration in economic growth during the second half of 2025, driven by a cooling labor market and tariff impacts that are expected to boost inflation to 3.3% for the year.

Figure 1: Change in CBRE Expectations

Impact on Commercial Real Estate

Today's interest rate cut will support capital markets activity by bolstering investor sentiment and reducing borrowing costs. We now expect commercial real estate investment volume to increase by approximately 15% for the year, up from our earlier projection of 10%.

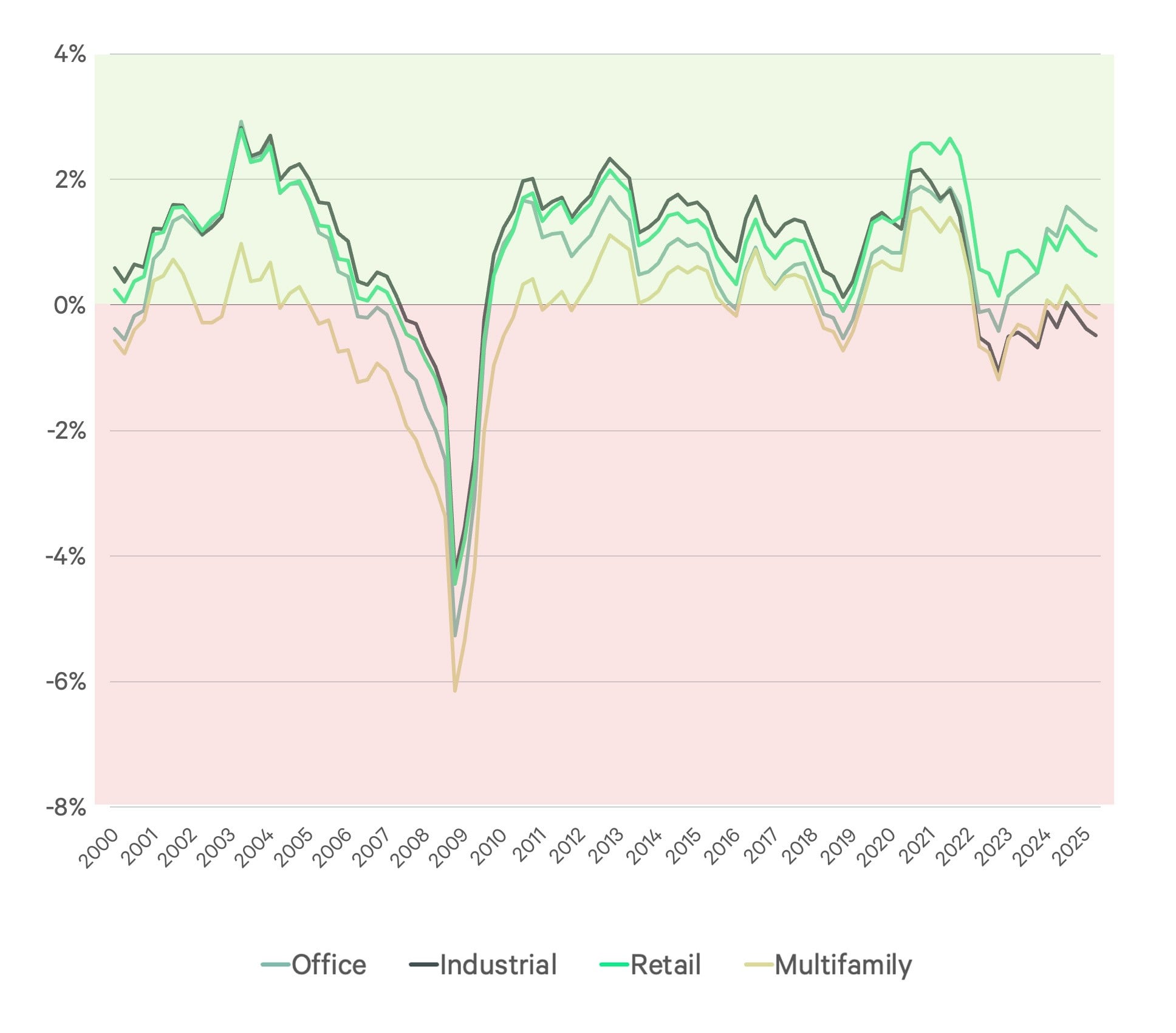

Improved liquidity will benefit most sectors and we expect to see continued refinancing opportunities. However, challenges persist, particularly for distressed office assets. The U.S. aggregated all-sector cap rate stood at 5.95% in Q2 2025 from 6% a year earlier. CBRE forecasts limited cap rate compression this cycle, as long-term interest rates are expected to remain elevated. This points toward a more income-focused investment cycle that underscores the importance of strategic investment decisions and careful asset selection.

Despite today’s rate cut, a weakening labor market may moderate occupier leasing demand. However, flight-to-quality and gateway market recovery—especially in the office sector—are expected to persist, alongside robust lease renewal activity. The 2025 Americas Office Occupier Sentiment Survey highlights strong expansion plans by professional services and small office-based businesses, while third-party logistics occupiers will pace demand for industrial space. CBRE anticipates a moderate increase in leasing activity through 2025 and into 2026.

Figure 2: U.S. Cap Rates Less All-In Cost of Capital

Contacts

Dennis Schoenmaker, Ph.D.

Global Head of Forecasting and Strategic Insight, Head of Data Centre of Excellence