Intelligent Investment

North America Data Center Trends H1 2025: AI & Hyperscaler Demand Lead to Record-Low Vacancy

August 19, 2025 3 Minute Read

This brief provides highlights of CBRE’s upcoming North America Data Center Trends H1 2025 report, due for release in early September. The full report will provide a more detailed analysis of supply, pricing and other dynamics that are creating the tightest market conditions in more than a decade.

North America’s data center vacancy rate is at an all-time low 1.6%, as hyperscale and AI occupiers race to secure power and capacity years ahead of delivery, according to CBRE’s upcoming North America Data Center Trends H1 2025 report. Demand is outpacing supply in nearly every major market, driving elevated lease rates and prompting rapid market expansion. Competition for available power and infrastructure remains intense, with large-scale occupiers moving quickly to lock in capacity for future growth.

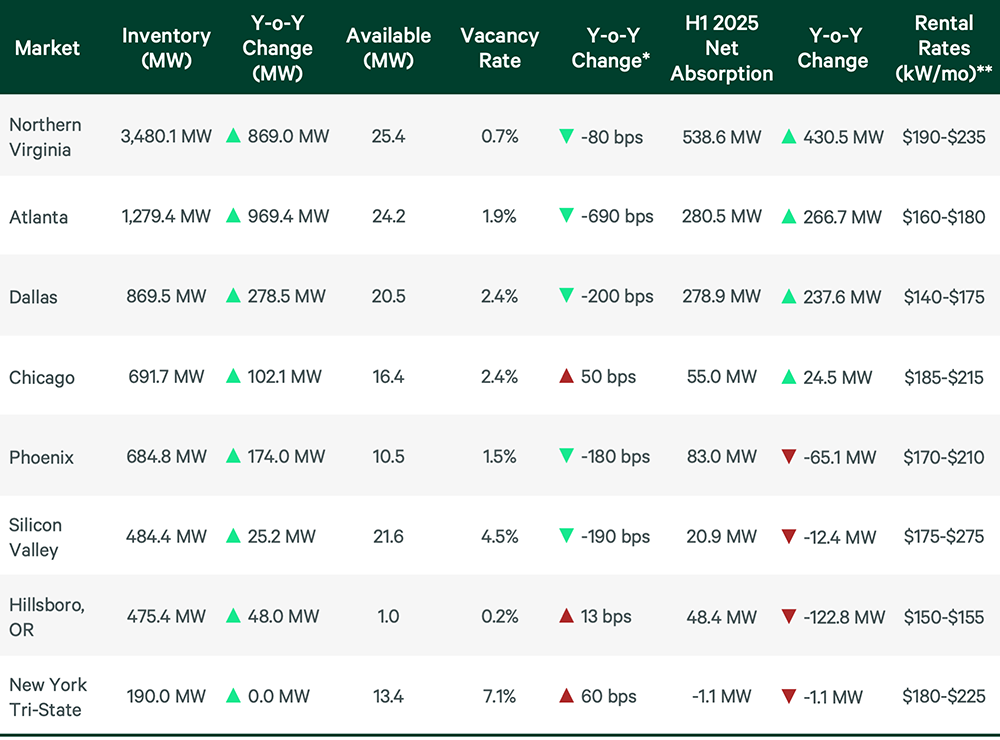

Figure 1: H1 2025 Wholesale Primary Market Fundamentals

*Vacancy Y-o-Y changes are calculated by comparing the difference between H1 2025 and H1 2024.

**Rental rates are quoted asking rates for 250+ kW at N+1/Tier III requirements.

Source: CBRE Research, CBRE Data Center Solutions, H1 2025.

Key findings of the report include:

- Single and continuous requirements for 10 megawatts (MW) or more recorded the sharpest increases in lease rates, driven by hyperscale demand, limited power availability and elevated construction costs.

- Atlanta posted the largest year-over-year inventory growth in H1 2025, adding 969.4 MW.

- The record-low vacancy rate of 1.6% highlights unrelenting demand from hyperscale and AI occupiers.

- Northern Virginia maintained its position as the top-performing market, with 538.6 MW of net absorption and an 80% surge in under-construction capacity.

- 74.3% of capacity under construction is preleased, primarily to cloud and AI providers securing future infrastructure.

- Power availability and delivery timelines continue to shape site selection, leasing and pricing strategies across major U.S. markets.

Figure 2: H1 2025 Wholesale Secondary Market Fundamentals

*Vacancy Y-o-Y changes are calculated by comparing the difference between H1 2025 and H1 2024.

**Rental rates are quoted asking rates for 250+ kW at N+1/Tier III requirements.

Source: CBRE Research, CBRE Data Center Solutions, H1 2025.

Looking ahead, CBRE expects the following market conditions:

- Pricing will remain elevated, comparable to 2011–2012 levels at $200+ per kilowatt (kW) per month, though sustained double-digit annual increases are unlikely.

- In Dallas-Fort Worth, recent completions and ongoing projects will double the market’s size by year-end 2026.

- Large occupiers requiring 10-to-30 MW of continuous capacity will continue to face rental rate premiums, outpacing growth for smaller-scale needs.

- Markets with low power costs such as Atlanta, Charlotte-Raleigh, Dallas-Fort Worth, Austin and San Antonio are poised for accelerated supply growth.

- Development activity is shifting to emerging markets with faster power access, as established hubs face constraints.

Related Insights

-

Mortenson’s Maja Rosenquist and CBRE’s Gordon Dolven examine one of real estate’s most dynamic sectors. They discuss how AI’s growth has accelerated data center development, how site-selection strategies are evolving and the challenges posed by power constraints.

-

While economic uncertainty tempers growth, fundamentals remain healthy with pockets of outperformance across the industry.

-

Global data center growth surges as hyperscale demand fuels expansion in emerging markets, despite power constraints.

-

CBRE explores top data center markets in North America, reporting on supply, demand, and pricing trends for 2024.