Intelligent Investment

Potential Impact of Rising Oil Prices on Real Estate Values

March 30, 2026 3 Minute Read

Executive Summary

- While the link between crude oil prices and capitalization rates is relatively modest, oil prices have an indirect impact because they strongly influence monetary policy, inflation expectations and long-term interest rates.

- Upward pressure on cap rates, which are highly sensitive to long-term interest rates, is more likely as the Middle East conflict drags on and oil prices contribute to higher inflation.

- Global uncertainty is exceptionally elevated because of the near closing of the Strait of Hormuz, through which approximately 25% of the world’s seaborne oil trade transits.

- We have not yet seen any direct impact of rising oil prices on commercial real estate occupier demand.

Since the Middle East conflict began on Feb. 28, Brent crude oil prices have been extremely volatile, ranging from $70 to $115 per barrel.

For real estate investors, the impact of a sudden, dramatic rise in oil prices on cap rates (known as yields in Europe) can be multifaceted. Higher energy costs could erode operating margins for commercial tenants, weakening their ability to afford rents and, potentially, reducing occupier demand. Expectations of rising inflation could persuade central banks to maintain or tighten monetary policy, keeping interest rates higher for longer. Together, these dynamics could push cap rates upward, particularly in energy-sensitive sectors like data center and industrial & logistics facilities.

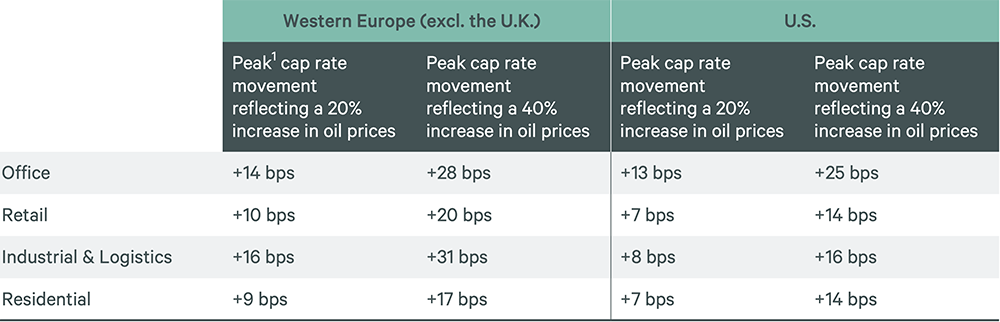

In the table below, CBRE estimates the potential impact of a crude oil supply shock under two scenarios. Our base case assumes a 20% oil price increase based on Brent crude oil futures for September 2026, while our downside scenario assumes a 40% oil price increase. This analysis reveals three notable patterns:

- Western European cap rates (excluding the U.K.) are more sensitive than U.S. cap rates to oil price changes, reflecting the eurozone's greater dependence on imported energy.

- Residential cap rates show more limited sensitivity than most other property sectors in both Western Europe and the U.S. This is due to the need-driven nature of housing demand.

- The U.S. is more resilient to oil price shocks, with cap rate impacts peaking and dissipating faster than in Western Europe.

Figure 1: Effect of Brent oil price increases on European & U.S. cap rates

1 Peak refers to the biggest annual increase in cap rates over the next four years that is caused by the percentage rise in oil prices due to an unexpected supply shock.

These findings reinforce our belief that commercial property returns will be largely driven by net operating income in this cycle. As such, investors may favor assets with longer weighted-average lease expirations, as well as those in more defensive sectors such as multifamily.

Contacts

Dennis Schoenmaker, Ph.D.

Global Head of Forecasting and Strategic Insight, Head of Data Centre of Excellence