Intelligent Investment

Private Credit Stress: Contained or Contagious?

May 11, 2026 3 Minute Read

Executive Summary

- Issues in private credit are unlikely to pose systemic risk to financial markets. Consequently, we do not view this as a major issue for commercial real estate, though there are some potential impacts.

- Current stress in private credit is largely concentrated in the corporate direct lending segment. Commercial real estate could be indirectly impacted if private credit stress causes banks to tighten credit lines or if LPs lose enough confidence to slow real estate fundraising. A wall of maturities in 2026 would exacerbate such challenges, should they emerge.

- Private credit is a much smaller debt class than subprime mortgages, which precipitated the Global Financial Crisis (GFC). Banks are better capitalized today vs. pre-GFC, lending support to the view that private credit stress is likely to remain contained.

- CBRE is closely watching linkages between the macro environment and public policy changes that could interact adversely with stress in the private credit market.

Defining Private Credit

As a segment of the lending market outside of traditional public bond markets or bank syndication, private credit attracted investors by offering higher yields than investment-grade bonds or public equity as well as the perceived opportunity to achieve returns that are uncorrelated to the public markets. We grouped the sector into the following categories:

Corporate Direct Lending

Primarily senior secured term loans and subordinated debt to middle market borrowers, typically non-rated, with credit profiles broadly equivalent to single-B equivalent or lower. Spreads are quoted over SOFR, typically S+450-500bps (dependent on borrower size, sector, and position in the capital structure), with 8.5% to 9.5% yields. Total leverage typically runs 5-6x EBITDA, with senior debt at 4-5x. Business Development Companies (BDCs) are the primary stress signal being monitored since this is one of the few private credit segments with public exposure (quarterly NAVs, traded equity), thus offering a real-time window into private credit performance.

Asset-Backed

Senior secured or subordinate exposure to consumer and commercial loan pools (autos, credit cards, student, trade receivables, leases, etc.) with credit enhancement sized to historical loss curves/experience.

Commercial Real Estate Mortgages

Senior secured or subordinate financing collateralized by commercial real estate, originated by debt funds operating since the mid-90s. Credit enhancement sized to LTV, DY, and DSCR rather than EBITDA multiples. Tangible collateral, institutional LP base, no quarterly redemption obligations, and the segment benefits from a value reset following a decline driven by higher interest rates.

Infrastructure

Project lending backed by cash-flow-producing hard assets, with return profiles driven by contracted revenue rather than corporate earnings.

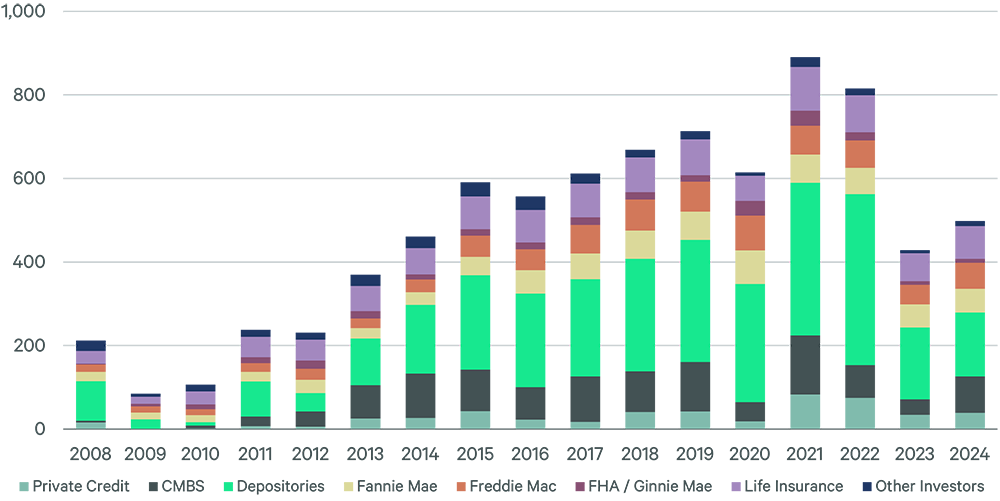

Alternative lenders, including commercial real estate debt funds and mortgage REITs, accounted for 40%1 of non-agency closings in Q4 2025 making them a primary source of bridge, mezzanine and transitional financing in parts of the capital stack, which do not typically appeal to banks and government agencies.

Figure 1: Commercial Real Estate Lending Market Share ($Bn)

Potential Risks Emanating from Private Credit

Issues in private credit are mostly confined to Business Development Companies (BDCs), particularly those lending in the software sector. BDCs are primarily corporate and middle-market lenders with limited or incidental commercial real estate exposure. Unlike many commercial real estate funds, BDCs often offer periodic redemption opportunities, attract more retail capital and underwrite to borrower cash flows rather than hard asset collateral. BDC portfolio deterioration doesn’t directly reduce commercial real estate debt fund lending capacity; these are separate pools of capital with different mandates, collateral types and investor bases. Nevertheless, three structural features of BDCs warrant closer attention.

- Borrower Concentration in Tech and Software

Tech and software accounts for 20% to 40%2 of BDC loan books and AI disruption has caused many to question borrower long term creditworthiness. - Liquidity Mismatch

BDC portfolios are inherently illiquid and have no secondary market depth. Under stress, redemption requests can create self-reinforcing negative feedback loops, pressuring funds. Redemption caps provide some buffers but offering liquidity to investors with illiquid assets remains a structural mismatch. - Listed vs. Unlisted BDCs

Listed BDCs have fewer redemption risks due to easier exit via secondary markets, but they are exposed to price risk as market sentiment shifts. Meanwhile, unlisted BDCs have a more stable capital base, but are more exposed to risks during redemption periods.

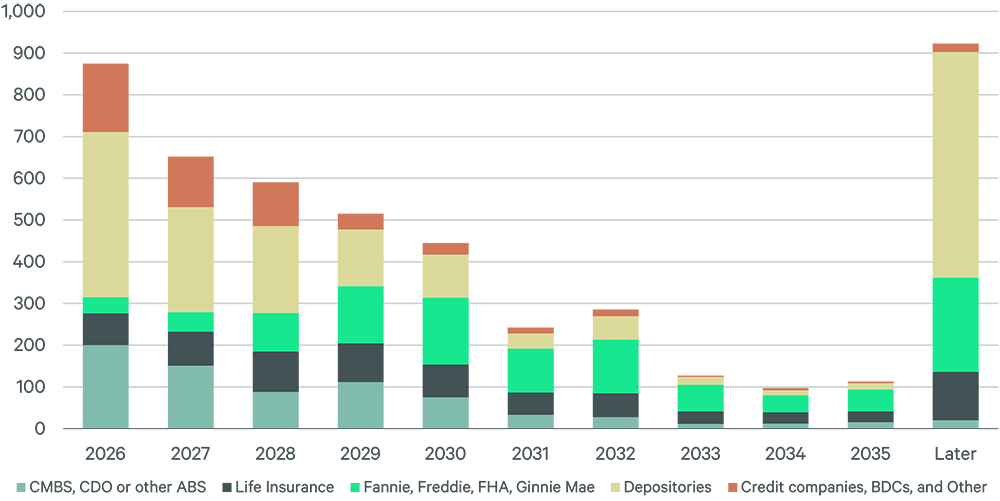

There could be indirect impacts to commercial real estate. Key areas to watch include bank credit line tightening across private credit vehicles, LP confidence deterioration—which could slow commercial real estate fundraising—and liquidation sequencing that hits illiquid assets later. Additionally, the 2026 maturity wall totaling over $800 billion3 amplifies indirect risk. If lending capacity shrinks at the right time, commercial real estate loan maturities coming due could find limited options, potentially causing distress or even a decline in values.

Figure 2: Commercial Real Estate Debt Maturities by Lender Type

Key Differences with the Global Financial Crisis (GFC)

Private credit stress today is structurally different from GFC conditions, with a risk profile more consistent with a contained credit cycle than a systemic unwind.

- BDC total assets of ~$451 billion4 are well below the ~$1.5 trillion5 in subprime exposure at the center of the GFC.

- Redemption caps limit forced selling.

- The investor base is largely institutional, despite some panic-induced outflows from high-net-worth retail capital.

- Exposure is distributed across diverse industries rather than a heavily concentrated bet on housing (as in the GFC), though the 20-40% exposure to tech and software as a service (SaaS) is worth monitoring.

- Regulated BDCs operate under a leverage cap of 2x, well below the 30x that made GFC-era subprime so fragile.

- Banks themselves are better capitalized today with capital cushions roughly double pre-GFC levels, reducing the likelihood that private credit stress evolves into a broader banking system problem.

Our View

Our analysis indicates that private credit stress is not likely to escalate into market contagion. The structural buffers discussed above support this view. The variables we are watching include: bank warehouse line behavior, where any pullback would directly constrain private credit deployment capacity; BDC NAV trends vs. realized losses, where current marks may understate stress; and office-related maturity and workout activity, which could drive losses in private credit vehicles.

The greater risk may stem from private credit issues interacting with macro conditions and policy changes. Regulatory tightening under Basel III and potential Synthetic Risk Transfer (SRT) reclassification could constrain the bank linkages that private credit depends on. This may coincide with higher tariffs that raise construction costs and weigh on broader economic activity. Other factors that may cause complications include restrictive immigration policy that affects labor availability on the supply side, and residential and retail on the demand side. The ongoing Middle East conflict also presents energy price and inflation risks that could keep interest rates elevated longer than anticipated. Any of these factors could interact unpredictably with existing private credit strains to produce outcomes worse than our base case.

The Bottom Line

The current consensus view holds that a systemic crisis stemming from private credit is unlikely. CBRE shares this view given the limited direct linkages between BDC stress and commercial real estate lending, structural buffers in private credit, CMBS markets remaining open for quality collateral, and the relative resilience of hard asset lending. Still, indirect risks remain, as ongoing macro and geopolitical uncertainty coincides with a wall of approaching debt maturities. As such, we will continue to monitor credit and macroeconomic conditions.

1 CBRE, “Commercial Real Estate Lending Momentum Continues to Improve,” (Feb 2026).

2 Estimates vary by source and classification methodology, ranging from ~20% under narrow definitions to ~30%+ under broader classifications. See Octus, “BDC Performance, Software Exposure Trigger Pricing Fears” (Mar 2026); UBS, “2026 Private Credit Outlook: Defaults, Disruption and Dispersion” (Jan 2026); MSCI, “Run Risk or Rational Repricing?”, (2026).

3 Mortgage Bankers Association

4 Mayer Brown LLP, “BDC Facts & Stats,” (June 2025).

5 Federal Reserve Bank of Chicago, “Comparing the Prime and Subprime Mortgage Markets,” (August 2007).

Related Insights

-

In this episode of Capital Markets Conversations, Talia Hall, a member of the CBRE Investment Banking team, offers a grounded, data-informed view of where the real risks lie—and where they don't.

-

U.S. cap rates show signs of stabilization, with improving liquidity, firmer pricing and growing confidence that yields are past their peak.

-

Nearly three quarters of commercial real estate investors plan to buy more assets in 2026 as prices stabilize and fundamentals improve.

Related Services

- Invest, Finance & Value

Capital Markets

Gain proactive insights and strategies that unlock value, drive returns and enhance outcomes for your real estat...

- Invest, Finance & Value

Debt & Structured Finance

Find innovative options for any capital requirement with our unique combination of robust lender relationships, leading deal volume and proprietary te...