Intelligent Investment

Some Distress Will Emerge Amid Wall of Loan Maturities

May 8, 2024 3 Minute Read

Executive Summary

- Although more defaults are likely, we expect that a significant amount of commercial real estate loan maturities this year will be extended to 2025 and beyond.

- Loan defaults will be concentrated in office, which suffers from high vacancy and lower demand, and in multifamily, where many investors who financed acquisitions at ultra-low interest rates face significantly higher debt servicing costs as loans mature.

- Bank lending will remain subdued given less capital to recycle as loans are extended and regulators manage banks’ exposure to commercial real estate.

- More favorable pricing amid high interest rates and less debt availability will create unique opportunities for investors less reliant on debt capital.

Looming Wall of Maturing Loans

Nearly $2 trillion of the $4.7 trillion in commercial real estate loans nationwide will mature over the next three years, according to the Mortgage Bankers Association. CBRE expects that most of these loans will be extended, although some forced sales will occur as lenders lose patience or borrowers default.

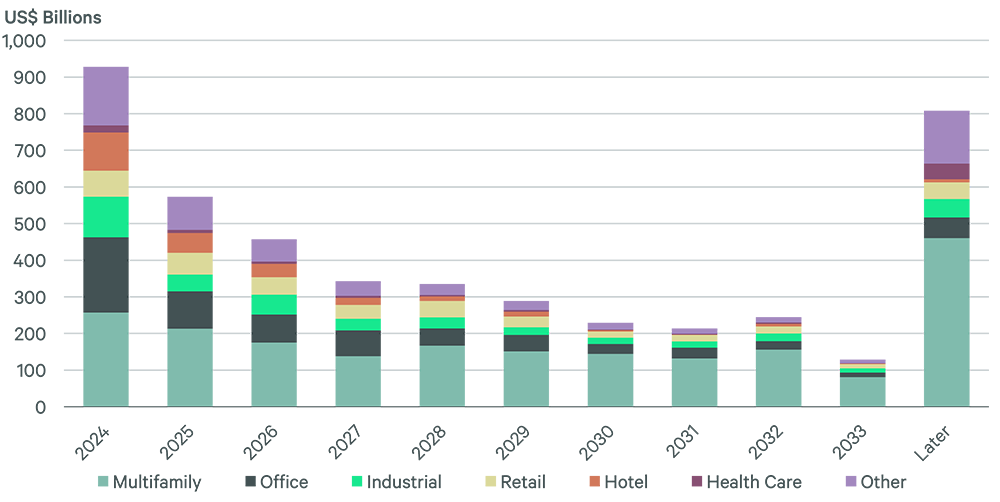

Figure 1: Commercial Real Estate Loan Maturities by Property Type

Profile of Loan Maturities

Of the $900 billion in commercial real estate loans maturing this year, multifamily accounts for $257 billion and office $206 billion. Maturing loan totals for other sectors include $110 billion for industrial, $105 billion for hotels, $71 billion for retail and $19 billion for health care.

Many of the $700 billion in loans that came due last year were extended, increasing the total of loans coming due this year by $271 billion. Similarly, we expect that many of the 2024 maturities will be extended to 2025.

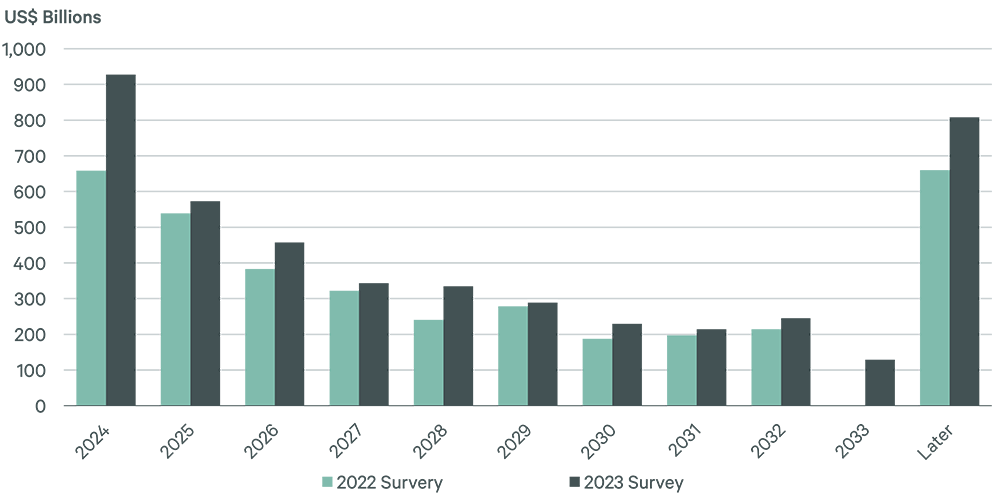

Figure 2: Expectations for Annual Commercial Real Estate Loan Maturities, 2022 vs. 2023 MBA Surveys

Office sector loan maturities are the most concerning given the big drop in demand and associated impacts for office space since the pandemic. We expect that lenders will prefer to extend many of these loans rather than foreclose, particularly for assets that would realize large losses, like downtown office towers. However, some defaults will occur, particularly for the hardest-hit buildings.

The outlook for the multifamily sector is much different since it does not suffer from weak underlying fundamentals. However, there will be challenges with refinancing, as many borrowers took advantage of low interest rates and floating rate loans in 2021 and 2022. CBRE expects that lenders will work with borrowers. One-year extensions will be most common in hopes of lower interest rates next year. However, lenders will take back multifamily properties if they are at risk of a decline in value due to poor maintenance.

Figure 3: Commercial Real Estate Loan Maturities by Lender Type

Opportunities in a Challenging Lending Environment

Banks, which currently hold about 38% of total commercial real estate debt, will focus on maintaining their current loan portfolio and managing exposure to the sector over the next several years. This will be partly driven by greater regulatory scrutiny. Consequently, we think bank lending for commercial real estate will be relatively subdued. This will create an opportunity for private lenders to step in. We expect that opportunities for development and bridge loans will be particularly attractive.

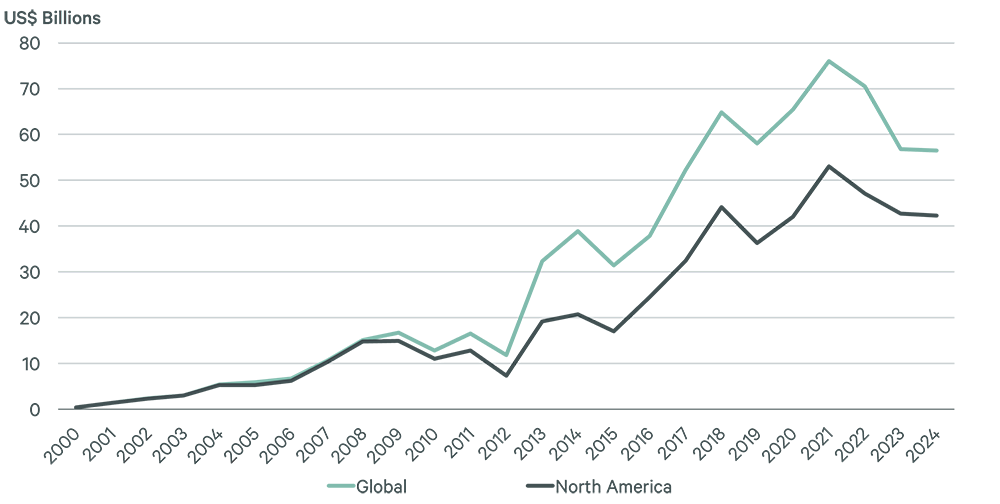

Figure 4: Real Estate Dry Powder – Debt Strategies

The Federal Reserve’s cautious approach to cutting interest rates this year will give investors more time to explore debt opportunities. It also will extend the window of opportunity for investors less dependent on debt capital, such as large endowments and sovereign wealth funds.

Despite negative sentiment about the office sector, seller capitulation is beginning to provide investment opportunities in some markets, particularly for Class A and B+ assets. Although many of these assets will require capital improvements, they offer the prospect of healthy returns over the long term, particularly in strong live-work-play districts and in large established markets with development constraints. Many of the big institutional investors also have increasing interest in prime trophy assets, given their relatively strong fundamentals.

While many opportunistic investors have raised funds in anticipation of distress, little has emerged so far. Still, there will be pockets of opportunity to provide capital to borrowers looking to address debt funding gaps with fresh equity and/or mezzanine debt. There also will be opportunities to acquire properties that lenders have taken back and will require capital improvements.