Future Cities

Atlanta

2024 North America Industrial Big-Box Review & Outlook

April 29, 2024 5 Minute Read

Demographics

Atlanta is the major population center of the Southeast and one of the country’s fastest-growing metropolitan statistical areas (MSAs). Over 6.4 million people live within 50 miles of the market’s core, with a projected five-year growth rate of 3.6%. Within 250 miles, occupiers can reach nearly 30 million people, with 23% aged 18-34.

Figure 1: Atlanta Population Analysis

The Atlanta MSA has 149,224 warehouse workers—a workforce that is expected to grow by 12% by 2034, according to CBRE Labor Analytics. The average wage for a non-supervisory warehouse worker is $17.78 per hour, on par with the national average.

Figure 2: Atlanta Warehouse & Storage Labor Fundamentals

*Median wage (1 year experience); non-supervisory warehouse material handlers.

Location Incentives

Over the past five years, there have been over 130 economic incentives deals for an average of $11,200 per new job in metro Atlanta, according to fDi Intelligence.

CBRE’s Location Incentives Group reports that top incentive programs in metro Atlanta include the Regional Economic Business Assistance (REBA) program. REBA is considered a “deal-closing” grant because it incentivizes construction in Georgia. REBA funds may be used for any fixed-asset costs, including infrastructure, construction, real estate and personal property.

Another program available in Atlanta is the Job Tax Credit, which awards businesses for creating net new full-time jobs. These credits can be applied toward a company’s corporate income tax liability or reduce the company’s payroll withholding requirements. To qualify, companies must have local headquarters or R&D operations in one of the following industries: manufacturing, warehousing/distribution/logistics, software development, contact centers, data centers, telecommunications or financial technology.

Figure 3: Atlanta Top Incentive Programs

Note: The extent, if any, of state and local incentive offerings depends on location and scope of the operation.

Logistics Driver

Atlanta offers port, rail, air and road logistics options. With service from CSX Transportation, Norfolk Southern and nearly two dozen short-line railroad companies, Atlanta has the most extensive rail system in the Southeast and serves as the region's largest intermodal hub. Interstate highways connect to 80% of the U.S. population within a two-day truck drive.

Atlanta Hartsfield-Jackson International Airport continues year-over-year gains in cargo volume. Georgia's seaports are magnets for international trade and investment. As the westernmost container port on the U.S. East Coast, the Port of Savannah enjoys a significant geographical advantage in reaching inland markets. Opened in 2018, the Appalachian Regional Port is also a gateway to North American markets. A network of major interstates, including north-south corridors I-95 and I-75 and east-west routes I-16, I-20 and I-85, means key cities and manufacturing points throughout the Southeast and Midwest can be reached within a one- to two-day drive.

Interstate highways connect to 80% of the U.S. population within a two-day truck drive.

Supply & Demand

Atlanta is North America’s fifth-largest big-box industrial market, with 393 million sq. ft. of total inventory. Vacancy rates have increased to 9.4% due to a combination of record new construction and a nearly 40% reduction in leasing activity, significantly higher than the 6.2% rate in 2022. Despite the decrease in leasing, rental rates continued to rise, with first-year base rents finishing the year at $5.84 psf/yr, a 12.3% increase from 2022. General retailers & wholesalers were the most active occupiers, representing 36.5% of total lease volume. The 3PL (27.2%) and automobile (16.7%) sectors were the second- and third-most active occupiers, respectively.

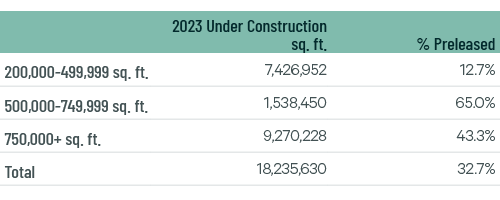

Difficulties in construction financing and rising vacancy rates have decreased the amount of product under construction to 18.2 million sq. ft. by year-end. 32.7% is preleased, nearly 20 million sq. ft. less than the previous year. The decline in product under construction will contribute to a slower increase in vacancy rates this year. Additionally, leasing activity should increase due to steady consumer spending and the stabilization and eventual decrease in interest rates. Atlanta will continue to benefit from population growth in the Southeast, remaining the region’s primary big-box hub for the foreseeable future.

Figure 4: Share of 2023 Leasing by Occupier Type

Source: CBRE Research.

Figure 5: Lease Transaction Volume by Size Range

Source: CBRE Research.

Figure 6: 2023 Construction Completions vs. Overall Net Absorption by Size Range

Figure 7: Direct Vacancy Rate by Size Range

Figure 8: Under Construction & Percentage Preleased

Figure 9: First Year Taking Rents (psf/yr)

Source: CBRE Research.

Explore Big-Box Insights by Market

-

Over 4 million people live within 50 miles of the market’s core, with a 5% expected five-year growth rate—the second-highest of any region in the Southeast.

-

Nearly 30 million people—24% aged 18-34—live within 250 miles of downtown Louisville.

-

Over 1.4 million people–23% aged 18-34–live within 50 miles of downtown Memphis.