Intelligent Investment

2024 Global Multifamily Investor Intentions Survey

March 20, 2024 8 Minute Read

Multifamily Remains Most Preferred Sector for Global Real Estate Investors

CBRE's 2024 Global Multifamily Investor Intentions Survey reveals upbeat investor sentiment despite persistently high interest rates, tight credit availability and softening fundamentals.

Among all major real estate sectors, multifamily remained the top acquisition target this year. Nearly half of the 1,200 global investors surveyed by CBRE in late 2023 said they would primarily invest in multifamily assets and increase their purchasing activity in 2024. Investment activity is expected to pick up in the second half of the year, with more investors considering lower-risk strategies than in 2023.

Key Findings

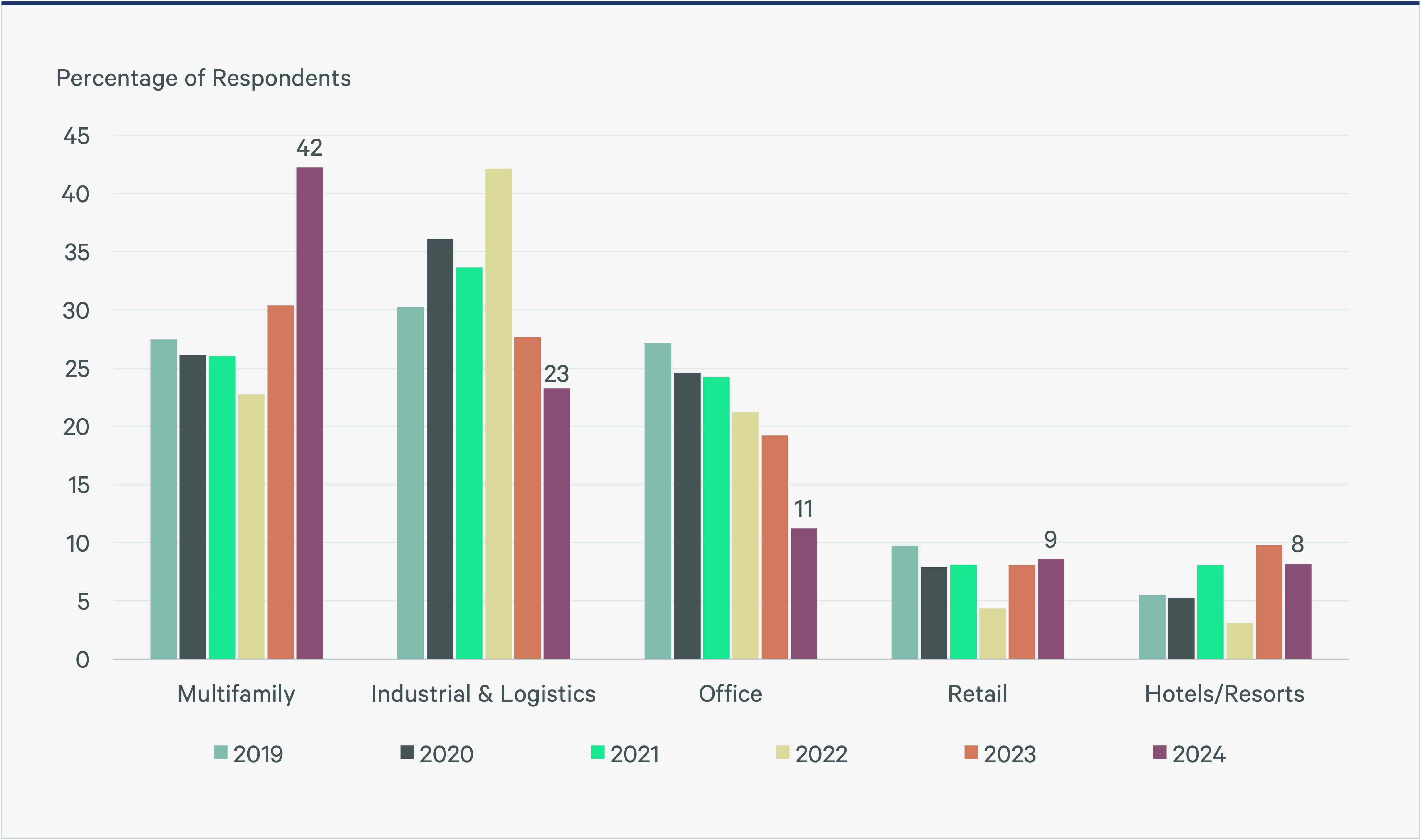

- Multifamily remained the most-preferred sector, favored by 42%of survey respondents vs. a lower top-rank 30% in 2023.

- For the first time in this survey’s eight-year history, multifamily was the most preferred sector in all three main global regions (Americas, Europe and Asia-Pacific).

- Industrial & logistics remained the second most-preferred asset type this year, favored by 23% of survey respondents vs. 28% last year.

- Despite softening fundamentals from a glut of new supply, U.S. Sun Belt markets were again the most attractive for investment in the Americas.

- While Dallas-Ft. Worth remained the most targeted market in the Americas, two new markets—Atlanta and Charlotte—entered the top five.

- Global gateway markets remained the most attractive for European and Asia-Pacific (APAC) investors. London and Tokyo retained the top spots for their respective regions.

- Almost 60% of survey respondents expect to see small or no price discounts for multifamily assets this year, up slightly from 2023.

- 34% expect mid-to-large discounts, down from 44% in 2023. This is the second lowest percentage of any other asset type, behind industrial & logistics (25%).

- 62% of multifamily investors expect to increase their purchasing activity from last year, while 40% expect to sell more. Multifamily had the highest percentage of investors (27%) expecting to sell less this year.

- 47% of multifamily investors view high-risk (i.e., opportunistic, distressed and debt) as the most attractive investment strategy in 2024, down from 50% in 2023. Preference for lower-risk (i.e., core and core-plus) strategies increased to 33% of survey respondents from 27% in 2023.

- Student housing is the most preferred alternative sector, particularly in Europe where half of all investors favor it.

- Senior housing saw a resurgence in preference this year after three years of waning interest. A third of all European investors said they are interested in the sector.

- Build-to-Rent/Single-Family-Rental housing (BTR/SFR) was the second most preferred alternative sector among Americas investors (39%) after real estate debt (41%).

Multifamily Most Favored Property Sector for 2024

Multifamily once again is the most targeted real estate sector for investors in 2024, favored by 42% of global investors surveyed by CBRE vs. 30% in 2023. For the first time in this survey’s eight-year history, multifamily was the most preferred sector in all three global regions, favored by 44% of investors in the Americas, 44% in Europe and 32% in APAC vs. 37%, 25% and 30% last year, respectively.

Figure 1: Preferred Property Sector as Primary Investment Target

Note: Europe not included in 2020 data.

Most Attractive Markets for Multifamily Investment

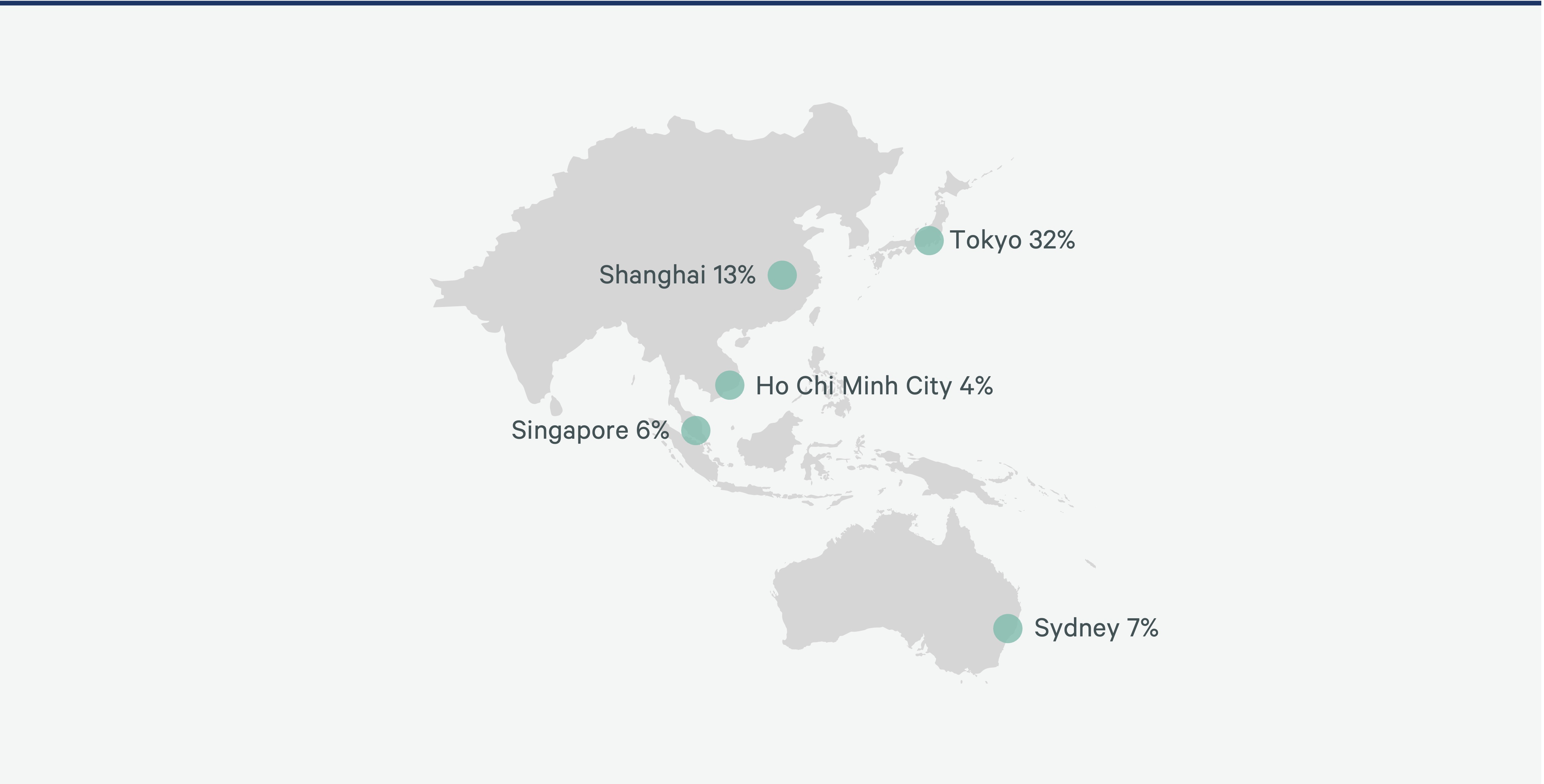

Figure 2: Which markets are the most attractive for multifamily investment in 2024?

U.S. Sun Belt markets were again the most favored by Americas investors, led by Dallas-Ft. Worth with 40% vs. 36% in 2023. Nashville and Raleigh-Durham tied for second, although the percentage of investors favoring them (21%) fell slightly from last year. Atlanta ranked fourth and Charlotte and Miami-South Florida tied for fifth.

Forty-five percent of European investors favor London this year, up from 38% last year. Berlin was second with 26% and Paris third with 24%. Amsterdam remained fourth with 19%, while Munich replaced Madrid for fifth with 16%.

Tokyo remained the top market in APAC, favored by 32% of that region’s multifamily investors. Shanghai was second with 13%, followed by Sydney with 7%, Singapore with 6% and Ho Chi Minh City with 4%.

Moderating Risk Strategies in 2024

Forty-seven percent of multifamily investors view high-risk (i.e., opportunistic, distressed and debt) as the most attractive investment strategy in 2024, down slightly from 50% in 2023. Preference for lower-risk (i.e., core and core-plus) strategies increased to 33% in 2024 from 27% in 2023. Multifamily investors had the greatest preference for lower-risk strategies when compared with industrial investors (32%) and office investors (26%).

Figure 3: What investment strategy is most attractive for your organization?

(Multifamily Investors Only)

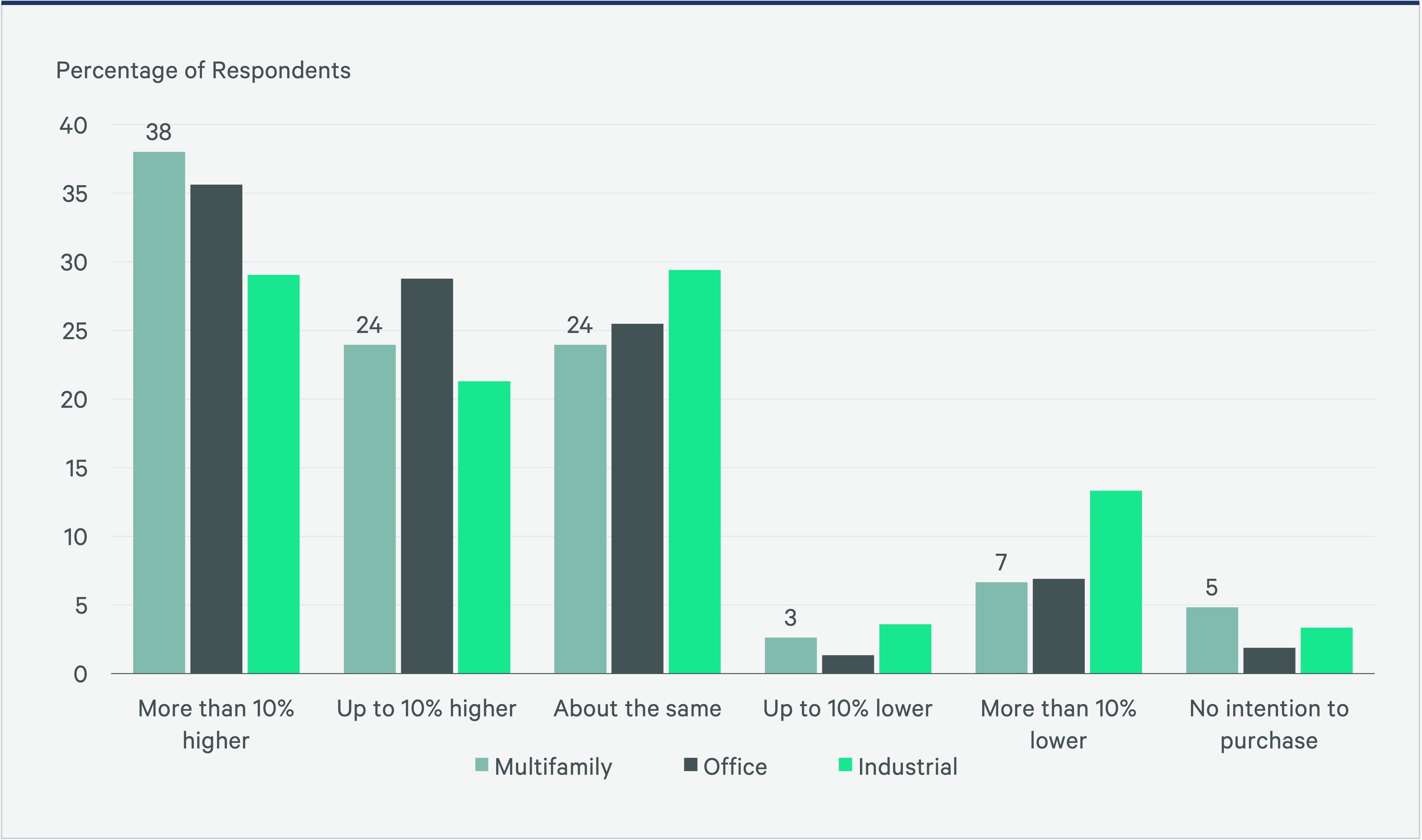

Greater Purchasing Activity Expected in 2024

Sixty-two percent of multifamily investors expect to increase their purchasing activity in 2024, with the greatest share (38%) expecting an increase of at least 10% over 2023, compared with 36% of office investors and 29% of industrial investors. Multifamily investors in the Americas were the most bullish, with 41% saying their purchasing would increase by at least 10% in 2024.

Figure 4: Compared with 2023, do you expect your purchasing activity will be higher, lower or the same?

Sales Expectations

Less than half (40%) of multifamily investors expect to increase their selling activity in 2024, compared with 47% of office investors and 44% of industrial investors. Multifamily had a greater share (26%) of investors who either intended to sell less or not at all in 2024 than industrial (20%) and office (18%). Forty-three percent of European and APAC multifamily investors said they would increase their selling activity, compared with 39% of Americas multifamily investors.

Figure 5: Compared with 2023, do you expect your selling activity will be higher, lower or the same?

Most Investors Expect Increased Activity in H2 2024

Nearly a third of multifamily investors expect their own investment activity to begin recovering in the first half of 2024 vs. only 9% who expect the same for the overall multifamily market. Most investors expect a recovery to begin for both their own organization and the overall market in the second half of the year. By mid-2025, nearly all investors expect that the multifamily investment recovery will be well underway.

Figure 6: When do you expect investment activity to begin recovering?

(Multifamily Investors Only)

Most Investors Expect Small or No Discounts for Multifamily Assets

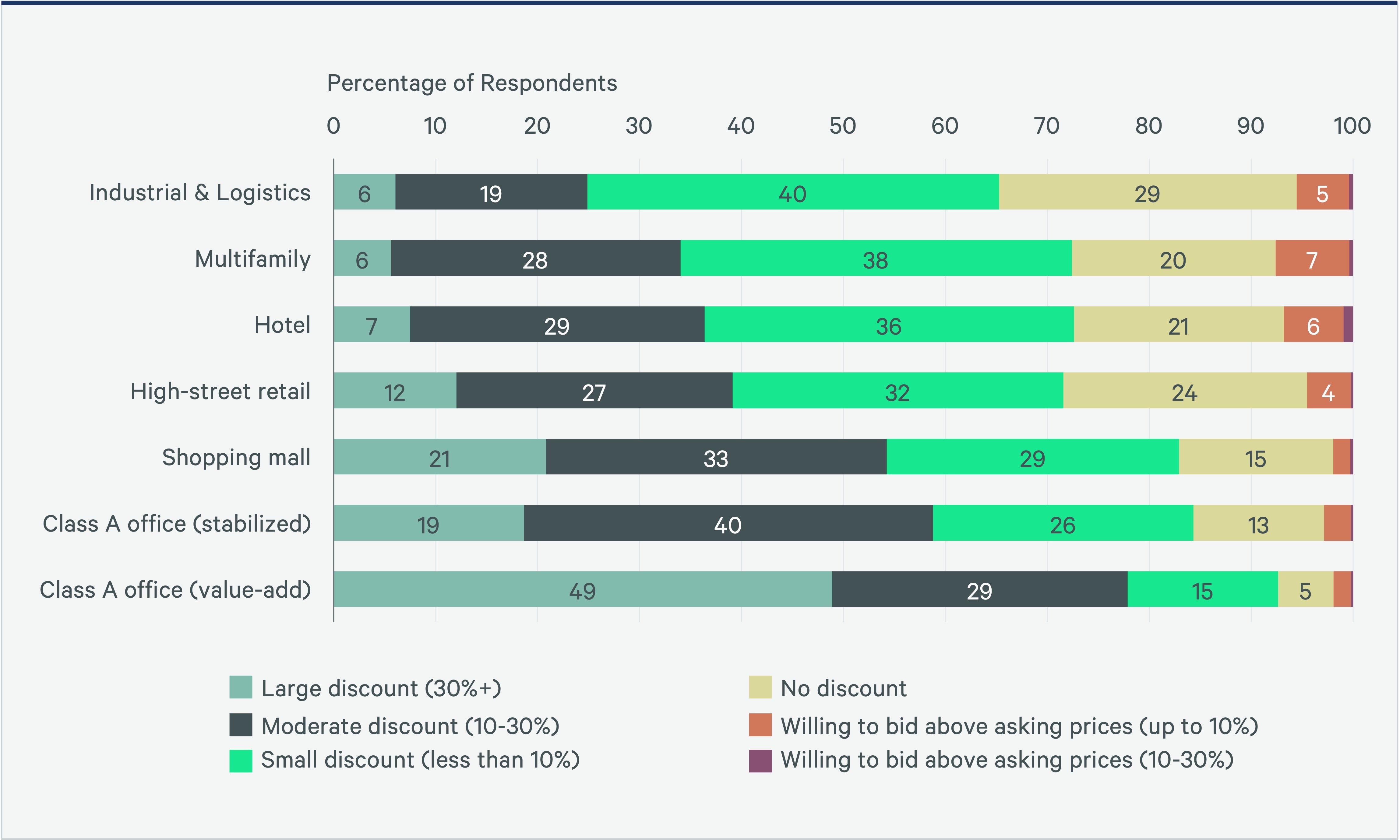

Fifty-eight percent of investors expect multifamily assets to have either small or no pricing discounts in 2024. Just 34% expect to see moderate-to-large discounts, down from 44% in 2023. This is second lowest percentage of any other asset type, behind industrial & logistics (25%).

Only 6% expect large discounts for multifamily and 20% expect no discounts at all. Multifamily had the highest rate (8%) of investors willing to bid above asking price, up from 5% in 2023.

Figure 7: What are your pricing expectations for different sectors compared with 2023?

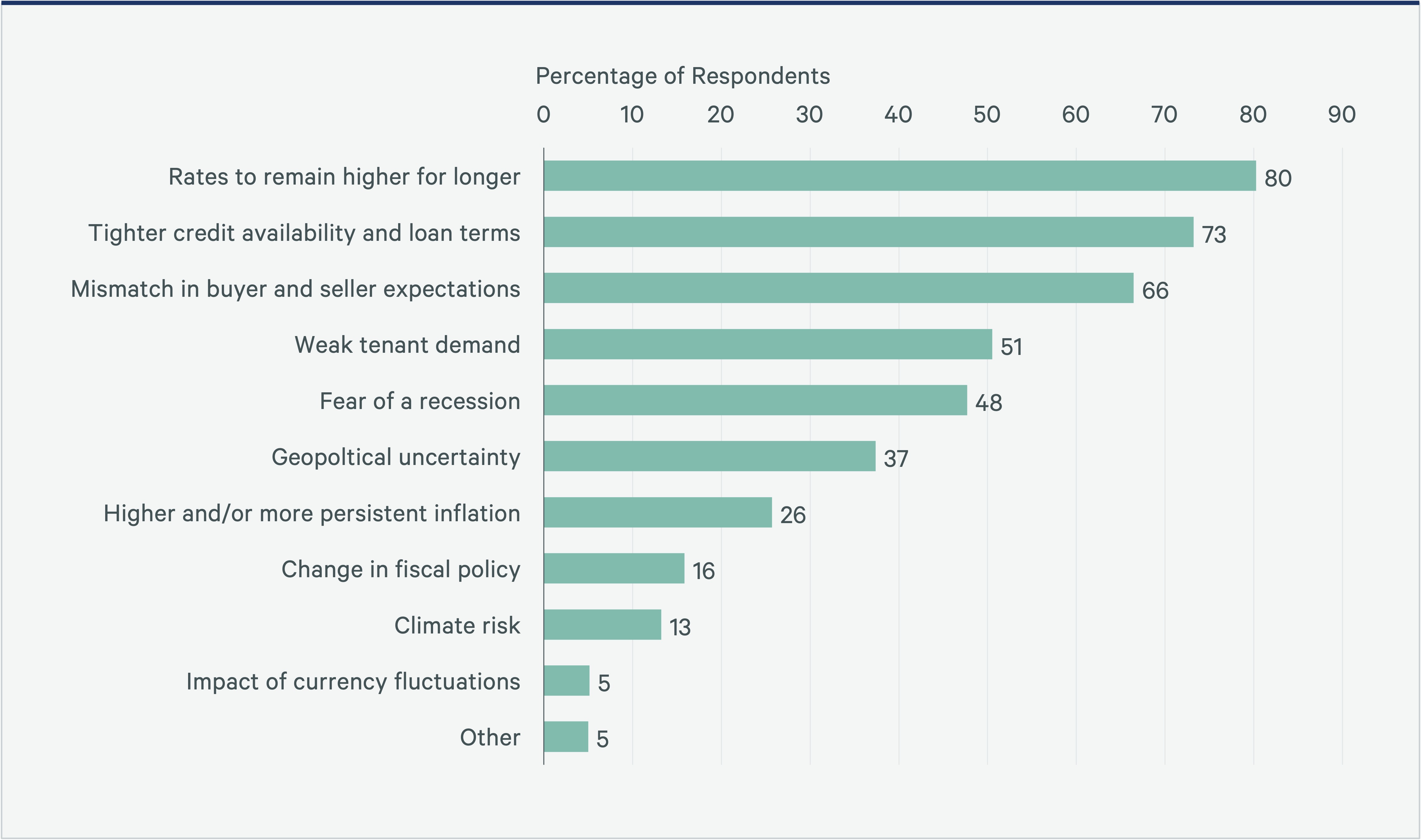

Higher Interest Rates, Credit Availability Are Top Concerns

Over 80% of multifamily investors cited interest rates as the primary challenge to commercial real estate investment this year. Credit availability and mismatches in buyer and seller expectations were cited as top challenges by 73% and 67% of respondents, respectively.

Half of surveyed investors cited the potential for weak tenant demand this year versus only 15% in 2023. Only 26% cited higher and more persistent inflation as a top challenge, down from 31% in 2023.

Figure 8: What are the major challenges for real estate investment in 2024?

(Multifamily Investors Only)

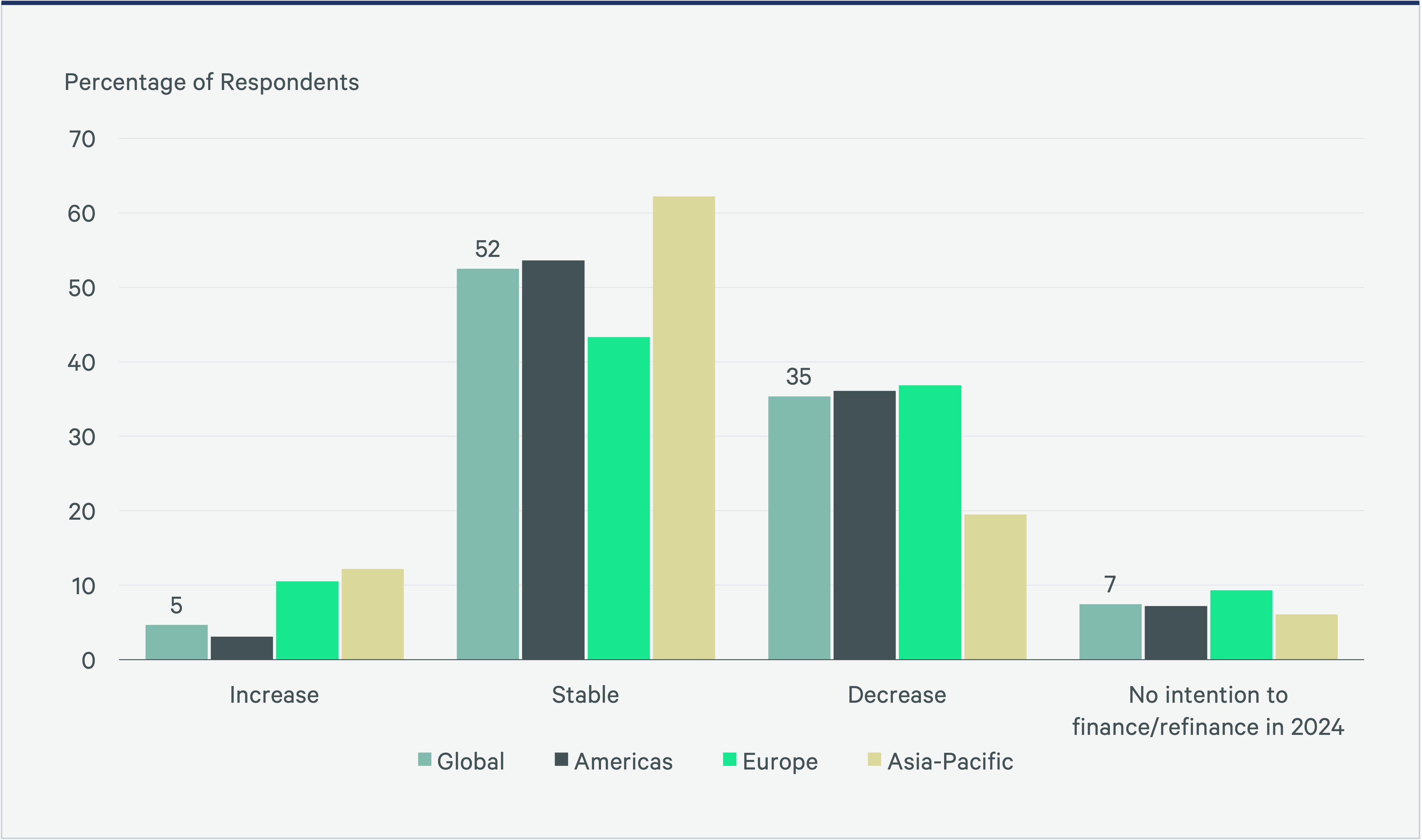

Most Multifamily Investors Expect No Change in Debt-to-Equity Ratios

The majority (52%) of multifamily investors expect no change in their debt-to-equity ratio when financing or refinancing assets. Thirty-five percent expect a decrease in the ratio, while only 5% expect an increase. Industrial and office investors had similar expectations.

Figure 9: Will you increase, decrease or maintain your debt-to equity ratios when financing or refinancing in 2024? (Multifamily Investors Only)

Investors Maintain Preferences for Multifamily Alternatives

Student housing is the most preferred alternative sector for investors globally, particularly in Europe where half of all investors favor it. Senior housing saw a resurgence in preference this year to 23% after three years of waning interest. A third of all European investors said they are interested in the sector.

BTR/SFR was the overwhelming top multifamily alternative (39%) for Americas investors, second only to real estate debt (41%).

Figure 10: Will you pursue investments in any of the following alternative sectors in 2024?

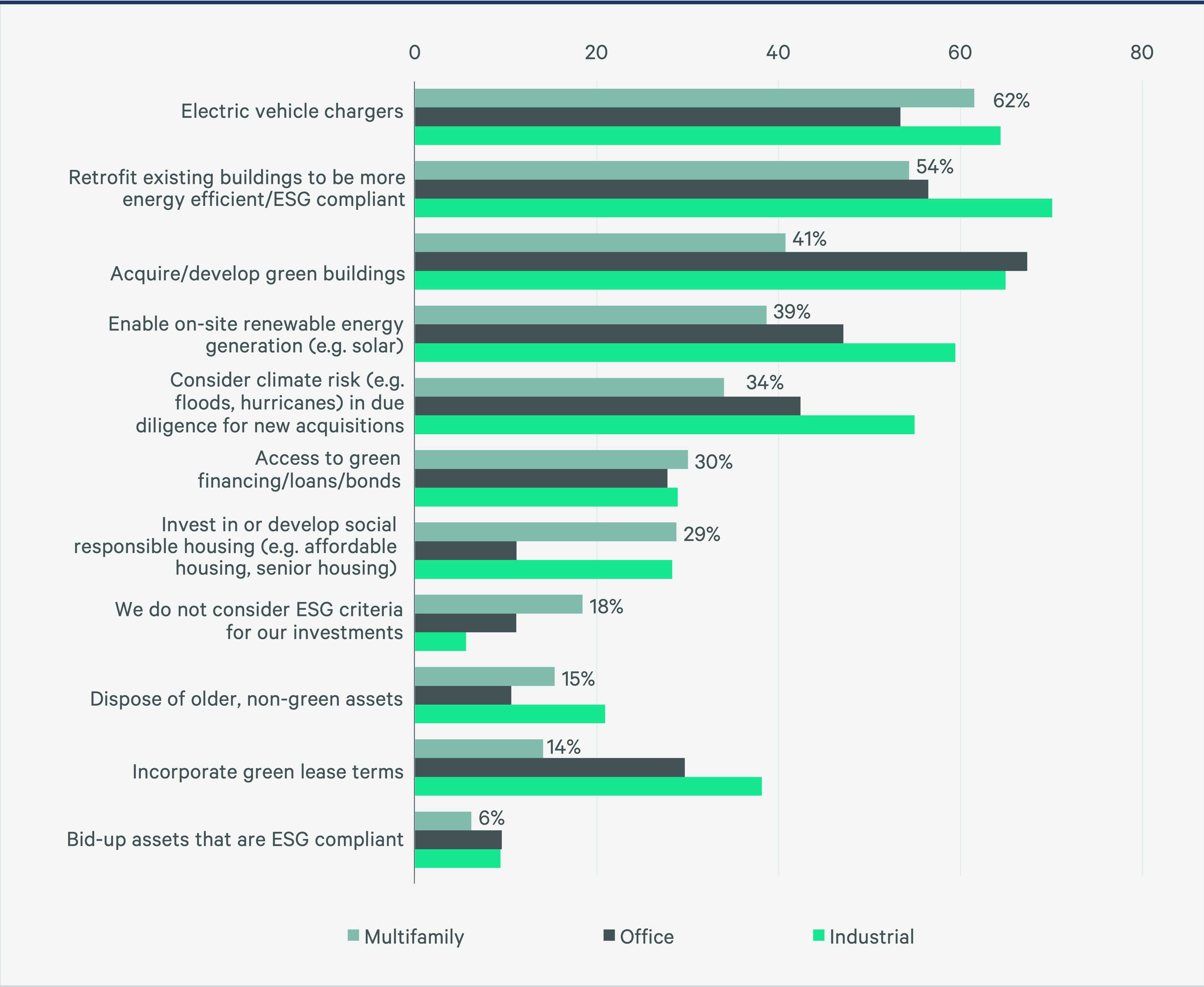

EV Chargers, Energy Efficiency Are Top ESG Initiatives

Just over 60% of multifamily investors said they would consider installing electric vehicle (EV) chargers at their properties, while 54% said they would consider retrofitting existing buildings for energy efficiency as their top ESG initiatives in 2024. Multifamily investors lagged office and industrial investors on every ESG category except for not considering ESG initiatives at all, albeit at a relatively small 18%.

Subsidized housing, which includes affordable housing, has garnered slightly more interest from global investors, indicating that they see value in the social component of ESG.

Figure 11: Which ESG initiatives will you consider for your real estate investments?

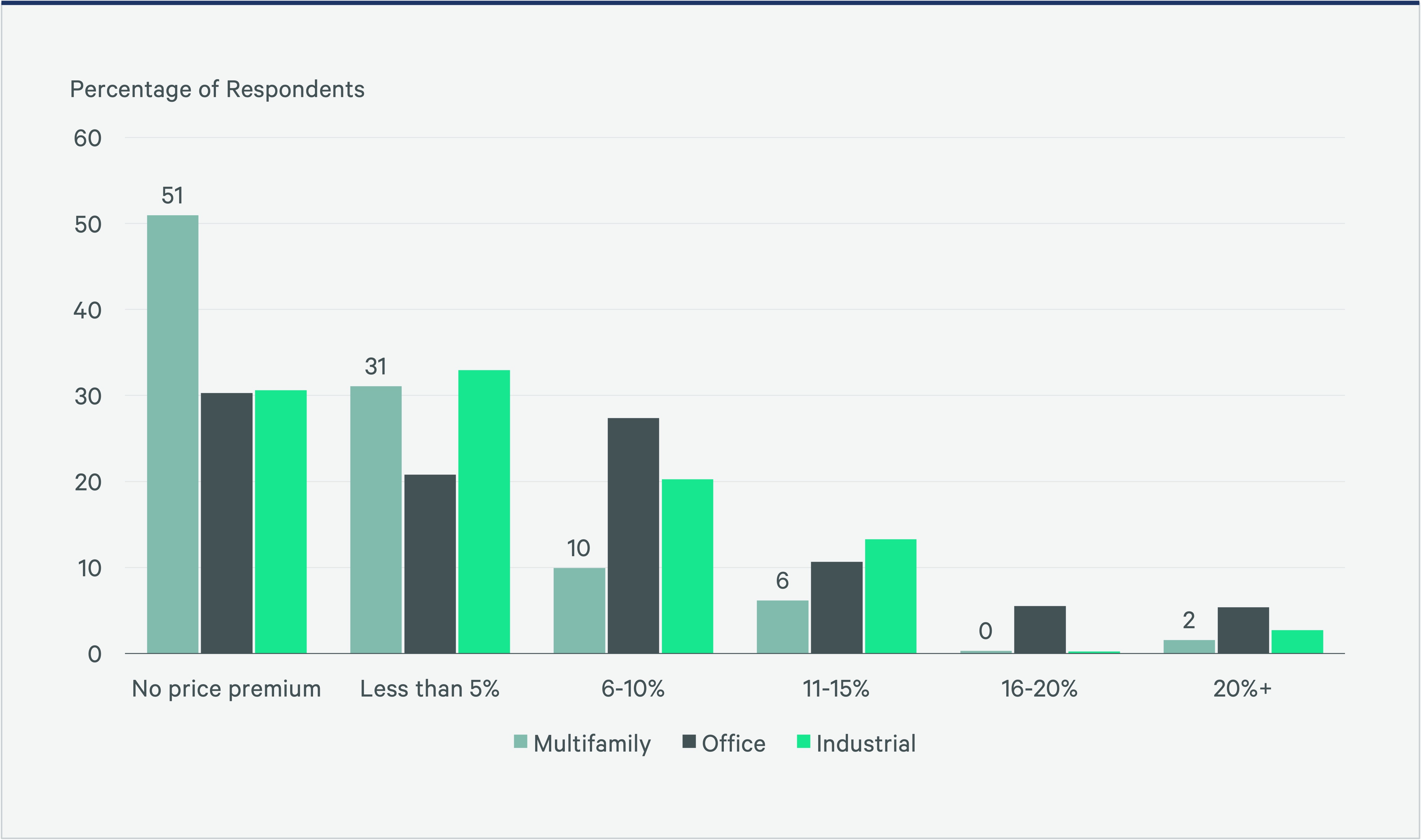

Half of Multifamily Investors Offer No Price Premium for ESG Assets

Over half of multifamily investors said they would offer no price premium for ESG-compliant assets, compared with 30% of office and industrial investors. Thirty-one percent of multifamily investors said they would offer a premium of less than 5% for ESG-compliant assets, while 18% said they would offer a premium of more than 5%. Forty-nine percent of office investors and 36% of industrial investors said they would offer premiums of more than 5% for such assets.

Figure 12: What if any price premium would you offer for ESG-compliant assets?

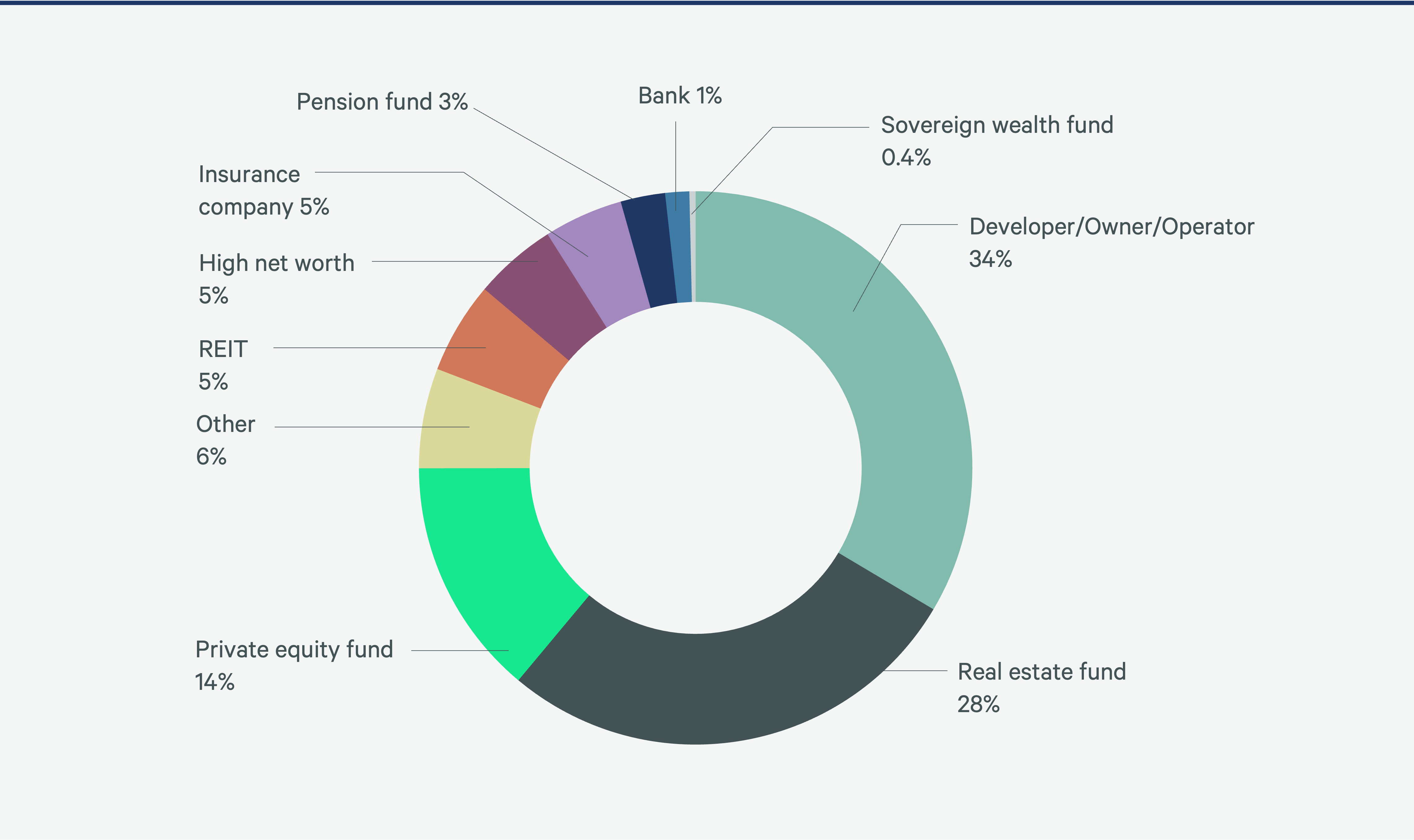

Who Took Part in Our Survey

CBRE’s 2023 Global Multifamily Investor Intentions Survey was derived from our regional surveys that included 1,200+ commercial real estate investors worldwide, over 500 of whom specified the residential/multifamily sector as their primary target. The surveys were conducted in late 2023.

Figure 13: Percentage of Survey Respondent Types

Figure 14: Percentage of Respondents by AUM

Related Insights

-

.jpg)

CBRE's 2024 European Investor Intentions Survey was conducted between November 6, 2023, and November 30, 2023.

-

Investors cited higher-for-longer interest rates, tight credit conditions and differing buyer and seller expectations as the biggest impediments to commercial real estate investment activity in 2024.

-

CBRE’s 2024 Asia Pacific Investor Intentions Survey was conducted in November and December 2023. Over 500 responses were received from participants who were asked a range of questions related to their buying intentions, perceived challenges and preferred strategies, sectors and markets for the coming year.

Related Services

- Invest, Finance & Value

Capital Markets

Gain proactive insights and strategies that unlock value, drive returns and enhance outcomes for your real estat...

- Property Type

Multifamily

Unlock the potential of your residential real estate with expert investment, financing, valuation, due diligence, design, management and leasing strat...