Intelligent Investment

Warehouse & Distribution Construction Cost Trends 2023-2024

March 15, 2024 10 Minute Read

Introduction

Construction costs have soared since the beginning of the pandemic due to multiple factors. Supply chain disruption caused materials shortages and price spikes, while a historically tight labor market drove up construction wages. Simultaneously, an unprecedented spike in U.S. construction activity, especially in the industrial and logistics sector, increased demand pressure on contractors, materials and the workforce.

The pandemic also accelerated many key warehouse and distribution demand trends that predate it. The rise of e-commerce and the need for supply-chain resiliency spurred a race for more warehouse space among major occupiers, motivating developers to build more than ever. This immense demand drove industrial construction costs higher than other commercial types, especially for modern warehouse and distribution facilities. As prices rose across the economy, the pace of warehouse construction cost inflation has been approximately 2.5 times the rate of CPI growth since 2019.

Given these trends, CBRE Project Management (CBRE PJM) and CBRE Strategic Investment Consulting (CSIC) partnered to study and present the warehouse sector’s unique construction cost and supply chain challenges.

For deeper insight, CBRE PJM conducted a survey of 19 major warehouse construction contractors across 15 major U.S. markets. Survey respondents provided a sample budget of a typical, hypothetical warehouse project across four time periods. Participants were also asked to provide estimated lead times for key materials during these time periods. CBRE PJM and CSIC analyzed more than 60 responses to provide novel insights about the warehouse construction sector.

This report’s Appendix outlines the drivers of increased industrial construction demand and cost inflation in more detail, using public data as well as proprietary and third-party sources.

Figure 1: Map of Locations Surveyed and Analyzed

Key Takeaways & Guidance

-

Price estimates vary among contractors and price uncertainty remains.

Contractor price estimates on the cost of industrial construction varied heavily, even within a single market and across material categories, despite providing detailed assumptions. This may indicate some uncertainty that persists in the construction sector. -

Pandemic-driven cost spikes affected all markets, but unevenly.

Markets were affected differently by pandemic-driven cost spikes. There are natural market-to-market price differences due to local competitive advantages during periods of market equilibrium. But every market experiences cost increases during major supply chain instability, which tended to impact lower-cost markets more. -

Moderating costs in certain categories appear on the horizon, but sentiment is mixed.

On average, contractors noted costs have been virtually flat since 2022. However, this varies dramatically by market. Some recent budget estimates noted over 10% cost increases, while others noted significant decreases. Contractors’ 2024 budget outlooks were more aligned at an average 2% to 4% cost increase. However, contractors in a few markets project further decreases. -

Lead times for key materials have generally improved and are unlikely to worsen in the near-term.

Normal pre-pandemic lead times for most materials ranged from 6 to 12 weeks, then rose to 12 to 33 weeks as demand spiked and supply chains were disrupted. Lead times for most materials have normalized, which is expected to continue. But lead times for key categories like electrical equipment and HVAC remain two to three times their pre-pandemic timeframe, with little improvement expected this year. -

Early involvement from experienced professionals is important in this uncertain time.

Given the general construction costs uncertainty this year, underscored by the wide price range cited throughout this report, experienced and connected project management professionals are more important than ever to help ensure optimal timeliness and pricing.

Cost Survey Results

Price Estimates Vary Among Contractors and Price Uncertainty Remains

Cost estimates for both price per sq. ft. and escalation rate varied, even within a single market.

Cost estimates from Chicago-based contractors demonstrate how much pricing and escalation rate variance is possible (Figure 2). Pre-pandemic price estimates were less varied, except for Budget 1. There was similar variation during the pandemic’s peak, with some disparity in how the prices changed. Price estimates diverged further in 2023 and varied most for 2024.

This example demonstrates how contractors may have interpreted the specifications differently, but also how differently contractors experienced the market over the past several years. This underscores the importance of working with experienced and skilled project management professionals to help ensure the lowest budget cost.

The following pages show aggregated cost data for the U.S. and the 15 markets in this study, so it is important to note the broad variance underlying these reported averages.

Figure 2: Budget Examples from Chicago-Area Contractors

Source: Various Contractors, CBRE PJM, CBRE Strategic Investment Consulting, Data as of Q3 2023.

Industrial Construction Cost Inflation Has Generally Settled From Its Peak

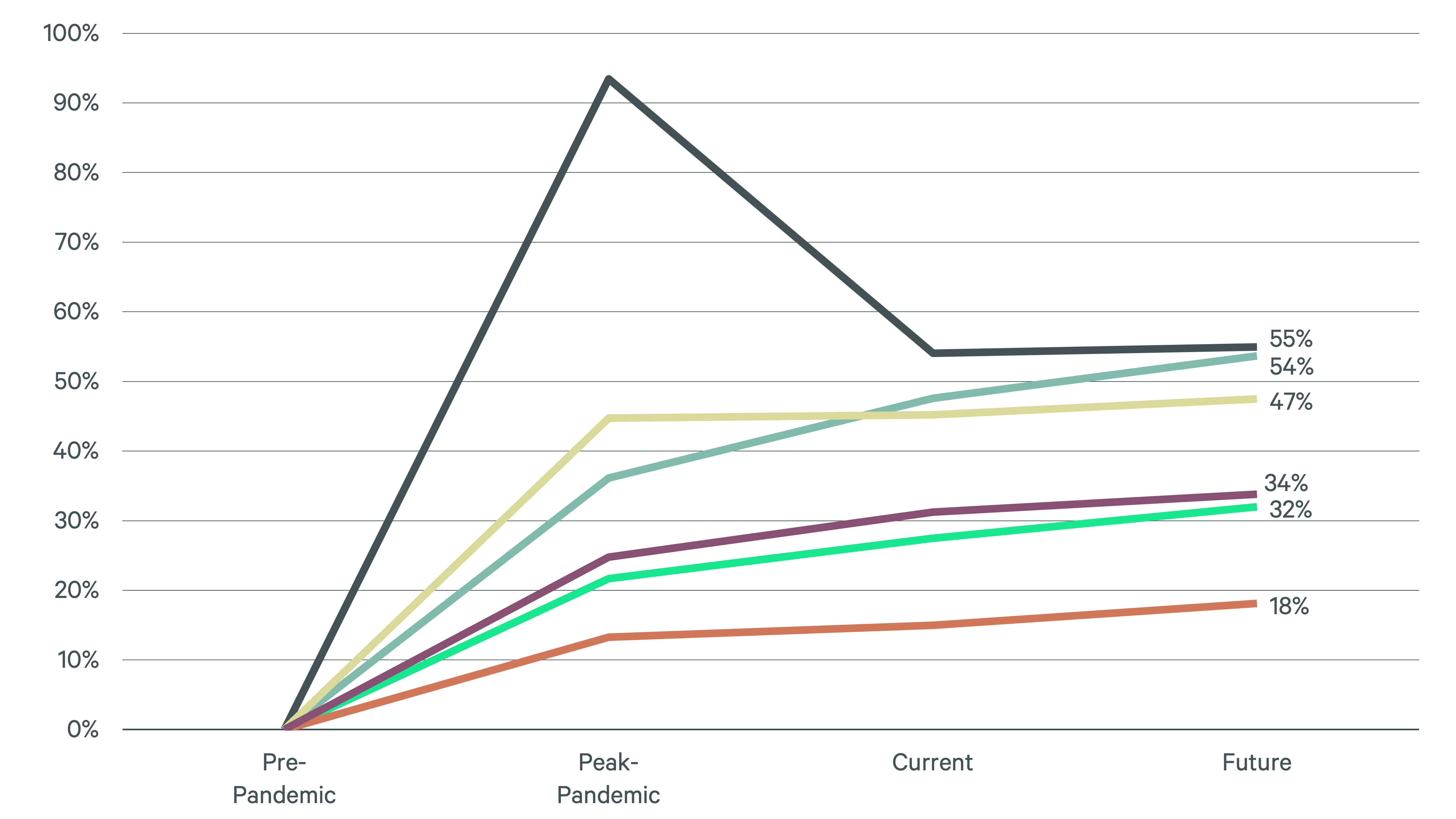

In aggregate, CBRE PJM’s contractor survey respondents reported total industrial construction costs increased 38% from the pre- to peak-pandemic. They reported virtually unchanged costs from the peak-pandemic to the current period, and a 2.6% increase from the current to future period.

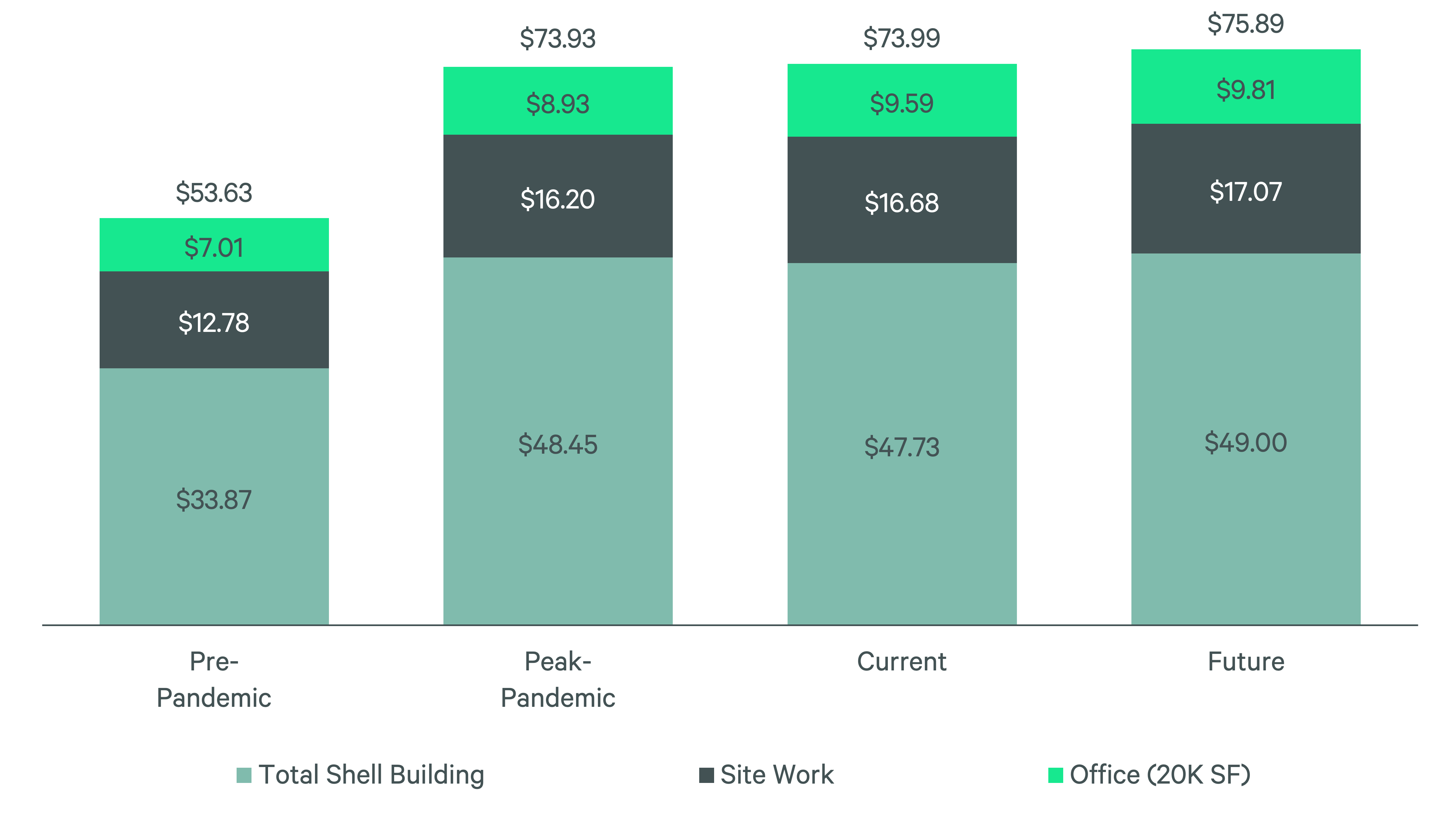

Building shell makes up about 65% of the total construction cost, site work accounts for 23% and office TIs account for about 13%.

Building shell structure construction, site work and office TIs each sharply increased in cost from the pre- to peak-pandemic. Shell costs increased by 43% over this period, the biggest increase. This was due to the price volatility of specific materials required for shell construction, such as large amounts of concrete and steel (Figure 6). Site utilities, asphalt paving and landscaping/irrigation were the primary drivers of cost increases of site work during the peak-pandemic. Office TI costs have been rising more quickly since the peak-pandemic because HVAC and electrical equipment can be a large share of office build-outs.

Figure 3: Industrial Construction Costs by Major Category & Time Period

Figure 4: Cumulative Rate of Industrial Construction Cost Increases Since 2019

Industrial Construction Costs Spiked More Than Other Commercial Types Because of Its Highly Concentrated Materials Mix

Structural steel and carpentry as well as concrete and precast/tilt make up more than half of the shell cost. Each had higher price spikes during the peak-pandemic, along with roofing costs.

Most other commercial construction has less cost concentration in a few core materials, decreasing overall price volatility compared to industrial construction.

Since the peak-pandemic, most contractors reported that steel prices decreased. They also reported concrete and precast/tilt costs increased by 8%—the sharpest increase of any material category over this period. Mechanical, electrical, plumbing and fire protection (MEP/FP) was up 5% during this period.

Looking ahead, contractors expect shell costs to increase by 3% from the current to future period. Concrete and precast/tilt as well as MEP/FP are the two material categories expected to drive this increase, with both expected to rise by 4% over this period.

Figure 5: Industrial Shell Budget Components, U.S. Average as of Q3 2023

Note: Steel and carpentry were combined into one category because the use of steel in warehouse construction varies across U.S. regions. For example, Western respondents allocated less budget for steel because panelized wood is more commonly used there.

Figure 6: Cumulative Rate of Industrial Shell Construction Cost Increases Since 2019

Industrial Project Costs Per Sq. Ft. Can Vary Dramatically by Region and Market

Costs for shell materials and site work tend to be lower in the Sun Belt.

Shell cost differences generally had the biggest impact on construction cost variation across markets. Markets furthest from the major U.S. steel-importing ports (i.e., Houston, Mobile, AL, New Orleans and Los Angeles/Long Beach) tended to have higher steel costs, likely due to transportation costs during a period of higher freight prices. Concrete prices were lowest in the South and Midwest, which sharply lowers industrial development costs in these markets. In contrast, concrete and precast/tilt costs spiked dramatically in Seattle due to a prolonged strike impacting regional concrete producers. This caused major shortages in this market and rationalizes a large part of Seattle’s outlier pricing displayed in Figures 7 and 8.

Site work cost estimates also varied by market, generally due to labor and service cost differences. Secondarily, materials and topography costs are major factors. Site concrete and asphalt paving accounted for about one-third of site work costs. Their pricing was variable but highest in Houston, Dallas-Ft. Worth, Phoenix and Philadelphia. Topsoil, earthwork, grading and excavation averaged about a quarter of site work costs, tending to be higher in the South and Northeast. Site utilities were also a key factor in sitework costs and were much higher in the Northeast. Even within each market, site work estimates varied more than most materials, so market-wide estimates for site work are less likely to reflect individual estimates in any market.

Figure 7: Price Per Sq. Ft. Estimate of a 500,000-Sq.-Ft. Warehouse Built in August 2023 (Select Major Markets)

Source: Various Contractors, CBRE PJM, CBRE Strategic Investment Consulting, Data as of Q3 2023.

Figure 8: Price Per Sq. Ft. Breakdown of Total Shell of a 500,000-Sq.-Ft. Warehouse Built in August 2023 (Select Major Markets)

Source: Various Contractors, CBRE PJM, CBRE Strategic Investment Consulting, Data as of Q3 2023.

Pandemic-driven Cost Spikes Affected All Markets, but Unevenly

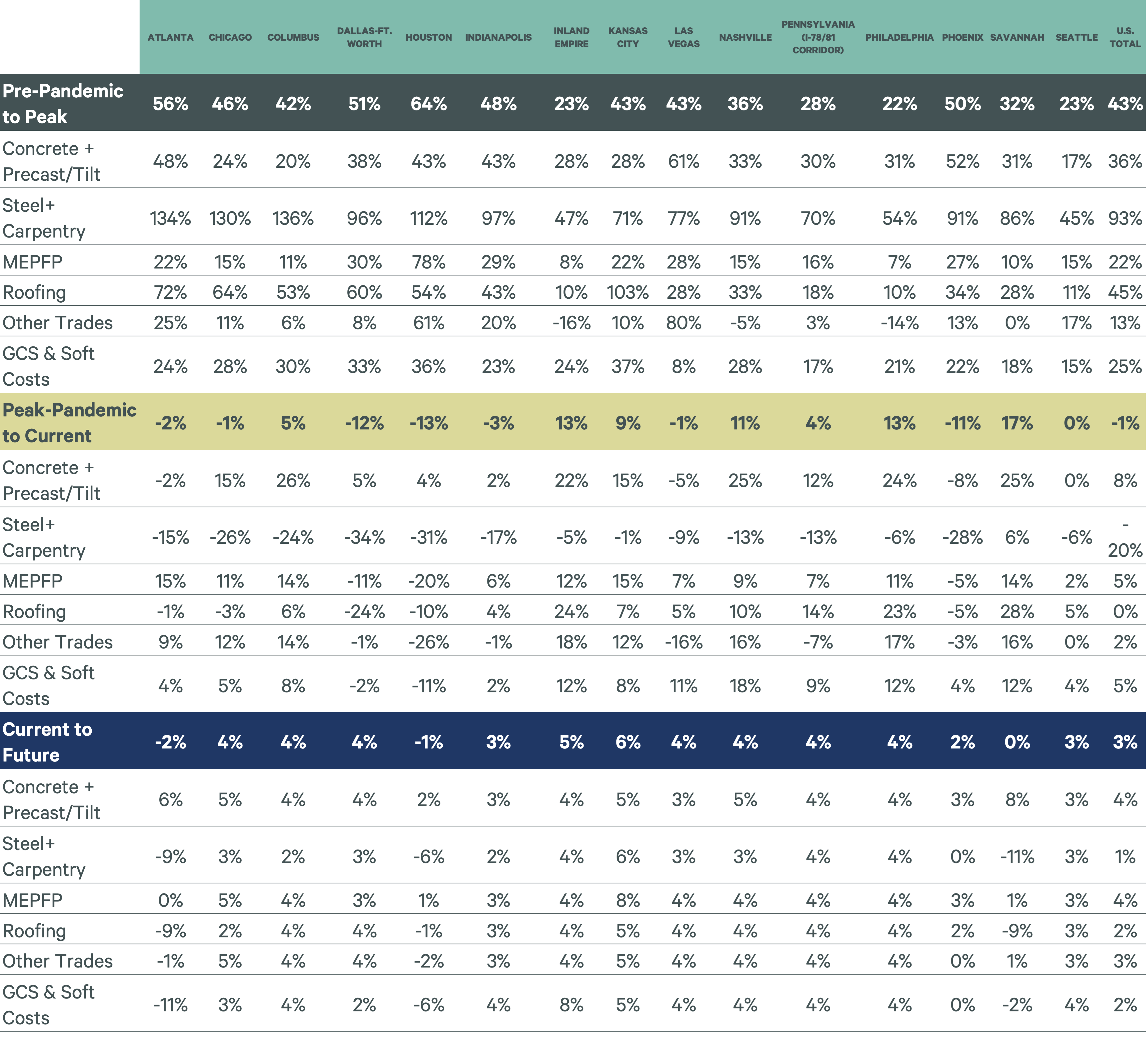

Markets in the Midwest and Sun Belt were more likely to have outlier price increases for key shell materials like concrete, steel and roofing.

Every market with an above-average total cost increase from the pre- to peak-pandemic had this in common: at least one key material had an above-average cost increase, but higher cost spikes were also a consequence of starting with a lower cost base. There are natural market-to-market price differences due to local competitive advantages during periods of market equilibrium, but every market experiences cost increases during major supply chain instability.

Savannah, GA, Nashville, TN, Columbus, OH, the Inland Empire, CA and Philadelphia experienced below-average inflation from the pre- to peak-pandemic, but these markets’ costs increased above average from then to the current period (Figure 9). This has primarily been due to rising concrete and precast/tilt costs in these markets, up almost double the national average over this time period.

Costs have declined since the peak-pandemic in most of the highest-inflation markets. Additionally, contractors in Houston and Atlanta expect further cost declines this year. Most other markets are projected to see costs rise by less than 5% this year, which more closely resemble pre-pandemic inflation rates. Figure 10 breaks down price changes by shell building material category.

Figure 9: Change in Cost Per Sq. Ft. of an Industrial Construction Project by Time Period

Source: Various Contractors, CBRE PJM, CBRE Strategic Investment Consulting, Data as of Q3 2023

Figure 10: Shell Construction Components Cost Changes of a 500,000-Sq.-Ft. Warehouse (Select Major Markets)

Source: Various Contractors, CBRE PJM, CBRE Strategic Investment Consulting, Data as of Q3 2023.

Lead Times for Key Materials Have Generally Improved and Are Unlikely to Worsen in the Near-term

Average materials lead times increased by two to three times during the peak-pandemic.

Normal pre-pandemic lead times ranged from 6 to 12 weeks for most materials. As demand spiked and supply chains were disrupted, most materials’ lead times ranged from 12 to 33 weeks. Lead times for thermal and moisture protection (which includes roofing) increased the most during the pandemic but are nearing their pre-pandemic norm. Respondents from Atlanta and Savannah, GA noted the highest spike in lead times in this category, but also reported improved timeframes through the current period.

Lead times for other hard-hit materials like electrical equipment and HVAC have improved from their pandemic peak but remain at two to three times their pre-pandemic timeframe. Little improvement is expected this year. Central U.S. markets like Dallas, Indianapolis, IN and Kansas City, MO are currently experiencing the highest lead times for these materials, while Chicago and the Inland Empire have lead times closer to their pre-pandemic norm.

Overall, materials lead times are mostly expected to stay the same or improve this year in all markets surveyed.

Figure 11: Median Reported Lead Time by Time Period

Methodology

CBRE PJM surveyed 19 major contractors spanning 15 U.S. markets. We solicited detailed budgets for a hypothetical warehouse/distribution facility over four different time periods.

Our primary goal was to learn the underlying price impacts unique to industrial construction across time periods and markets.

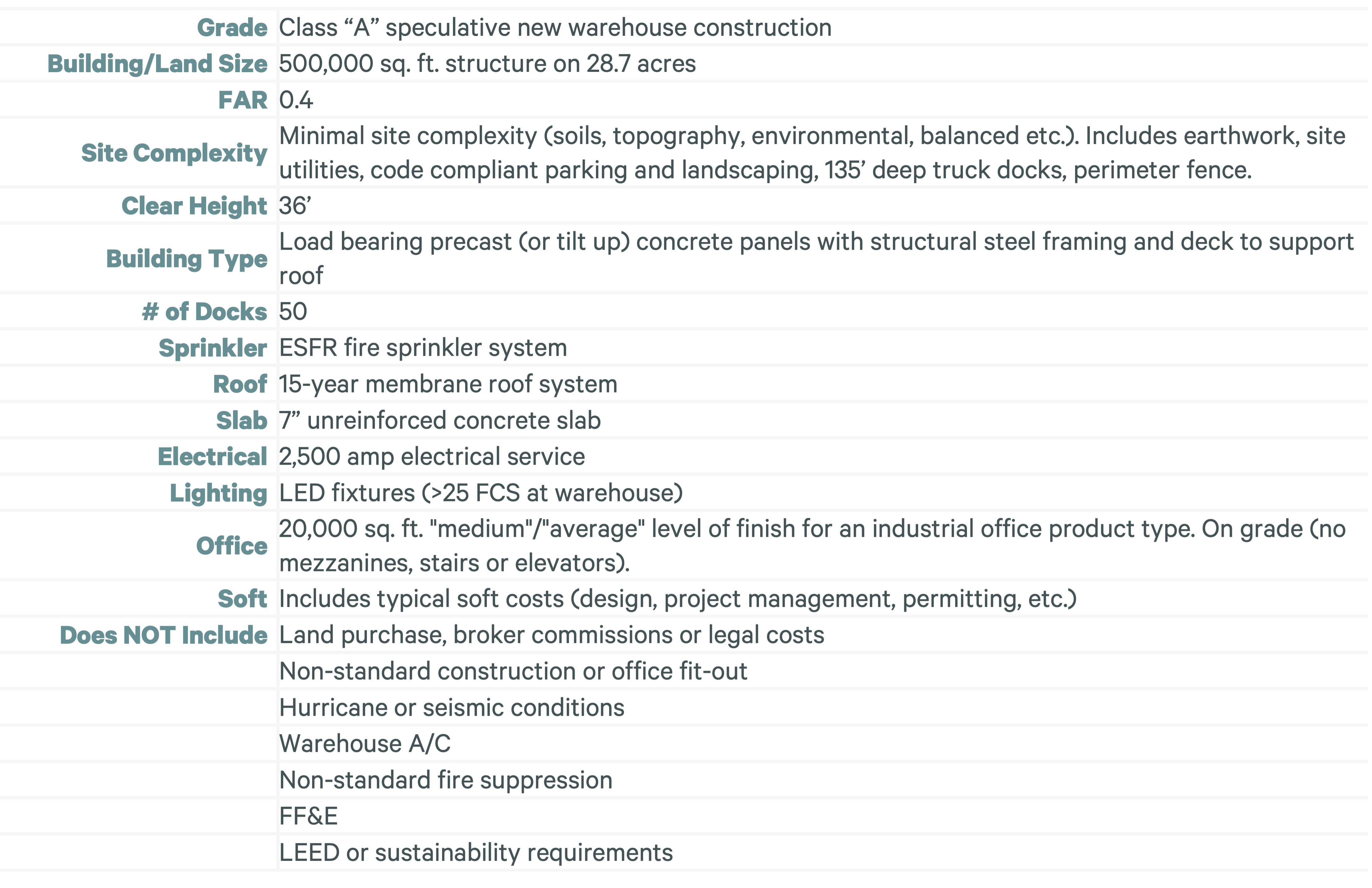

Survey participants were asked to provide detailed budget estimates for site work, shell and office tenant improvements (TI), including important material categories. Participants were instructed to assume the project is a 500,000-sq. ft. Class A spec warehouse (Figure 12) for comparable responses across contractors and markets.

Project estimate time periods used in this report:

- Pre-pandemic: 2019

- Peak-pandemic: 2020-2022 (actual date will vary by respondent and market)

- Current: Q3 2023

- Future: Q3 2024

Respondents were asked to base budget values on a "lowest expectation of cost," meaning project costs would not be less than what is reported. Some outlier cost per sq. ft. responses were adjusted up or down to better reflect market averages and align more with relative costs learned from other sources (including proprietary CBRE data). However, reported changes over time were left as initially reported. Due to a large variance in responses, office TI data was augmented using CBRE’s latest cost guide.

Additionally, many respondents were asked to report on multiple markets. The 15 markets were chosen based on their major size, as well as geographic variation and contractor relationships. To determine a national average, a weighted average was calculated for each market using the volume of industrial construction in the market since 2020. In total, 60 responses were used for this analysis.

Figure 12: Hypothetical Specs Provided to Survey Respondents

Plans to Provide You With Deeper Insights

In a 2024-2025 edition of the report, CBRE PJM and CBRE CSIC plan to improve the survey methods to gain better insights on how industrial construction costs are evolving. Improvements will include:

- Focus on different regional methods of construction to capture better pricing differences (i.e., steel vs. wood structure, HVAC needs, etc.).

- Seek out more detail, including more exact breakdowns for precast/tilt, HVAC methods and other areas.

- Improve alignment with existing CBRE PJM office cost reports.

- Establish a CBRE industrial cost index by market.

- Explore expanding beyond the 15 U.S. markets selected for this report.

- Target a minimum of five budgets per market to ensure adequate sampling and a more accurate central tendency.

Related Insights

-

Labor costs and hourly wages continue to rise. Increasing construction labor costs are a major challenge facing the industry.

-

The U.S. industrial market is expected to stabilize in 2024, with net absorption on par with 2023 levels and taking rent growth moderating to 8%.

-

Projects movement of the FM Cost Index across regions and includes an outlook encompassing contract, energy and labor costs, as well as cost management strategies

Related Services

- Property Type

Industrial & Logistics

We represent the largest industrial real estate platform in the world, offering an integrated suite of services for occupiers and investors.

- Design & Build

Project & Program Management

Deliver projects seamlessly with an integrated team that manages everything from schedules and budgets to the entire construction process.

Bespoke analysis to help you make confident decisions, attract more capital, enhance asset performance and drive value for your business.