Intelligent Investment

Grocers Adding More Stores to Meet Rising Consumer Demand

April 16, 2026 5 Minute Read

Executive Summary

- U.S. consumers spent more than $915 billion on groceries in 2025, up by 3% from 2024 and 21% since 2020, according to the U.S. Census Bureau.

- Shopper visits to grocery stores also increased in 2025, reflecting a growing emphasis on health and wellness and consumers’ preference for eating at home more often.

- As a result of this rising demand, grocers have announced plans to add new stores totaling almost 21 million sq. ft. this year.

Grocery Spending Will Continue to Increase

Consumer spending on groceries increased by 3% last year to nearly $1 trillion, according to the U.S. Census Bureau. Most of the country’s biggest grocery chains like Kroger, Albertsons and Publix reported same-store sales growth of between 1.5% and 3%. Mass merchants and wholesale clubs like Walmart and Costco reported even greater increases of between 5% and 6% due to more grocery offerings.

Figure 1: 2025 Same-Store Sales Growth

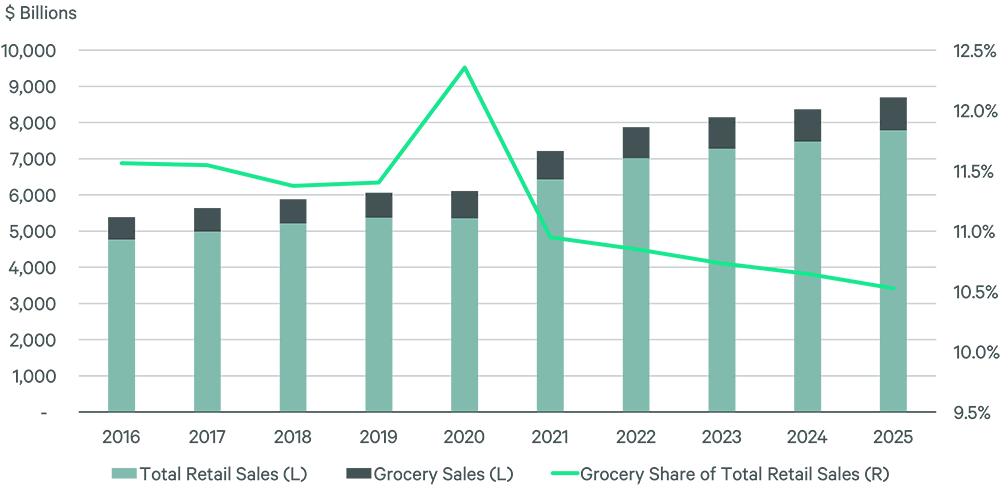

While grocery sales continue to climb, their share of overall consumer spending has declined by 1 percentage point over the past decade (Figure 2). This was likely due to pent-up demand for in-person dining experiences after the end of the COVID pandemic, as well as consumers’ general shift toward favoring services and experiences over goods.

Figure 2: Grocery's Share of Total Retail Spending

However, given lingering economic uncertainty, consumers are once again prioritizing the value offered by grocery stores. U.S. Census Bureau and National Restaurant Association data indicates that restaurant pricing has increased by nearly 60% over the past 10 years, while grocery prices rose by 30%. This has made buying and preparing food at home an appealing option for those looking to cut costs.

Physical Stores Integral to Grocery’s Success

While many grocers have increased their online fulfillment capabilities since the pandemic, physical store shopping has accounted for most of the recent sales growth. Retail consulting firm Placer.ai reports that grocery foot traffic increased across all formats last year (Figure 3). Fresh-format grocers like Whole Foods and Sprouts had the biggest increase in store visits by nearly 10%, as consumers favor alternatives to eating out. Value grocers like Trader Joe's, Aldi and Lidl all saw more shopper visits last year, highlighting consumers’ desire for low-priced options. While the broader retail industry has been focusing on higher-income consumers’ outsized spending power, grocers are seeing the greatest growth in visits coming from lower-and-middle income consumers.

Figure 3: Year-over-Year Foot Traffic Growth by Grocery Format

Many retailers are leveraging their stores as fulfillment centers for curbside and in-store pickup of online orders. Capital One reports that 85% of its customers who buy online and pick up in store (BOPIS) tend to make an additional purchase within the store itself. These BOPIS shoppers consistently show higher order values and stronger repeat behavior, driving reliable repeat store traffic.

Trade association ICSC has found that grocery-anchored retail centers attract approximately three times as many customers annually than unanchored centers in comparable trade areas. This translates to a roughly 200% increase in foot traffic and allows owners of grocery-anchored centers to command 15%-to-25%-higher rents for adjacent in-line spaces.

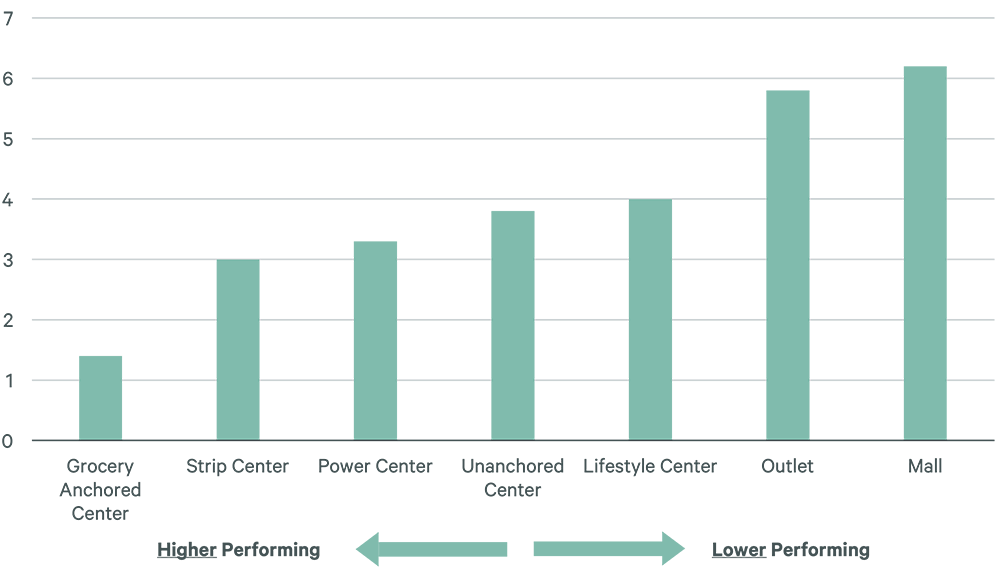

Grocery-anchored centers’ performance metrics make them extremely attractive to investors. MSCI reports that investment volume of this asset type totaled $12.8 billion last year, its largest rolling-four-quarter total since 2022. CBRE’s 2026 North American Investor Intentions Survey found that 85% of retail investors favored grocery-anchored centers, making them the most preferred retail format by a wide margin. Additionally, CBRE’s H2 2025 Cap Rate Survey found that grocery-anchored centers have the best expected investment performance of all retail asset types (Figure 4).

Figure 4: Expected Rank of Retail Property Type Investment Performance Over Next 10 Years

More Expansion to Come in 2026

Grocery retailers are poised to capitalize on strong sales growth by adding more stores this year. As many as 850 new stores will open in 2026, led by Dollar General, a discount retailer that heavily features grocery items, with 450. Among discount grocers, Aldi plans to open 180 new stores this year, while fresh-format grocers like Whole Foods and Sprouts each plan to open between 25 and 40 new locations.

Mass merchandisers and wholesale clubs will also remain key players in the grocery industry. BJ’s and Target both plan to open 30 new stores this year, while Walmart plans to cash in on population growth across the Sun Belt with 12 to 15 new locations this year, mainly in Florida and Texas.

Figure 5: 2026 Planned Grocery Store Openings

Grocery remains one of the few retail categories that deliver both resilience and growth, making it increasingly critical for retail owners to understand the nuances of the sector. Grocery spending growth is driving demand for more grocery stores that generate greater foot traffic and enable landlords to command higher rents from adjacent tenants.

Related Insights

-

Podcast | Intelligent Investment

What’s in Store: Retail Real Estate’s Investment Outlook

April 7, 2026

Retail real estate has emerged as an increasingly attractive asset class. LBX Investment’s Phil Block and CBRE’s Chris DeCouflé discuss the strategies driving today's returns and where the smart money is headed.

-

U.S. cap rates show signs of stabilization, with improving liquidity, firmer pricing and growing confidence that yields are past their peak.

-

Nearly three quarters of commercial real estate investors plan to buy more assets in 2026 as prices stabilize and fundamentals improve.

-

Despite uncertainty, growth will continue for the U.S. commercial real estate market in 2026.