Market Intelligence

Middle East Conflict Reshapes Global Gas Market Dynamics

March 24, 2026 5 Minute Read

Executive Summary

The conflict in the Middle East shut down Qatar's Ras Laffan liquified natural gas (LNG) facility, the world's largest, and has effectively prevented safe passage through the Strait of Hormuz to tanker traffic, taking roughly 20% of global LNG supply off the market. The disruption coincides with the start of Europe's gas storage injection season, when countries build up their inventories ahead of the winter. European storage stands at about 30% of capacity as of March 2026, its lowest seasonal level since the winter (2021/22) before Russia's invasion of Ukraine.

A global supply shortfall will likely keep global gas and power prices elevated while the conflict lasts, forcing buyers to choose between locking in long-term power and gas contracts at high prices or remain exposed to further spot market volatility.

A quick resolution of the Middle East conflict could see European and Asian gas prices for near-term delivery retrace below longer-dated contracts. Buyers anticipating a short-lived disruption can avoid locking in summer and winter future prices now, which would also fall in such a scenario. For those that expect a persistent supply disruption, the backwardation in current forward curves could offer a window to hedge summer and winter supply below today's front-month prices. This option might narrow if the conflict persists and the curve flattens upward.

Figure 1) Global Forward Gas Contracts, by Delivery Date as of March 13, 2026

Macro Scenario Assessment

Market Trends to Watch

The Supply Disruption

Qatar's Ras Laffan complex, the world's largest LNG facility, shut down after military strikes in late February. The simultaneous constraints at the Strait of Hormuz has taken roughly 20% of global LNG supply off the market. On-site gas storage at Qatari and United Arab Emirates (UAE) facilities can buffer roughly one week of output. Beyond that, large-scale liquefaction shut-ins become unavoidable. The full extent of infrastructure damage remains unclear, and the longer the conflict continues, the greater the risk of lasting disruption to global gas supply.

Key Highlights

- No immediate substitute for Qatari LNG likely exists in the market, as other LNG export terminals are running near full capacity and Europe's pipeline suppliers have limited headroom to increase flows.

- Replacement options for Qatari LNG might be more constrained than in 2022, when U.S. LNG terminals still had spare capacity to ramp up exports to Europe and Russian gas limited by international sanctions.

- European buyers are competing for available U.S. LNG cargos with Asian importers that are likely willing to pay much higher premiums given their outsized reliance on Qatari LNG.

The disruption in global gas flows also coincides with the start of Europe's gas storage injection season. EU storage stands at approximately 30% of capacity, its lowest seasonal level since the winter before Russia's invasion of Ukraine.

European countries face a decision as they begin refilling gas storage ahead of winter 2026/27. Buying now likely locks in elevated prices in a severely undersupplied global market. Waiting could risk even higher costs if the conflict persists but would pay off if the disruption is short-lived and prices retrace. EU regulation requires storage to reach at least 80% by November 1. With inventories starting below 30%, the narrow refilling window and substantial volumes required likely limits the time available to delay procurement decisions.

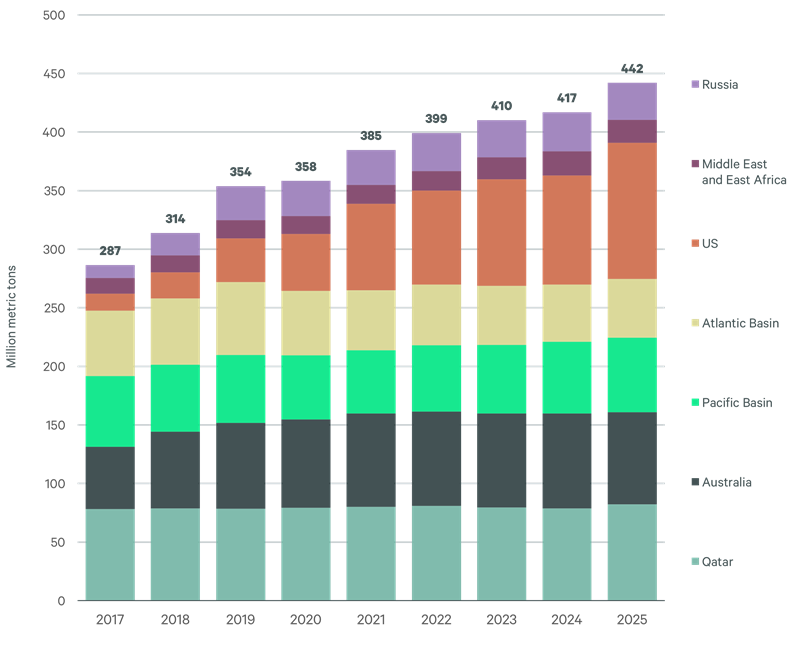

Figure 2) Global LNG Exports by Region

Global Gas Markets Reaction

Gas Importers: Europe and Asia Pacific

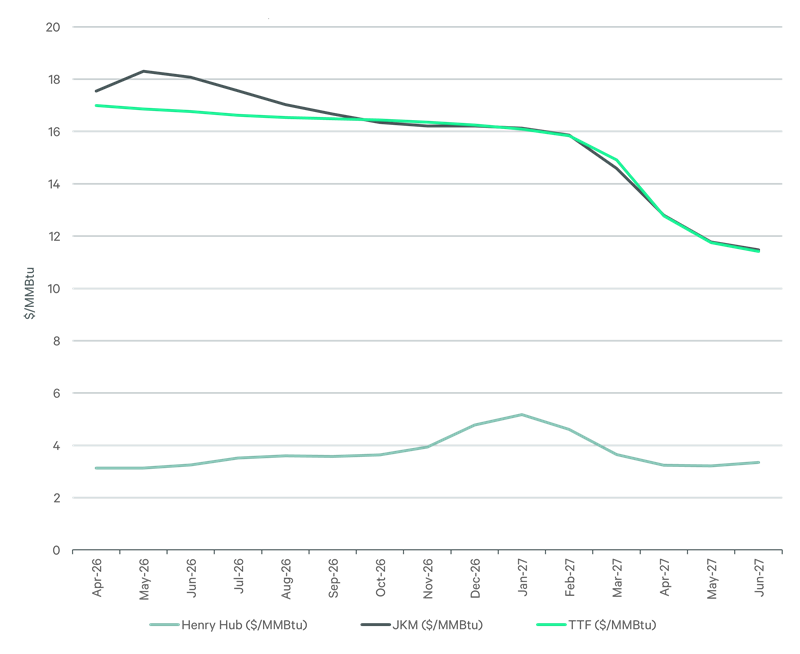

Europe's benchmark Title Transfer Facility (TTF) and Asia's Japan Korea Marker (JKM) gas forward curves remain in steep backwardation, where near-term prices exceed longer-dated forward contract prices. As of March 13, this signals markets expect the disruption to last weeks, not months. Prolonged constraints at the Strait of Hormuz would shift the price rally from near-term delivery contracts into the full summer and winter forward contracts.

Europe is now likely more resilient to gas shocks than during the 2022 energy crisis. U.S. LNG exports have more than doubled since 2020, improving the global gas supply mix. Power demand has also fallen by about 5% below 2021–22 levels, and solar and wind now account for 34% of annual power supply, up from 24% in 2021. However, gas still sets the marginal power price in most European markets, and April delivery prices across gas-heavy markets, such as Germany, the U.K. and Italy, are already up an average 23% as of early March. Italy, Europe's most exposed market to Qatari LNG, saw month-ahead around-the-clock power prices rise 46% to €135/MWh in early March.

Key Highlights

- As of March 13, TTF front-month futures have jumped 56% to €51/MWh compared with a month ago, but that's still well below the €311/MWh price reached during the 2022 energy crisis.

- The U.K.'s National Balancing Point (NBP) futures have risen by nearly 70% to over £44/MWh (€51/MWh), also well below the 2022 highs of £218/MWh (€259/MWh).

- Asia receives roughly 80% of Qatari LNG exports, making it the most exposed region to the supply loss. Europe buys less than 10% but competes with Asian buyers for the same pool of replacement cargoes.

- Asian spot LNG prices more than doubled in the first week of the conflict, with JKM benchmark prices reaching $25/MMBtu, its highest level since prices hit $68/MMBtu in 2022.

- The JKM-TTF spread rose to near $7/MMBtu after passage through Strait of Hormuz was constrained, pulling flexible LNG cargos away from Europe and into Asian markets.

Figure 3) Asia JKM LNG vs Europe TTF Natural Gas Front-Month Forward Prices ($/MMBtu)

United States

U.S. LNG export margins to Europe and Asia nearly doubled between February 27 and March 10 as the gap between Henry Hub and international benchmarks widened. This price premium will likely incentivize U.S. LNG facility operators to defer scheduled maintenance and maximize output. If the conflict persists and longer-dated European and Asian gas forwards rise above near-term prices, LNG operators would have a sustained incentive to maximize output, tightening domestic gas storage heading into winter 2026/27.

U.S. gas storage was below seasonal norms when the conflict began, but still tracking just above last gas year's levels spanning from November through October. Winter Storm Fern in late January triggered a record single-week storage withdrawal of 360 billion cubic feet (Bcf), pushing Henry Hub spot prices to an all-time high of $30.72/MMBtu. Prices have since normalized. Henry Hub front-month prices are trading at $3.3/MMBtu as of March 13, up 18% since the conflict began, but still in the range seen in early February.

If storage levels trail last year's heading into summer, forward gas and power prices could remain high through winter 2026/27, particularly as industry estimates of growing AI data center demand add a structural floor under U.S. gas consumption.

Figure 4) U.S Total Gas Storage Levels by Gas Year (November through October)

Energy Solutions

Accelerate your decarbonization efforts by transitioning to clean energy sources.