Report

Impact of hybrid working on office vacancy manageable thanks to flexibility of Dutch offices market

Polarisation is compelling owners to engage in more active asset management and increase their investments in ESG and flexibility

October 27, 2023

Executive summary - hybrid work

Looking for a PDF of this content?

More than three years ago, Dutch people working in offices were suddenly forced to work from home because of the COVID-19 pandemic. With hindsight, we can now see that this unforgettable situation was a game changer: hybrid working is here to stay. But exactly what impact has this change in behaviour had on future demand for offices? What risks does investing in offices currently involve and what can owners do to prevent an increase in vacancy?

Striking the right hybrid balance

Some 65% of the Dutch office workers now work more from home than in 2019. Despite this, employers and employees have yet to strike the right hybrid balance. As a result, the average number of days of working from home has fallen since the end of 2020: from 2 to 1.3 days per week. And these days are not spread evenly across the week. This is resulting in unbalanced occupancy levels at work, making it difficult to determine accommodation needs. A more effective spread is proving hard to achieve in practice.

Office vacancy rate still largely unaffected by hybrid working

If we consider the trend in the vacancy rate between the end of 2019 and now, we can see a significant decline in almost all Dutch office regions. Hybrid working has so far affected the vacancy rate only slightly, but research by CBRE shows that this is up until now almost completely compensated by companies that are expanding and increasing their need for office space.

Impact of hybrid working in the Netherlands cannot be compared to situation in the US

In the Netherlands, the vacancy rate is in a declining trend, but it is seeing a significant increase in the United States and some European countries. This is largely due to the desk-per-employee ratio in these countries, which was considerably higher than in the Netherlands before the pandemic. Whereas we have had an average of 0.6 to 0.7 desks per employee for years, the Americans have a ratio of 82%. Internationally, this desk ratio is expected to be between 50% and 55% in the future.

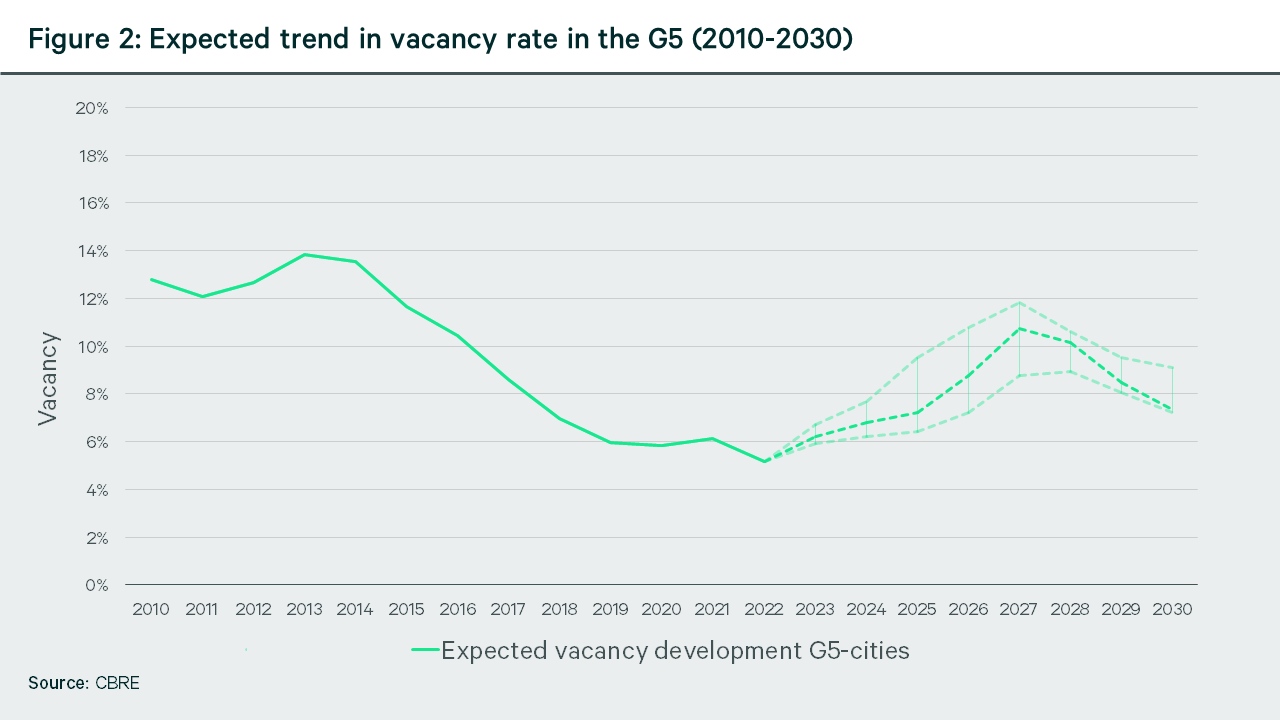

Demand for offices set to decline by 8.7% in the long term as vacancy rate rises

Despite this, hybrid working will ultimately gain a grip on the offices market and the amount of office space required per employee will decline as a result – albeit less so in the Netherlands compared to other countries. Based on our models, we expect to see demand for office accommodation in the G5 decline by -8.7% by 2030. Between 2027 and 2028, that will result in a peak in the vacancy rate of approximately 10.7% – significantly more than the current figure of 5.5% in the G5. After that, the vacancy rate will gradually decline again, partly in the wake of a second – and smaller – wave of office transformations.

Polarisation in the offices market as a result of rising vacancy rate

The vacancy rate is expected to increase more in secondary locations focused on highways. Our data analyses show that the return to the office here is around 5% lower than it is at central and multimodal locations. This may cause organisations in secondary areas to give up more office space when renewing their contracts. In addition, increasing numbers of relocating companies are opting for offices that are easily accessible by public transport: this reduces emissions and is a better match in view of their reporting obligations under the Corporate Sustainability Reporting Directive (CSRD) and their quest for talent.

The polarisation in the offices market presents challenges for policymakers. They will need to offer more space for offices around stations while also attempting to prevent additional vacancy at secondary locations by means of transformations.

Battle for tenants initiated, flexibility and ESG the key weapons

The competition for tenants is increasing in the Dutch offices market. Ultimately, it is the relative quality of an office that determines where organisations opt to set up business for the long term. Key criteria include flexibility and sustainability.

Our Global Occupier Sentiment Survey reveals that the demand for flexible office spaces is set to increase by around 55% in the next two years: this makes it easier for organisations to accommodate peaks in occupancy. Owners have an opportunity to capitalise on this, for example by offering additional flexible meeting rooms. Whereas in the past, the ratio between individual and shared working space was 70-30, this is predicted to shift to 40-60 in the years ahead. The increasing demand for rooms for collaboration and teamwork is expected to be met in part by flexible spaces available for rent in the building.

In addition, building owners can make a difference by means of sustainability and ESG. We are already seeing organisations choose offices that match their ESG ambitions. Shortages could result in significant rent increases in this office segment compared to other offices. CBRE expects to see a further increase in this price differential: demand for net zero offices is outpacing supply as a result of companies’ ESG ambitions. Our European ESG survey reveals that 50% of the large companies questioned aim to achieve net zero emissions by 2035. For owners, this figure is just 28%. This difference will ultimately lead to higher pricing for net zero office buildings, which will also make renovations and new builds more affordable.

Hybrid working results in sustainability upgrades and more transformations?

In the first instance, hybrid working has brought about a healthier situation in the offices market. The vacancy rate is below the friction level in many regions, making company relocations difficult, especially for larger organisations.

The more expansive market conditions expected to develop in the years ahead will initially result in a diverging market when it comes to location and quality. Companies will actually have the space to opt for quality again. This will create fertile ground for renewal and profitable investments and – as demand for offices declines – create more opportunities for transformations to housing. Transformations that – in view of the ever-increasing housing shortage – will prove essential in providing every Dutch inhabitant with a place to live and a place to work from home.

Impact of hybrid working manageable thanks to flexibility of Dutch office market

Polarisation is compelling owners to engage in more active asset management and increase their investments in ESG and flexibility

It is now three years since Dutch people were forced to work from home because of the Covid-19 pandemic. It was an unforgettable situation, and we now know that it turned out to be a game changer. It changed the way we work, shop, live and spend our leisure time – but above all, it changed our work/life balance. Afterwards, when the restrictions were lifted, the combination of less time spent commuting, a better work/life balance and improved productivity at home ultimately meant that there was very little change in employees’ behaviour. It was not only employees who were eager to adopt a new, hybrid way of working. Most employers are also in favour.

Partly as a result of this, there has been much talk in recent years of the ‘demise of the office’. The Netherlands Environmental Assessment Agency even predicted that we would see fewer traffic jams. Nothing could be further from the truth. In the first six months of 2023, congestion levels were 15% higher than in 2019. Interestingly, traffic congestion rose sharply on Tuesdays and Thursdays while declining on Mondays and especially Fridays. In other words, many people are opting to work from home at the start and end of the week. But what impact has this change in behaviour actually had on long-term demand for office accommodation? And what options do you have as an owner to prevent an increase in vacancy?

Changes in working from home

Home and office working yet to reach a balance

In order to gain a clear understanding of the impact of hybrid working on the offices market, we first need to find out what the breakdown is between working from home, at the office or elsewhere. Figures published by the Dutch Ministry of Infrastructure and Water Management show that the proportion of people working from home has fallen slightly since October 2020. Between 2021 and 2022, the number of days of working from home fell by 20.2%. Most people now spend between zero and three days working from home. Until last year, many people were still working from home for four or five days a week.

The main conclusion to be drawn from this significant change would appear to be that many employees and employers are still attempting to strike the right balance between working at home and at the office. As a result, employers may find it difficult to predict future accommodation needs. The fact is that the share of working from home has seen a 65% increase compared to pre-pandemic figures. This will decline slightly in the years ahead, but levels of working from home are still expected to remain significantly above pre-2020 levels.

As already indicated, Tuesdays and Thursdays are busier days at the office, but fewer employees can be found there on Fridays. Attendance on Fridays is 57% lower than on Tuesdays. Of course, this is also due to the large number of part-time workers who take Friday off, which was also the case pre-pandemic.

These discrepancies in office attendance make it difficult to determine accommodation needs. In the past, leases for offices were often based on peak occupancy. With such significant differences between the days, a different accommodation strategy is now required. The extent to which this is possible will depend on how much freedom the employer gives to employees. If they can decide for themselves when they come to the office, this automatically results in a higher peak demand.

If employers adopt a more mandatory approach, peak occupancy falls and with it the need for office accommodation. This means that employers can introduce compulsory office days in order to spread occupancy as effectively as possible across the five working days. Alternatively, they can provide incentives for employees to come to the office on quieter days. This can be done by scheduling events, drinks receptions or team or brainstorming sessions on these days. All of this can help to reduce the volatility of day-to-day occupancy levels.

With no compulsion from employers, day-to-day occupancy is much more variable since peak occupancy is concentrated mainly on Tuesdays and Thursdays. Interestingly, in 2023, we are starting to see signs of a shift to higher occupancy levels on Wednesdays. This may be because Tuesdays and Thursdays are so busy, both on the roads and in the office. It indicates that peak occupancy is already levelling off on these days. With no compulsion, occupancy levels on Fridays are falling significantly at many companies. Taking action to prevent this is difficult. Team meetings are rarely scheduled on Fridays since many part-time workers are not working.

With or without compulsion, hybrid working is ultimately requiring a recalibration of accommodation needs in order to maximise efficient and effective work: both in terms of the number of square metres needed and the office outfitting.

Impact of hybrid working still remains limited...

... but cannot be seen in isolation from other market changes

Many companies are currently adapting their accommodation strategy in line with the new working patterns, or plan to do so. But it is interesting to note that the current vacancy rates in the offices market show virtually no increase up to now, despite the rise in hybrid working over the last three or four years. Indeed, there has actually been a slight decline in the vacancy rate in most regions. This is in marked contrast to the situation in the rest of Europe or the United States, where the vacancy rate has increased significantly.

This difference between the Netherlands on the one hand and Europe and the United States on the other can partly be explained by faster decision-making. However, the primary cause is the fact that the desk-per-employee ratio for these countries was significantly higher pre-pandemic than it was in the Netherlands. Currently this ratio is 82% in the United States. That equates to 82 desks per 100 employees. In fact, some three-quarters of corporate businesses in the United States have a desk-per-employee ratio of 100% or higher. In Western Europe, this is quite a bit lower: 67%. The ratio in the Netherlands used to be higher as well, but has declined considerably since 2010 with the introduction of ‘the New World of Work’ (’het nieuwe werken’). This has made working from home and sharing desks commonplace in the country. As a result, the Dutch government – the country’s largest office occupier – has had a desk ratio of 60% to 70% since the introduction of ‘the New World of Work’.

Looking ahead, we predict a further decline in the ratio. According to our Global Occupier Survey, the ratio is expected to end up at between 45% and 60% internationally – approximately one desk for every two employees. This will result in a reduction in the number of square metres per desk per employee.

As offices are increasingly being used for meetings and collaboration, we are actually seeing an increase in the number of square metres for rooms suitable for collaboration. Examples include conference and brainstorming rooms and rooms to make phone calls, have lunch or relax. Where 70% of the leased accommodation used to be designated for desks, this figure is set to fall still further to around 40% in the future. The remaining 60% will be used to make phone calls, work in teams and for meetings.

Expected long-term impact of hybrid working

Impact of hybrid working not fully visible for a decade

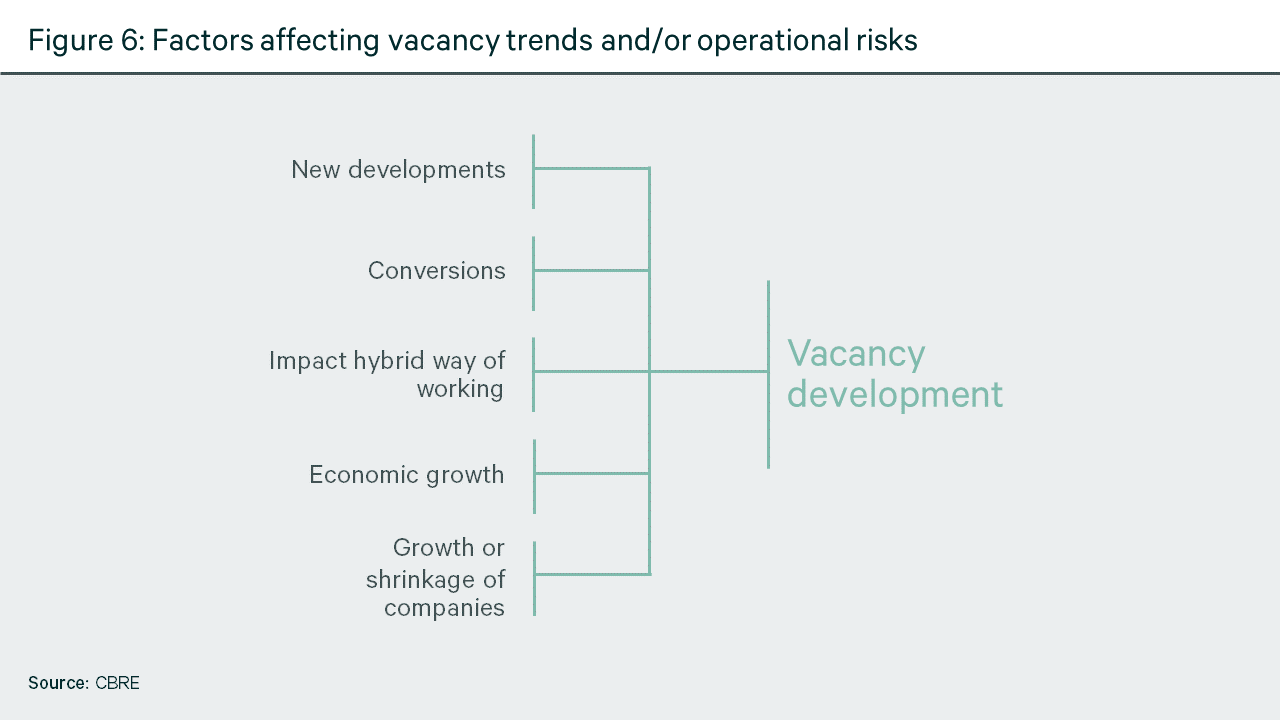

In the long term, hybrid working will result in a decline in the amount of office space required for each office worker. Despite this, the impact on the Dutch offices market will be limited compared to the rest of the world and especially the offices market in the United States. In order to effectively assess the risks of a permanent decline in demand, we need to look beyond the impact of hybrid working alone. The degree of operational risk for office owners depends on several factors: the economy, the growth or decline of companies and sectors, new builds and transformations.

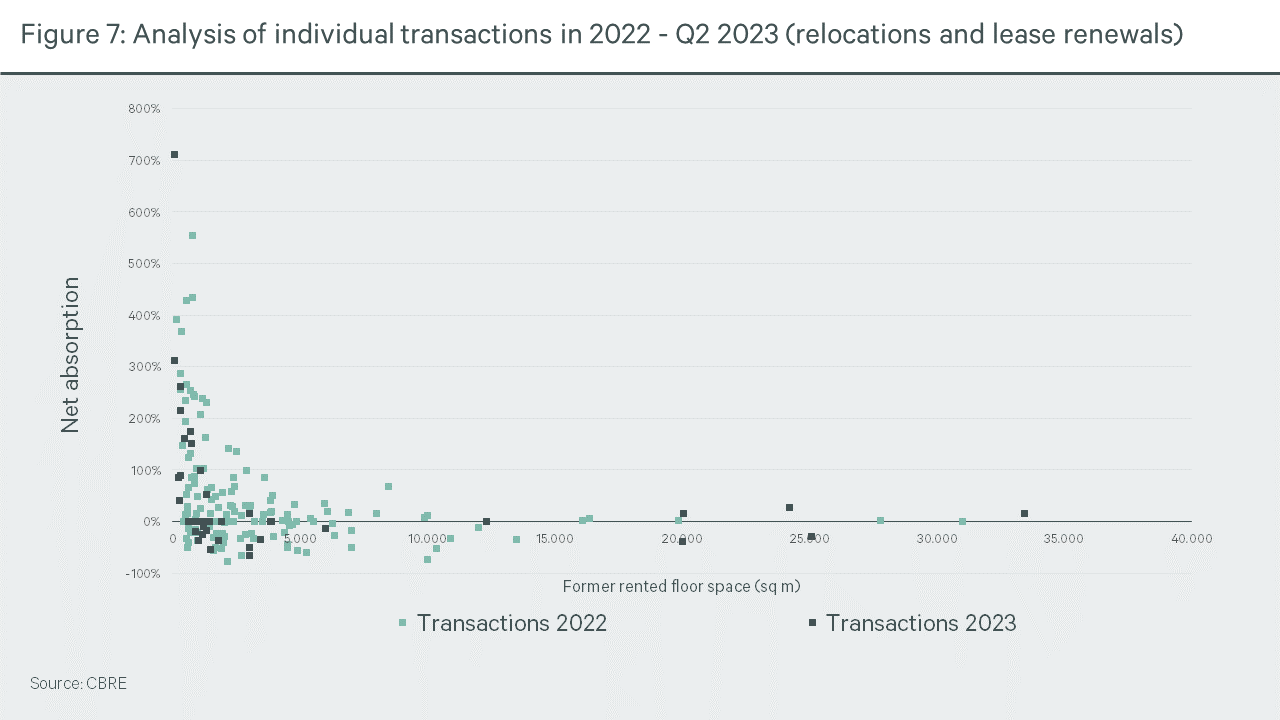

There is another issue: it is impossible to single out the effect of hybrid working statistically. The growth or decline of companies also affects the change in their demand on the offices market. An analysis of all transactions over the last 18 months makes this clear: the situation remains one of (positive) net absorption, although a slowdown is visible between 2022 and 2023. In other words, companies are still taking up more office space than they are abandoning. This goes some way to explaining the declining vacancy rates in most cities in the Netherlands.

Many decisions regarding accommodation involve a combined effect: the anticipated increase or decline in staff numbers on the one hand and hybrid working as a component of the accommodation strategy on the other. In CBRE’s experience, many companies are still resisting the urge to reduce the number of square metres despite hybrid working. They are postponing the decision and extending their leases with more or less the same floor space.

It would therefore appear that the impact of hybrid working will only result in a reassessment of demand for office space in about a decade – just as happened in the wake of the introduction of ‘the New World of Work’. Despite this, we can still conclude that hybrid working will have an impact on ongoing demand for office space. This will particularly apply to larger companies specialising in knowledge-related work. The return to the office remains an ongoing process as the behaviour of employees and employers’ policy choices continue to change. Nevertheless, CBRE is in a position to make an initial assessment of the long-term effects of hybrid working on the Dutch offices market.

Table 1: Principles for calculating the impact of hybrid working|

|

Principles |

|

Average attendance at the office |

45-55% |

|

Peak policy |

Limited compulsion to keep occupancy levels steady |

|

Number of desks per employee |

55% |

|

Growth in office work |

Oxford Economics forecast |

Demand for offices in the G5 to decline by 8.7% by 2030

Based on these principles, CBRE expects to see demand for office accommodation in the G5 decline by 8.7% by 2030. This will happen as hybrid working becomes increasingly widely integrated. However, an increase in office-related activities will likely offset the negative impact of hybrid working on demand for offices. Of course, this data will always be subject to behavioural changes. In order to make an effective assessment of the ongoing demand for offices, these models will also require annual recalibration.

So far, CBRE notes that SMEs are currently leading the trend as their employees are increasingly returning to the office and are doing so in greater numbers. The trend is much less marked in large organisations. In some cases, companies are actively engaged in encouraging more staff to return to the office. Here, average attendance of between 25% and 45% is the rule rather than the exception.

In all scenarios, the ongoing demand for office space declines and the number of square metres per FTE falls. Currently, the average in the G5 is 16.5 sq. m. per FTE. This is expected to fall to an average of 14.3 sq. m. by 2030.

The decline in demand for offices is not completely in line with the vacancy trend. A change in ongoing market demand is causing owners, project developers and local municipalities to adopt a different approach to new builds and transformations. This was seen in the recent past when the vacancy rate in the G5 rose to 14% during the financial crisis, triggering a wave of transformations shortly afterwards. Between 2010 and now, this has led to a record number of 3.2 million square metres of office space being given a new life in the G5, primarily in the residential and hotels market.

Although the vacancy rate has been below friction level (6%) for some time now, CBRE continues to see some owners opting to withdraw office space from the offices market. This is partly due to the strong demand for housing in the major cities. As a result, around 300,000 to 400,000 sq. m. of office space are set to be transformed in the G5 by 2027. The number of new additions is expected to be between 400,000 and 500,000 sq. m. over the same period. This shows that we are already seeing the market anticipating – and adapting to – a permanently lower demand for offices. Despite this, the vacancy rate in the major cities will inevitably increase in the years ahead. Vacancy is expected to peak at 10.7% between 2027 and 2028: an increase of 525 basis points compared to mid-2023. This amounts to almost a doubling of the current, very low vacancy rate.

Overall, this increase in the vacancy rate is slightly more manageable than it is in the United States and – according to expectations – in other European countries.

The fact that the vacancy rate increase is only limited is partly due to the considerable drop in value seen in the offices market over the last year. This reduces the book value of many offices, making transformation more worthwhile (in the long term) although the planned housing market regulation is also having a negative impact on this. Nevertheless, the vacancy rate is forecast to fall back to a level more in line with the friction level because more office real estate is being transformed. By 2030, we expect to see a transformation potential of around 1.6 million sq. m. in the G5. Transformations will ultimately cause the vacancy rate to decline, but will also bring about increased polarisation in the offices market in the years ahead. This may prove challenging for owners.

Assessment of market impact of hybrid working

Noticeable polarisation in the offices market

Although many owners are still currently experiencing a very low vacancy rate, this may change in the years ahead. The offices market is transforming from a landlords’ market to a tenants’ market, but this does not apply to every office or office submarket.

Although it is too early to draw any firm conclusions, the return to the office appears to be greater at central and multimodal locations than it is at secondary locations. Based on train and car mobility during rush hour, it is possible to estimate this return in various locations. This leads us to the tentative conclusion that the return to the office at secondary locations is around 5% lower than it is at central and multimodal locations. This may be due to the fact that back-office activities – work that can also be effectively done at home – often take place at secondary locations. This makes it more likely that the return of square metres will be greater in these areas in the long-term than at central and multimodal locations. This is separate from the question of how quickly any square metres freed up are put to a new use by potential new tenants.

If we look at the trends on this occupiers’ market, we are increasingly seeing a growing concentration of relocations to the same central and multimodal office locations. This is a trend that CBRE has highlighted on numerous occasions in the past. However, it is now easier to substantiate, in view of the CSRD requirements, working from home and the ongoing quest for talent.

This preference for multimodal offices is expected to bring about a polarisation in the offices market, especially in combination with the lower return to the office at secondary locations. CBRE expects to see the vacancy rate at less accessible locations in the G5 increase faster and also stay high for longer. After all, these locations are more difficult to transform. The vacancy rate of easily accessible locations will also increase, but to a lesser extent and for a shorter period.

This increasing polarisation will present policy challenges. The vacancy rate will rise in our five largest cities, but at the same time the necessity for new builds at the most accessible locations will persist. At the same time, more new builds will cause vacancy rates elsewhere in the city to increase due to the flight to quality by office occupiers. In view of this, policy in the years ahead is likely to revolve around a combination of space for new builds and transformation. This will be necessary not only in order to maintain a balanced offices market in terms of quantity and quality, but also to achieve planning capacity for housing construction in outdated office space. Besides, this policy strategy also boosts the local economy and accelerates sustainability upgrades for office stocks.

Most recent reports

-

Dutch retail parks are showing resilience: stable rental income, low vacancy rates, and attractive returns for investors.

-

The logistics market is entering a new phase. Following a period of growth, which peaked during the Covid-19 pandemic, it is now giving way to consolidation.

-

Report | Intelligent Investment

European Life Sciences Ecosystems: Sector Guide 2026

The European life sciences sector is a key contributor to global innovation and growth, propelled by technological breakthroughs, expanding scientific platforms, and a robust pipeline of novel therapies.

-

How the 25 most expensive retail streets adapt to shifting consumer behavior and economic pressures.